Starting a business as a sole trader in Australia is one of the simplest and most cost-effective ways to begin trading. As a sole trader, you operate the business in your personal capacity – there’s no legal separation between you and the business. This makes setup easy, with minimal red tape and low upfront costs. However, becoming a sole trader also means taking full personal responsibility for your business’s debts, obligations, and tax requirements.

This guide explains how to set up as a sole trader, from registering your business and meeting legal obligations to managing tax and getting professional support.

What Is a Sole Trader?

A sole trader is an individual operating a business in their own name or under a registered business name. It is the simplest and most common business structure in Australia. You control all decisions, receive all profits, and are personally responsible for losses and liabilities.

Unlike a company, there is no legal separation between you and your business. This structure suits freelancers, tradies, consultants, and small business owners who want a straightforward way to start trading.

Step-by-Step Guide to Setting Up as a Sole Trader

1. Apply for an ABN

An Australian Business Number (ABN) is essential if you’re carrying on an enterprise, such as selling goods or services. You’ll need it to issue tax invoices, register for the Goods and Services Tax (GST) (if applicable), and conduct business legally.

- Apply for an ABN online via the Australian Business Register

- The application is free and takes around 10 minutes

- You’ll need to provide your Tax File Number (TFN), personal details, and business activity information

If your application is complete and accurate, your ABN is usually issued instantly.

2. Register a Business Name (If Needed)

As a sole trader, you can trade under your legal name (e.g. John Smith) without further registration. However, if you want to operate under a trading name such as “Smith’s Plumbing Services,” you must:

- Check name availability via the ASIC Business Name Register.

- Register the name with ASIC

- Pay the fee: approx. $42 for one year or $98 for three years

Business name registration does not give you trademark protection – that requires a separate application with IP Australia.

3. Open a Business Bank Account

While not mandatory, opening a separate bank account for your business:

- Helps manage cash flow

- Keeps personal and business expenses separate

- Makes tax reporting easier

Many Australian banks offer low-fee or no-fee business accounts for sole traders. Keeping separate accounts improves record-keeping and is considered best practice.

4. Check for Industry Licences or Permits

Depending on your profession or location, you may need specific licences or permits. For example:

- Builders or electricians require trade licenses.

- Food businesses often need council approvals.

- Health or beauty service providers may need hygiene permits.

Tax Obligations for Sole Traders

1. Income Tax and Reporting

As a sole trader, you report your business income and expenses as part of your personal tax return:

- Include a Business Schedule in your individual income tax return

- Pay tax at your individual marginal tax rate

- You do not need to lodge a separate company tax return

Good record-keeping is essential. Keep receipts, invoices, and business records for at least five years to comply with ATO requirements and support any tax deductions you claim.

2. Registering for GST

You must register for GST if your annual business turnover is expected to exceed $75,000. Once registered:

- You must charge 10% GST on taxable sales

- Lodge Business Activity Statements (BAS), usually quarterly

- Claim credits for GST paid on business purchases

Voluntary GST registration is allowed even if your turnover is under the threshold, which may benefit some businesses for claiming input tax credits.

3. PAYG Instalments and Income Tax Payments

Unlike employees, sole traders do not have tax withheld from business income. To stay on top of tax:

- Set aside a portion (e.g. 25–30%) of each payment for tax and Medicare

- Consider setting up voluntary PAYG instalments

- The ATO may later require you to make quarterly PAYG instalments if your income exceeds a threshold

You are responsible for calculating and paying your own tax – late or underpaid taxes can attract interest or penalties.

4. Superannuation Contributions

While sole traders are not required to pay themselves super, contributing to your own super fund is wise for retirement planning. Voluntary contributions may also be tax-deductible.

If you hire employees or contractors deemed employees for super purposes, you must pay the Super Guarantee (SG) for them.

Insurance Considerations for Sole Traders

Because you’re personally liable for any business debts or legal action, insurance is important. Common types include:

- Public liability insurance – protects against third-party injury or damage claims

- Professional indemnity insurance – essential for consultants and service professionals

- Income protection insurance – replaces part of your income if you can’t work due to illness or injury

While not mandatory in all industries, insurance protects your personal assets and financial wellbeing.

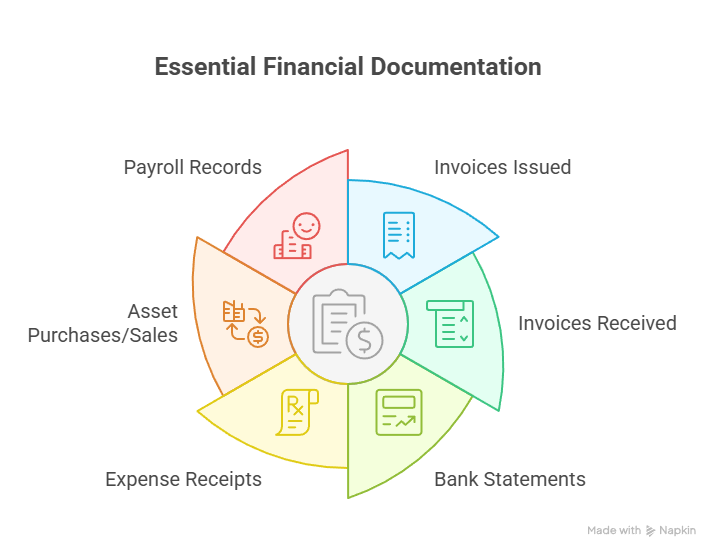

Record-Keeping Requirements

The ATO requires sole traders to keep records for five years, including:

- Invoices issued and received

- Bank statements

- Expense receipts

- Asset purchases or sales

- Payroll records (if applicable)

Digital record-keeping software can help streamline this process. Many sole traders use tools like Xero, QuickBooks, or MYOB to manage invoicing, expenses, and BAS reporting.

Getting Support When Starting Out

Even though the sole trader setup is simple, professional advice can help you get started on the right foot. Consider speaking with:

- An accountant or bookkeeper – for tax registrations, deductions, and GST

- A business advisor – for structuring, goal setting, or growth planning

- Government resources – such as business.gov.au, which provides guides, templates, and access to small business workshops

Taking time to set up your business properly reduces stress and future problems.

Reviewing Your Business Structure Over Time

As your business grows, it may outgrow the sole trader model. Reasons to change structure include:

- Seeking limited liability protection

- Bringing in co-owners or partners

- Needing to raise external funding

- Planning for future tax efficiency

You can transition to a company, partnership, or trust as your business evolves. Start simple – but review your structure periodically to ensure it still suits your goals.

Final Thoughts

Becoming a sole trader in Australia is a straightforward and popular way to start a business. It offers flexibility, low cost, and control. However, it also comes with personal liability and tax responsibilities. By registering correctly, maintaining good records, managing your tax, and seeking support when needed, you’ll be well-positioned for success.

For broader guidance on launching your business, read our article on Starting a Business in Australia: A Step-by-Step Guide (insert actual link). If you’d like tailored help, feel free to contact us for expert support.