Running a Self-Managed Super Fund (SMSF) gives you control over your retirement savings—but it also comes with a high level of responsibility. If you’ve ever looked into managing your own super, you’ve likely come across the importance of SMSF accounting in keeping your fund compliant and effective.

Unlike industry or retail funds managed by professionals, an SMSF is a DIY structure where you act as the trustee. This means you’re responsible for managing investments, lodging tax returns, maintaining financial records, and ensuring the fund complies with strict superannuation laws. Good accounting practices are essential to avoid costly penalties and keep your SMSF on track for long-term retirement growth.

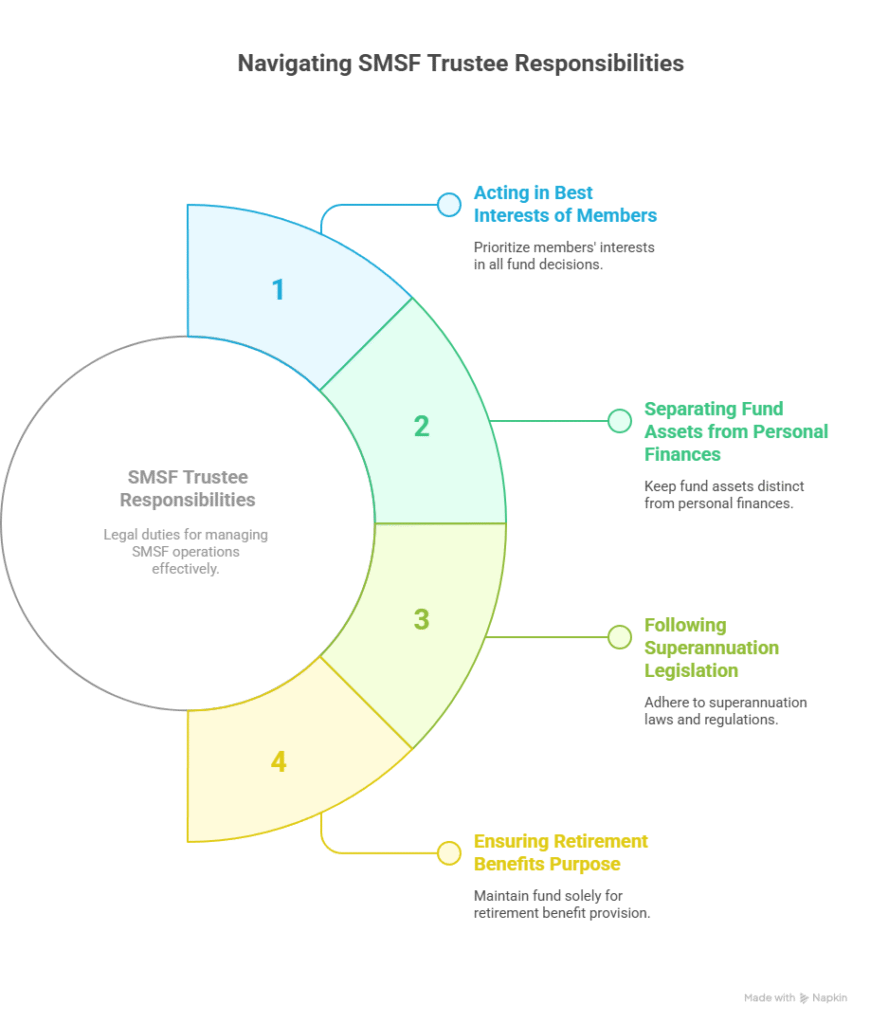

Know Your Responsibilities as an SMSF Trustee

As the trustee of your fund, you hold legal responsibility for its operations. Your duties include:

- Acting in the best interests of all members.

- Keeping fund assets completely separate from personal finances.

- Following superannuation legislation, including contribution caps and conditions of release.

- Ensuring the fund is maintained solely for the purpose of providing retirement benefits.

Failing to meet these responsibilities can result in severe penalties, including loss of the fund’s tax concessions or even disqualification as a trustee. That’s why accurate, compliant accounting is essential at every stage.

SMSF Accounting: What Records Must You Keep?

Superannuation law requires SMSF trustees to maintain detailed financial and administrative records for a minimum of 5 to 10 years. Incomplete or disorganised records can lead to ATO scrutiny or compliance breaches.

Here’s what you should be tracking:

1. Transactions and Supporting Documents

Keep records of all:

- Contributions (employer, personal, concessional, non-concessional)

- Investment income (dividends, rent, interest)

- Expenses (accounting fees, bank charges, asset purchases)

- Benefit payments

Attach source documentation like bank statements, invoices, and receipts to each transaction.

2. Financial Statements

Each financial year, you must prepare:

- An income statement (profit & loss)

- A balance sheet (assets, liabilities, and net assets of the fund)

These documents must be signed by all trustees as confirmation of their accuracy and readiness for audit.

3. Trustee Resolutions and Meeting Minutes

Record decisions such as:

- Approving financial statements

- Making investment decisions

- Paying benefits

- Adopting or changing the investment strategy

Minutes provide a clear audit trail, proving that your fund is operating in line with regulations and your stated strategy.

Annual Audit & SMSF Reporting Obligations

Each SMSF must be audited by an approved SMSF auditor every year before the fund’s annual return can be lodged with the ATO.

Timing:

- You must appoint the auditor at least 45 days before your SMSF Annual Return due date.

- If you use a registered tax agent, you may be eligible for an extended deadline.

SMSF Annual Return (SAR)

The annual return includes:

- The fund’s income tax return

- Regulatory information

- Member contribution reporting

Even if your SMSF has no tax to pay, lodging the return is mandatory. Late lodgment may result in administrative penalties or even a status downgrade of the fund on ATO registers.

Tips to Keep Your SMSF Compliant

Following these best practices can help ensure your fund remains compliant and audit-ready:

1. Separate Personal and SMSF Finances

Never mix personal and fund assets. This is a common breach that can invalidate the fund’s tax concessions. Always maintain a dedicated bank account for the SMSF.

2. Adhere to the Investment Strategy

Your fund must have a written investment strategy, and your investments must align with it. If you change your investment approach (e.g. moving from shares to property), document this in your trustee minutes and update the strategy accordingly.

3. Monitor Contributions and Conditions of Release

Always stay within contribution caps (e.g., $27,500 concessional limit for 2024–25). Only pay benefits when a member meets a condition of release—such as retirement or reaching preservation age.

4. Stay Up to Date

SMSF regulations change regularly. Subscribe to ATO updates for trustees or engage a professional to help interpret new rules. Ignorance is not an acceptable excuse for breaches.

SMSF Accounting Software and Support

Many trustees use SMSF-specific accounting software (like BGL Simple Fund 360 or Class) to automate record-keeping and streamline reporting.

However, as your fund grows or becomes more complex (e.g. including property, borrowing, multiple members), it often makes sense to engage a professional SMSF accountant. They can assist with:

- Preparing annual financial statements

- Liaising with auditors

- Lodging the SMSF Annual Return

- Providing advice on tax and compliance

- Interpreting super law changes

Why Work With SMSF Accounting Experts?

While SMSFs offer flexibility and control, compliance can be time-consuming. That’s where a professional team like TTS & Associates can help.

If you’re also considering starting a business in Australia, check out our comprehensive guide: Establishing a Business in Australia: Beginner’s Guide 2025.

Partnering with experts ensures:

- Your fund is fully compliant

- You meet all lodgment deadlines

- You get guidance tailored to your investment strategy

- You reduce risk of ATO penalties or breaches

An SMSF accounting specialist also provides strategic insights that help you grow your retirement savings while staying within the rules.

Need Help With SMSF Accounting?

If you want peace of mind that your SMSF is running smoothly, contact us today. Our experienced team at TTS & Associates can help manage your fund’s accounting, audit preparation, and ATO lodgments—so you can focus on your long-term financial goals.

Disclaimer

This article provides general information only. You should seek personalised advice from a registered SMSF specialist or financial advisor before making decisions regarding your SMSF.