Financial Planning Retirement is easier when you treat it as a series of decisions, not one big leap. Most people need to answer the same practical questions: when can I stop working, what income will I have, what will happen to my super, and how do tax and government benefits fit in?

This guide explains the moving parts in Australia and the common traps we see, especially around superannuation and timing. This is general guidance for Australians and isn’t personal financial advice.

Start with your target lifestyle, not a magic number

Retirement goals work best when they’re based on what you want your life to look like. A budget-style estimate of future spending is often more useful than chasing a single “lump sum” target.

Consider:

- housing costs (mortgage, rent, downsizing, maintenance)

- health and insurance costs

- travel and lifestyle spending

- support for family members

- one-off costs (car replacement, renovations)

ASIC’s MoneySmart provides tools and guidance on building a retirement plan and estimating income (see MoneySmart – plan for your retirement).

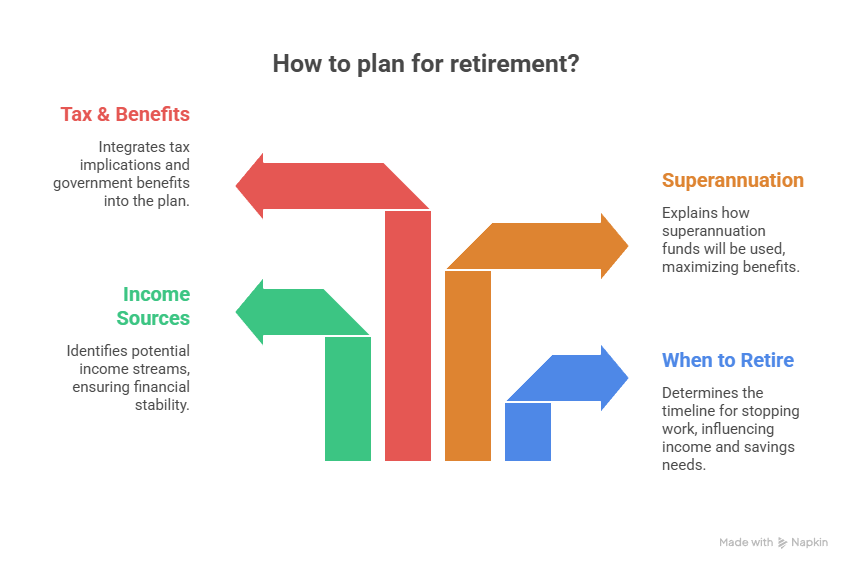

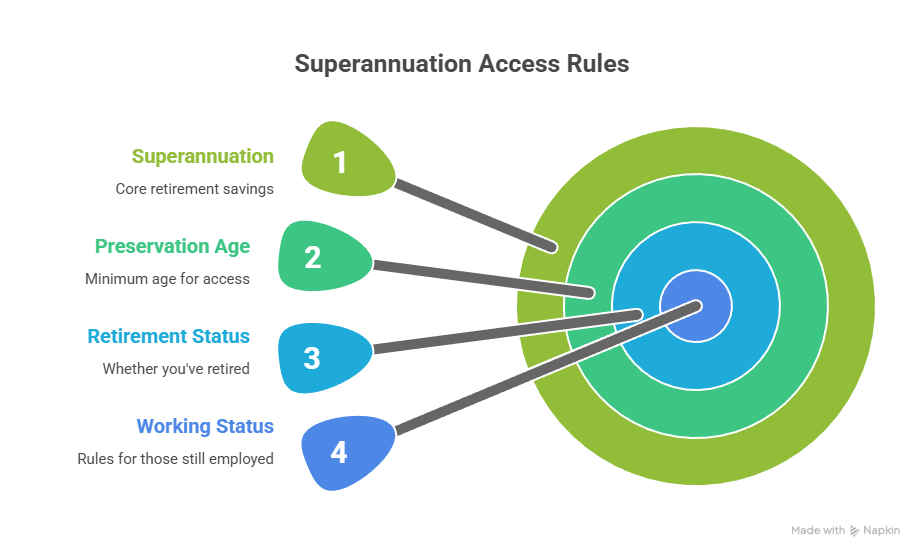

Understand when you can access super

Superannuation is usually the biggest pool of retirement savings, but access is tied to rules. Your ability to access super generally depends on your preservation age and retirement status, and different rules apply for people still working.

The ATO explains key concepts and where to find your preservation age and access conditions (see ATO – super and planning for retirement).

If you’re considering whether a Self-Managed Super Fund (SMSF) is appropriate as you approach retirement, this guide can help you understand the setup and responsibilities: Set up self managed super fund.

Build your income “stack”

Retirement income usually comes from a mix of sources. Mapping the “stack” helps you see which parts are stable and which parts fluctuate.

Common sources include:

- super income streams (e.g., account-based pensions)

- part-time work or business income (early retirement years)

- investment income outside super

- government benefits such as the Age Pension (subject to eligibility)

A key planning issue is sequencing: which source funds which years. For example, some people draw from non-super savings first, while others prefer to preserve outside assets depending on tax, risk, and flexibility.

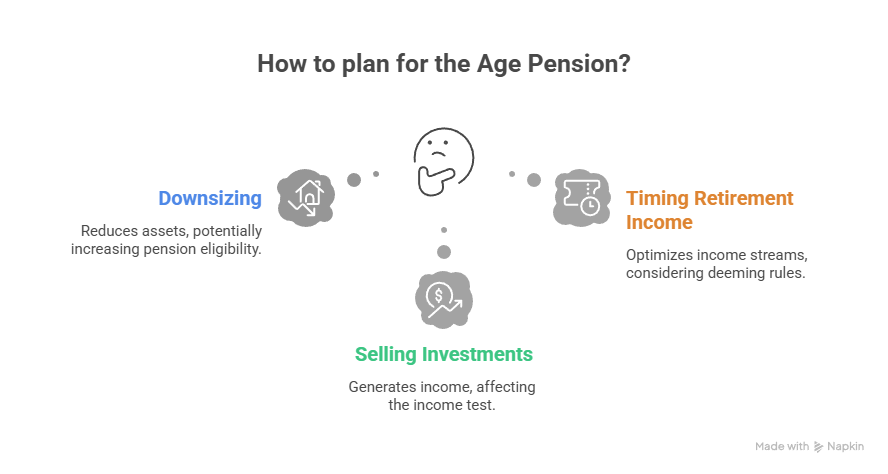

Factor in Age Pension rules early

Even if you expect to be “self-funded”, it’s worth understanding how the Age Pension is assessed because eligibility can change over time as spending and assets move.

Services Australia uses both an income test and an assets test, and financial assets can be subject to deeming (see Services Australia – income test and Services Australia – assets test). Planning around these rules can affect decisions like downsizing, selling investments, or the timing of retirement income streams.

Plan for tax at the drawdown stage

Tax doesn’t stop at retirement; it changes shape.

Areas to think about:

- taxable income from investment properties or dividends

- capital gains tax if you sell assets

- the tax treatment of different super components and income streams

- Medicare levy and any relevant offsets

Super itself can be tax-effective, but contribution and balance rules matter before you retire. The ATO sets contribution caps and explains how contributions are taxed (see ATO – contributions caps).

If you’re still building wealth, tax planning can help reduce “surprise” liabilities and improve cash flow. You can explore our overview here: Tax planning in Australia.

Don’t overlook transition years and paperwork

Many retirements aren’t clean cut. People downshift, change roles, or sell a business. These “transition years” are where planning pays off.

Practical steps include:

- checking employment arrangements and super contributions

- reviewing insurance cover as income changes

- updating beneficiary nominations and estate documents

- documenting cost bases and records for investments you may sell

If you’re a business owner, succession and exit timing can interact with tax outcomes and family goals. This guide is a useful starting point: Succession planning plan.

Choosing help: what’s regulated and what to ask

In Australia, personal advice about financial products (including super and investments) is regulated. If you work with an adviser, confirm they’re authorised and review their background (see MoneySmart – financial advisers register).

Questions worth asking include:

- What is in scope (retirement modelling, super strategy, insurance, estate coordination)?

- How are fees charged and how often will the plan be reviewed?

- What assumptions are used (inflation, market returns, spending changes)?

- How will tax be considered alongside the advice?

Your accountant can also help you understand tax consequences and keep reporting aligned with the plan, particularly if you have a business, property, or an SMSF.

A practical retirement planning checklist

To keep it simple, work through this list:

- Estimate annual spending in retirement (today’s dollars).

- Map your retirement income sources and when they start.

- Confirm when you can access super and any conditions.

- Review contributions and caps while you’re still working.

- Identify likely asset sales and potential CGT outcomes.

- Check insurance needs and estate documents.

- Set a review cadence (at least annually, and after major life events).

Financial Planning Retirement is not about predicting every detail. It’s about making a few key decisions early, then adjusting as life changes.

General information only – seek professional advice before acting.