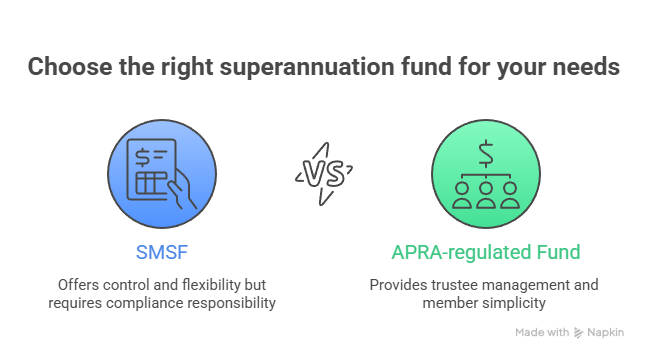

A superannuation self managed fund (often called an SMSF) can offer control and flexibility, but it also turns you into the person responsible for compliance. That’s a big shift from an APRA-regulated super fund where a trustee company runs the fund and you’re simply a member.

If you’re considering an SMSF, the most useful starting point is not “what can I invest in?” It’s “what am I legally responsible for, every year, without fail?”

What an SMSF is (and what it isn’t)

An SMSF is a private super fund set up for a small number of members. Each member is usually a trustee (or a director of a corporate trustee). The fund must meet the “sole purpose test”, meaning its activities must be for providing retirement benefits (see ATO: Setting up an SMSF).

An SMSF is not a personal bank account, a short-term property strategy, or a way to access super early. The flexibility exists inside strict rules.

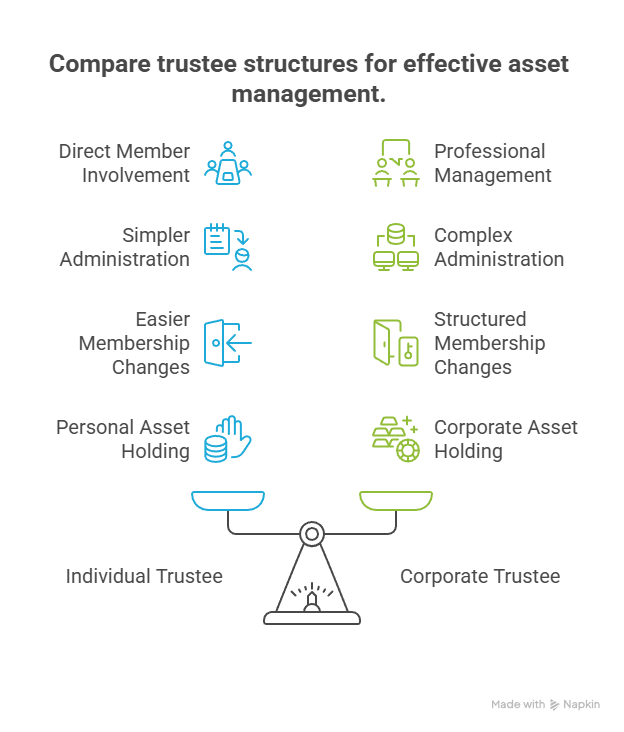

Trustee structure: individual vs corporate trustee

One of the first design choices is the trustee structure. With an individual trustee model, each member is a trustee. With a corporate trustee model, a company acts as trustee and members are directors. The structure you choose affects administration, changes in membership, and how assets are held.

There isn’t a universal “best” option, but corporate trustees can simplify some changes over time. The ATO outlines trustee structure considerations as part of the setup steps (see ATO: Setting up an SMSF).

The setup steps that must be done correctly

A superannuation self managed fund needs a valid foundation before it can receive rollovers or contributions. Key steps include:

- Create and execute a compliant trust deed

- Appoint trustees/directors and document acceptance of duties

- Establish a dedicated SMSF bank account

- Register the fund for an ABN and TFN and elect to be regulated

The ATO provides a specific registration pathway (see ATO: Register your SMSF). The “paperwork” isn’t busywork—errors at establishment can be painful to fix later, especially if assets have already been acquired.

For a practical walkthrough, see our guide Set Up a Self-Managed Super Fund (SMSF): Step-by-Step.

Ongoing obligations: where most people underestimate the workload

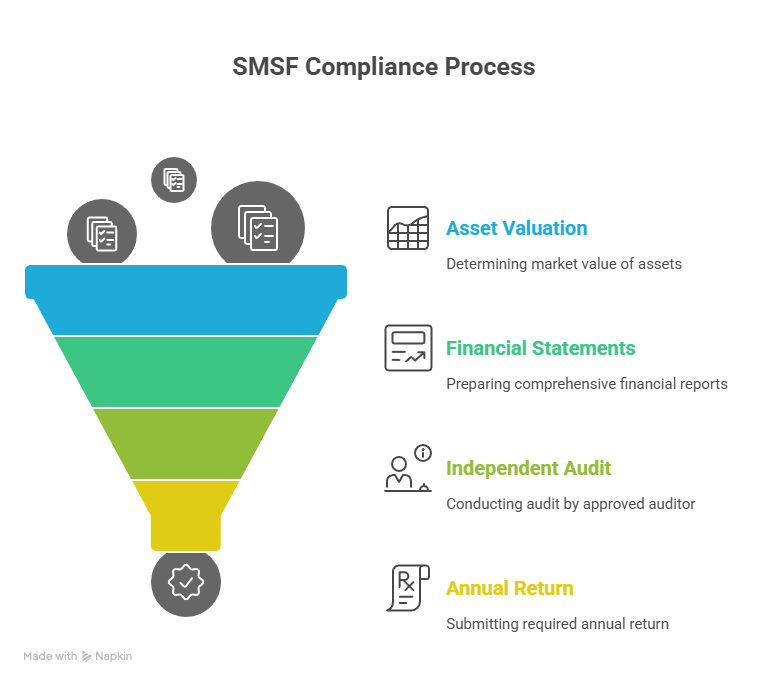

The ongoing obligations are what catch people out. Even if you outsource administration, trustees remain responsible for compliance. Each year, SMSF trustees generally need to:

- Keep records, minutes, and supporting documents for decisions

- Value fund assets at market value

- Prepare financial statements

- Arrange an independent audit by an approved SMSF auditor

- Lodge an SMSF annual return (SAR)

The ATO is clear that an SMSF annual return must be lodged each year, even if the fund has no tax liability (see ATO: Lodge SMSF annual returns). Auditors also have timing requirements (see ATO: Your SMSF auditor).

Investment strategy and arm’s length behaviour

Every SMSF must have an investment strategy, and it must be reviewed regularly. It should cover risk, diversification, liquidity, and insurance considerations. This is not just a “template”—it is meant to explain why the fund’s investments make sense for member circumstances.

The second pillar is arm’s length conduct. SMSFs have strict rules around related-party transactions and personal use. If you’re investing in property, for example, the fund must comply with the sole purpose test, and many “it’ll be fine” ideas are simply not allowed.

ASIC’s MoneySmart provides a useful reality check on the work involved and the need for financial and legal knowledge (see MoneySmart: Self-managed super fund).

What good governance looks like in practice

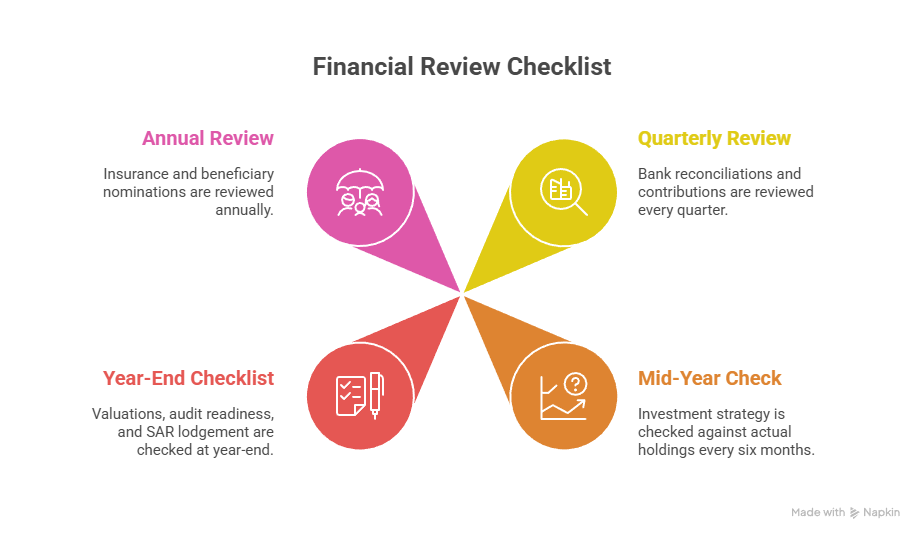

A well-run SMSF is boring in the best possible way. Decisions are documented, cash buffers are planned, and compliance work is scheduled. A practical governance rhythm might include:

- Quarterly bank reconciliations and review of contributions

- Six-month check of investment strategy vs actual holdings

- Year-end checklist for valuations, audit readiness, and SAR lodgement

- Annual review of insurance and beneficiary nominations

This is one reason we encourage trustees to align SMSF administration with their broader tax planning calendar. Our article Tax Planning for Victorians: 10 Smart Ways to Save Tax provides a simple month-by-month rhythm that many trustees adopt.

Is an SMSF right for you?

The best “fit test” is whether you want ongoing responsibility and have the time to maintain records and governance. Some people benefit from control and flexibility. Others are better served by an APRA-regulated fund.

If you’re weighing up costs, workload and suitability, see our selection criteria in SMSF Accountant: Tips for Choosing the Right Expert.

A superannuation self managed fund can be a strong retirement vehicle when it’s built on discipline and clean processes. It becomes risky when it’s built on shortcuts. TTS & Associates is well versed in superannuation and how it can be applied to your situation.

General information only – seek professional advice before acting.