Investing in early‑learning facilities is one of the few opportunities that delivers both reliable cash flow and meaningful social impact. Demand continues to rise, fuelled by dual‑income households and the Federal Government’s Child Care Subsidy (CCS).

With the right ownership structure, you can capture this upside while staying fully compliant with Australian tax law. This guide explains the main investment models, key tax considerations and practical steps for maximising after‑tax returns.

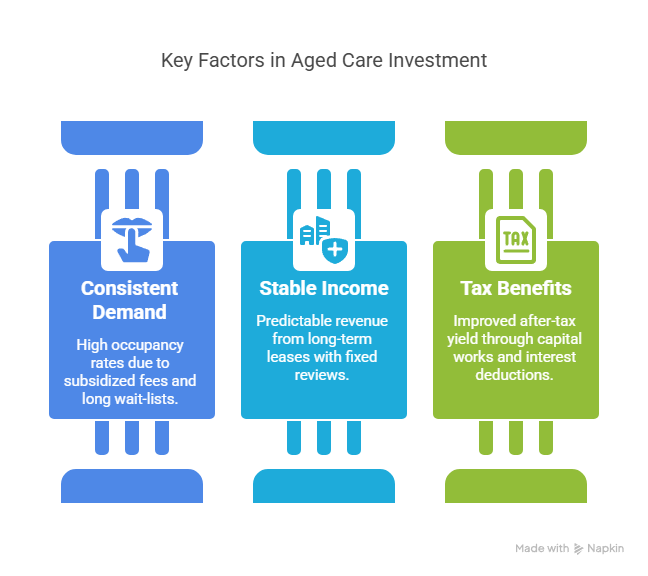

Why Child Care Is a Compelling Asset Class

- Consistent demand. Subsidised fees and long wait‑lists underpin high occupancy rates.

- Stable income. Long leases (often 10–20 years with fixed reviews) provide predictable rent or operating revenue.

- Significant tax benefits. Capital‑works deductions, depreciation on fit‑out and interest deductions can materially improve after‑tax yield.

Three Principal Investment Structures

1 Direct Property Ownership (Landlord Model)

You purchase the land and building, then lease it to an approved provider.

| Tax benefit | Detail |

| Capital‑works deduction | Claim 2.5 % p.a. over 40 years on the building and eligible fit‑out. |

| Interest deduction | Loan interest is fully deductible where borrowings are used to acquire the property. |

| GST treatment | Commercial rent is generally subject to GST. The operator (who makes GST‑free supplies of child‑care services) can still claim the input‑tax credits. (community.ato.gov.au) |

| CGT | Hold >12 months to access the 50 % discount (individuals and trusts). |

Best for: Investors seeking passive income with strong tenant covenants and long‑term capital growth.

2 Operate the Child Care Business Yourself

You hold the service approval, employ staff and either lease or own the premises.

- Assessable income – Parent fees and CCS amounts paid to the centre are both assessable for income‑tax purposes. (ato.gov.au)

- Deductible expenses – Wages, consumables, utilities, rent, insurance and depreciation on centre assets.

- GST – Fees charged to parents for approved care are GST‑free, but you can still claim input‑tax credits on related acquisitions. (community.ato.gov.au)

- Payroll tax – In Victoria the threshold rises to $900 000 from 1 July 2024 and $1 million from 1 July 2025. (sro.vic.gov.au) Check thresholds in your state or territory.

Best for: Hands‑on operators comfortable with compliance under the National Quality Framework (NQF) and ACECQA.

3 Develop‑to‑Lease (Build‑to‑Rent Model)

Acquire land, construct a purpose‑built centre and sign a long‑term lease with an operator.

- GST credits – Input‑tax credits on construction costs are claimable, improving project cash flow.

- Capital‑works deduction – Full 40‑year schedule starts once the building is ready for income production.

- Profit intent – If you sell on completion, the margin may be treated as ordinary income rather than a capital gain—structure the project carefully.

Best for: Experienced developers with access to capital and strong operator networks.

Cross‑Structure Tax Issues to Nail Early

- Choice of entity – Companies offer a 25 % tax rate but no CGT discount; discretionary trusts allow flexible distributions; unit trusts often suit syndicates. Seek advice before committing. citeturn0file0

- Depreciation schedules – Engage a quantity surveyor to capture every qualifying asset and maximise deductions. Instant asset write‑offs (currently $20 000 for small business entities) may apply—check the latest ATO thresholds.

- Land tax & rates – These vary by jurisdiction and can erode returns; model them conservatively. Some states offer concessions for preschool facilities—verify with the relevant revenue office.

- GST registration & BAS – Leasing property (taxable supply) or operating a centre (GST‑free supply) still requires BAS lodgements once turnover exceeds $75 000.

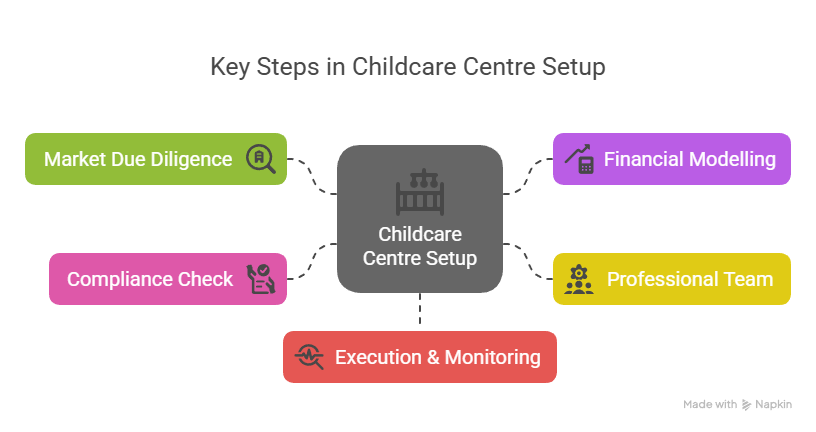

Practical Roadmap to a Tax‑Efficient Investment

- Market Due Diligence – Analyse demographics, parent demand and government funding trends.

- Financial Modelling – Build after‑tax cash‑flow forecasts under at least two different structures.

- Professional Team – Engage a tax accountant, solicitor and property adviser early—errors in entity setup are costly to unwind.

- Compliance Check – Ensure premises design meets NQF ratios, accessibility and local planning rules before settlement.

- Execution & Monitoring – Once operational, review BAS, PAYG and payroll‑tax obligations quarterly; update depreciation schedules after major capex.

A Final Word

Child care centre investments can deliver robust, inflation‑linked returns when structured correctly. By aligning ownership models with current Australian tax law—and leveraging deductions, GST credits and appropriate entities—you can enhance net yields while remaining fully compliant.

If you are considering entering this sector, speak with the specialist team at TTS & Associates. Since 2002 we’ve helped investors and operators design tax‑efficient structures that stand the test of time.

Disclaimer: The information above is general in nature and should not be taken as tax advice. Always consult a registered tax agent for guidance tailored to your circumstances.