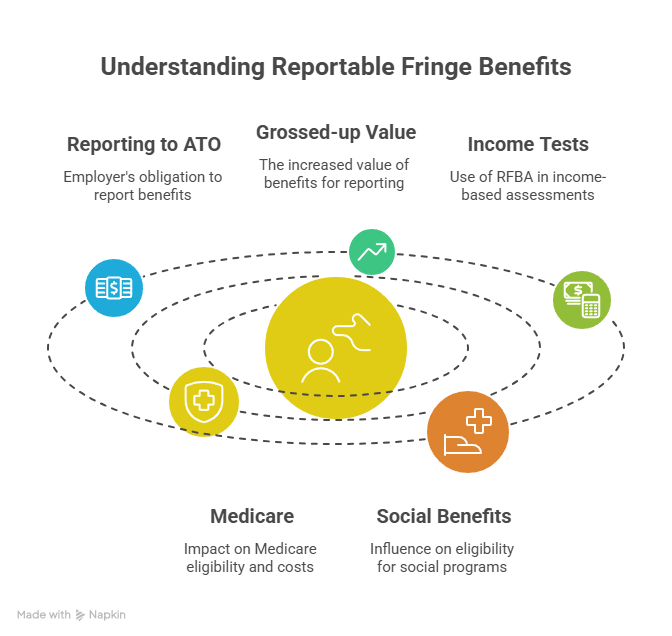

When you receive fringe benefits from your employer, those perks may be subject to being reported on your year-end income documents. A Reportable Fringe Benefits Amount (RFBA) is the grossed-up value of certain fringe benefits that your employer reports to the ATO for transparency. While it doesn’t add to the tax you pay on your income, it does get used for various income tests (for things like Medicare, social benefits, etc.). Here’s what you need to know about reportable fringe benefits.

The $2,000 Threshold

Not every cup of coffee or minor perk is reported – there’s a minimum threshold. If the total taxable value of your fringe benefits in an FBT year (1 April to 31 March) is more than $2,000, your employer must report it. If the value is $2,000 or less, nothing gets reported. The key word here is taxable value (the value after any FBT exemptions or reductions). The ATO notes that if the taxable value exceeds $2,000 during the FBT year, the grossed-up amount is reported (for example, $2,000.01 becomes $3,773 RFBA) (ATO, 2025).

How Reportable Amounts Are Calculated

Your employer does the heavy lifting in calculating the RFBA – you don’t need to crunch the numbers yourself. They will:

- Determine the taxable value of each fringe benefit you received. (Different benefit types have different valuation rules under FBT law.)

- Sum all those taxable values for the FBT year.

- If the total exceeds $2,000, multiply it by the gross-up rate (currently 1.8868 for reporting purposes). Even if a higher gross-up rate applied when calculating FBT, the lower rate is used for all benefits when reporting.

- Include the resulting grossed-up figure as a reportable fringe benefits amount on your PAYG payment summary or income statement for the financial year (ending 30 June).

Does an RFBA Affect Your Taxable Income?

No – an RFBA does not mean you pay more income tax. You do not include the RFBA in your assessable income on your tax return, and it doesn’t change the tax on your wages. Your employer’s FBT payment has essentially taken care of the tax on those benefits.

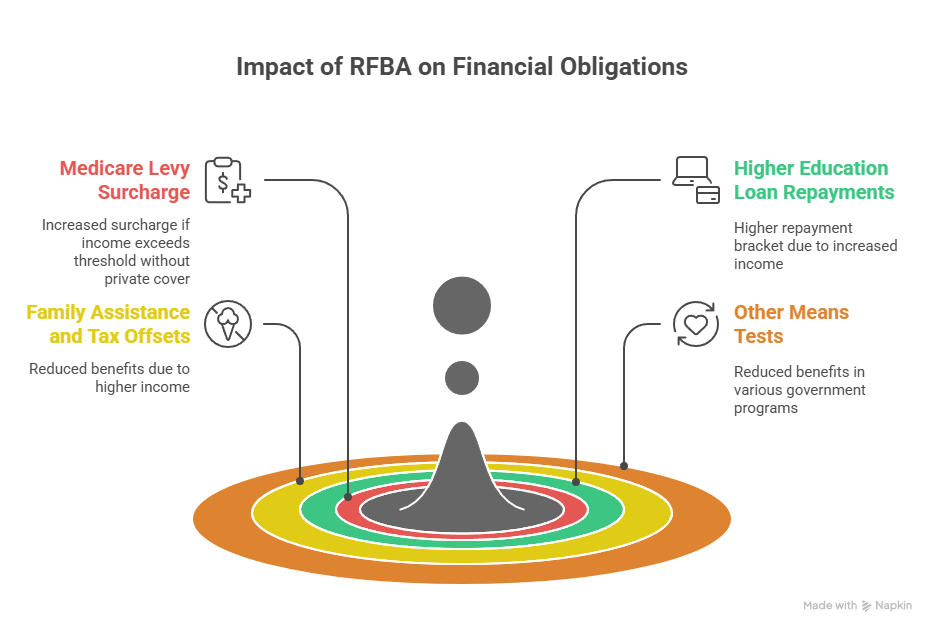

However, the RFBA is used by government agencies to assess your “adjusted income” for a range of thresholds and benefits. The logic is that fringe benefits, while not taxed as income, still increase your effective income and ability to pay. Therefore, the grossed-up RFBA is counted when determining:

- Medicare levy surcharge – if your income including RFBA goes over the surcharge threshold and you don’t have private hospital cover, you’ll be liable for the surcharge.

- Higher Education Loan Program (HELP) and similar loan repayments – your RFBA is added to your taxable income to calculate your repayment income, possibly pushing you into a higher repayment bracket.

- Family assistance and tax offsets – programs like Family Tax Benefit Part A and B, childcare subsidies, and tax offsets (e.g. the seniors and pensioners tax offset) use income tests that include any RFBA.

- Other means tests – any government calculation that looks at “adjusted taxable income” (for example, certain Centrelink benefits or older superannuation surcharge calculations) will include your RFBA as part of your income.

Tips for Employees

From an employee perspective, you typically can’t alter the RFBA your employer reports (aside from reducing your fringe benefits themselves). But you should:

- Be aware of your RFBA: Check your income statement or PAYG summary. If you have a reportable amount listed, know that that figure will be used for the above tests. It might explain, for instance, why you got a Medicare surcharge bill despite your base salary being under the threshold.

- Plan around thresholds: If your RFBA is pushing you just over a threshold (say, just $1,000 over a Medicare surcharge income limit), you could discuss options with your employer. Perhaps you might take a slightly smaller benefit or make an after-tax contribution to reduce the fringe benefit value – small adjustments could keep you below certain cutoffs.

- Consider employee contributions: In some salary packaging arrangements, you can make out-of-pocket payments toward the benefit (for example, paying part of your novated lease car’s running costs yourself). Doing so reduces the taxable fringe benefit and thus the RFBA. Essentially, you’re trading off some tax savings to reduce your reported benefits amount – which can be worthwhile if it preserves an entitlement (for example, avoiding loss of a rebate or incurring a surcharge).

- Know the exemptions: Benefits like work-related items or minor benefits under $300 are not included in the RFBA calculation. If you have control or choice in your benefits, it’s good to know which perks are “FBT-free” versus those that aren’t. Opting for an exempt benefit means no FBT for your employer and no RFBA for you.

For further reading on a related topic, check out our fringe benefits and novated leases guide which explores the FBT implications of salary packaging a car (a common source of reportable benefits).

Learn what Reportable Fringe Benefits (RFBA) mean, how they impact your tax, and why they matter. TTS & Associates can help—contact us today.