A family (discretionary) trust can help manage family wealth, provide asset-holding flexibility and—in the right cases—deliver tax efficiency. Getting family trust set up steps correct at the start prevents costly rewrites later. This guide walks through the core decisions, the paperwork, and the ATO registrations most families need.

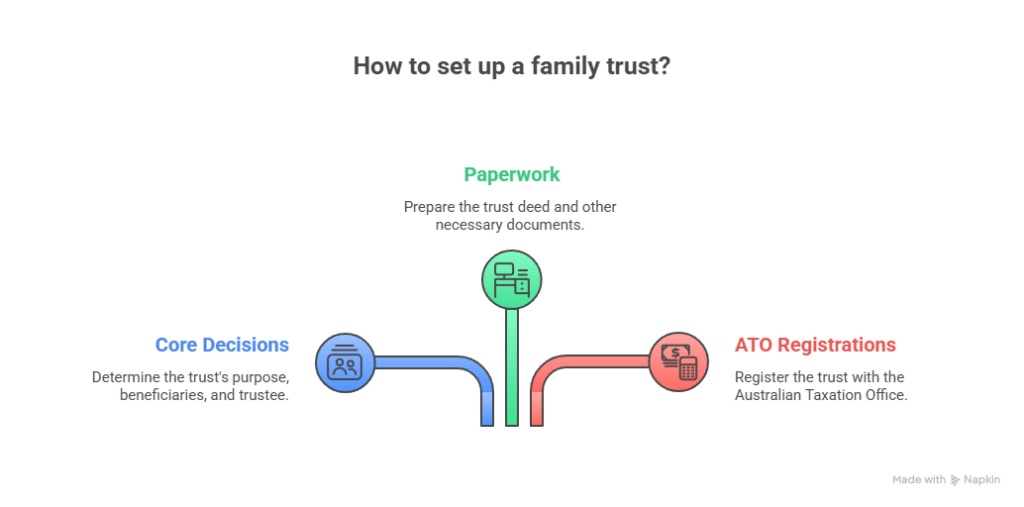

Decide the role and beneficiaries

Clarify why you want the trust: investment holding, running a business, or estate-planning flexibility. A discretionary trust gives the trustee power to distribute income or capital among defined beneficiaries. The ATO’s family trust page explains how “family trust” is a tax concept tied to making a Family Trust Election (FTE), not just a label on your deed (see Family trusts). Australian Taxation Office

Draft and execute the deed

Work with a lawyer to draft a deed that defines the trust, appoints a trustee (individuals or a company), sets the appointor/replacement rules, and outlines distribution powers. Once executed and (where required) stamped under your state rules, store an original copy safely and create certified copies for banks and the ATO.

Choose the trustee structure

A corporate trustee is common: it simplifies asset separation and succession (directors can change without retitling property). Individual trustees can be cheaper but complicate ownership changes later.

Obtain TFN, ABN and registrations

A trust generally needs its own Tax File Number (TFN) and, if carrying on an enterprise, an ABN. The ATO explains trust registration and reporting, including separate obligations when the trust is an employer or in the PAYG instalment system.

Applications are made via abr.gov.au (often together with the ABN application). The ATO provides instructions for organisational TFN applications.

Consider a Family Trust Election (FTE)

An FTE can unlock concessions (for example, loss/tracing concessions and certain franking-credit integrity rules) but narrows who can receive distributions without triggering Family Trust Distribution Tax (FTDT). Make this election with care and keep your family group register up to date. The ATO’s instructions explain the process and how revocations/variations work.

Build a compliance rhythm

- Annual trust minutes: Document trustee resolutions before 30 June or the deed’s stipulated date to ensure beneficiaries become presently entitled.

- Bank and accounting: Use a dedicated bank account. Map your ledger to trust tax return labels, and attach invoices to entries.

- Distributions to minors: Be aware that Division 6AA imposes higher tax on most unearned income for minors (some excepted income exists, such as from testamentary trusts). The ATO’s trustee instructions outline how these rules operate for under-18 beneficiaries.

Risk management and ATO focus areas

The ATO’s compliance guide PCG 2022/2 sets out how it approaches section 100A (trust reimbursement agreements). Keep commercial documentation, avoid circular flows, and seek advice before implementing complex arrangements.

Common pitfalls (and easy fixes)

- Vague minutes: Use clear resolutions naming beneficiaries and classes of income.

- Using personal accounts: Always transact through the trust’s account to preserve records.

- Late TFN/ABN: Apply early—banks often require them to open accounts.

- Untracked loans: Related-party loans in and out of the trust should have written terms and interest where appropriate.

For a deeper walkthrough of documents and sequencing, read TTS & Associates’ How to Set Up a Trust in Australia: Step-by-Step Guide and Trust Setup Australia: Simple Steps.

General information only – seek professional advice before acting.