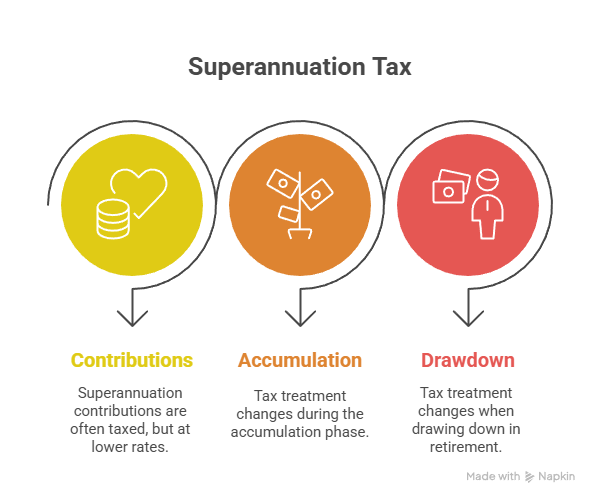

A common question we hear is “is superannuation taxed, or is it all tax-free?” The short answer is: super is usually taxed, but often at lower rates than ordinary income—and the tax treatment changes depending on whether you’re contributing, accumulating, or drawing down in retirement.

This overview covers the main tax points so you can ask better questions and avoid accidental breaches.

Tax on contributions: concessional vs non-concessional

Most employer Superannuation Guarantee (SG) payments and most salary sacrifice amounts are treated as concessional contributions. Concessional generally means “before-tax”, and in many cases the super fund pays contributions tax on the way in.

In many situations, concessional contributions are taxed at 15% inside the fund. That’s not a blanket promise—eligibility, caps, and special rules apply—but it’s a key reason super can be tax-effective compared with earning the same amount as salary.

Non-concessional contributions are typically “after-tax” personal contributions. They’re not generally taxed when they go into the fund, but strict annual caps and eligibility rules apply. If you exceed caps, additional tax and admin work can follow.

Contribution caps: the hidden driver of tax outcomes

The tax outcome is heavily influenced by whether you stay within contribution caps. Caps exist because super is a concessional system. The ATO publishes caps and thresholds (see ATO: Key super rates and thresholds).

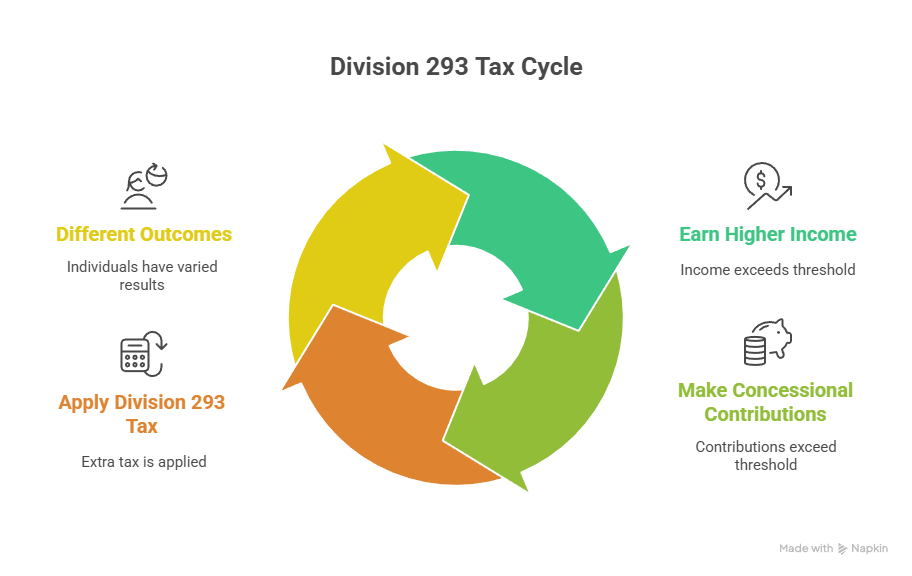

If you’re a higher-income earner, there’s another layer: Division 293 tax, which can apply extra tax to concessional contributions once your income and contributions exceed the relevant threshold. This is one reason a “one-size-fits-all” approach to super can backfire—two people with the same contribution amount can have different outcomes.

Tax on investment earnings inside super

Super funds invest your balance and earn income (dividends, interest, rent) and capital gains. In the accumulation phase, investment earnings are typically taxed within the fund, often up to 15%. Capital gains on assets held longer than 12 months may receive a discount within the fund, which can reduce the effective tax rate.

This is where structure and timing become practical. If you switch options frequently or crystallise gains, the internal tax settings can affect net returns even if you never see a “tax” line item.

Tax when you withdraw: the big picture

Tax on super withdrawals depends on your age, the form of the withdrawal (lump sum or income stream), and the components of your benefit (tax-free vs taxable components).

As a general guide, super income stream payments are usually tax-free once you’re aged 60 or over, but may be taxed if you’re under 60 (see MoneySmart: Tax and super). The ATO also publishes the withholding tables used by funds and administrators (see ATO: Super income stream tax tables).

Conditions of release: tax isn’t the only rule

Before tax is even relevant, you must meet a legal condition of release. Access to super is not automatic and generally requires reaching preservation age and meeting a condition of release such as retirement, or turning 65 (see ATO: Conditions of release).

Common scenarios that catch people out

Even when the general rules are understood, real-world situations create surprises:

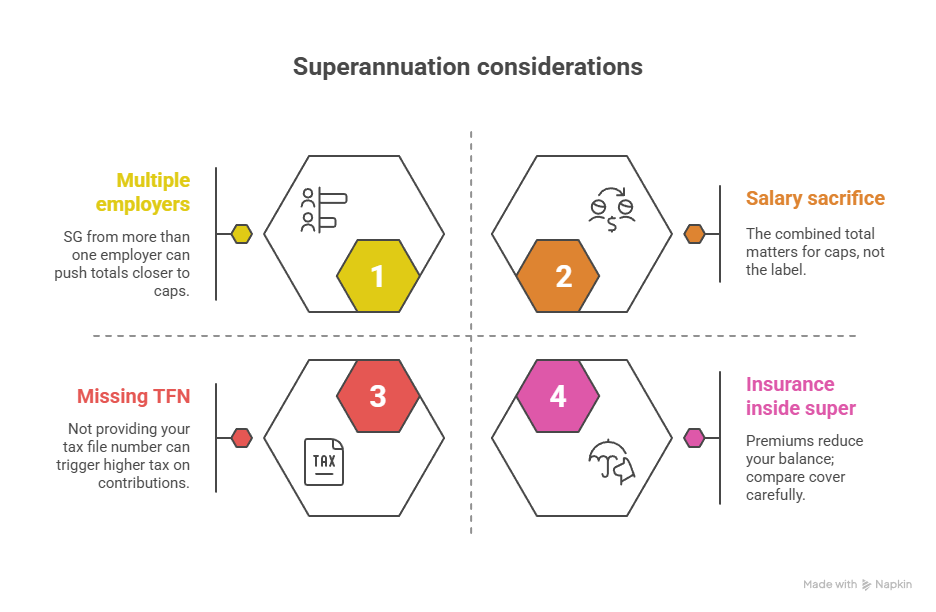

- Multiple employers: SG from more than one employer can push totals closer to caps.

- Salary sacrifice on top of SG: the combined total matters for caps, not the label.

- Missing TFN: not providing your tax file number can trigger higher tax on contributions.

- Insurance inside super: premiums reduce your balance; compare cover carefully.

SMSF-specific considerations

If you’re running a self-managed super fund (SMSF), trustee decisions (and documentation) directly affect compliance and tax reporting. You’ll want a tight admin rhythm: investment strategy, minutes, arm’s length documentation, and timely annual returns.

For SMSF basics, see What is a Self Managed Super Fund? and Set Up a Self-Managed Super Fund (SMSF): Step-by-Step.

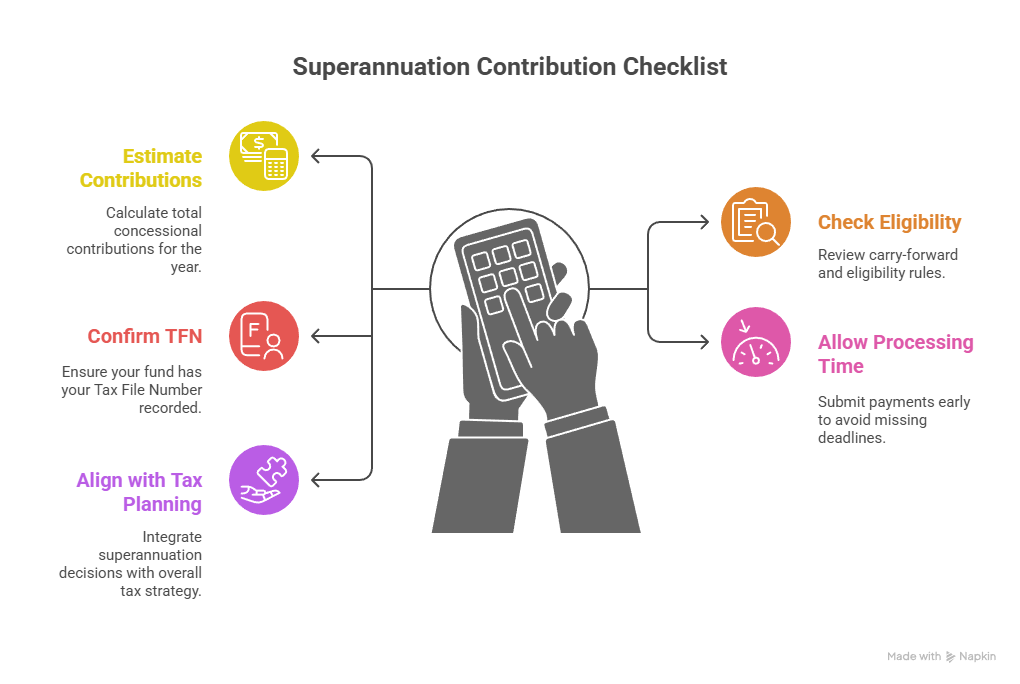

Practical planning: a checklist before 30 June

If you’re asking “is superannuation taxed” because you’re considering extra contributions, start with process:

- Estimate your total concessional contributions for the year (SG + salary sacrifice + personal deductible contributions)

- Check whether carry-forward or eligibility rules might apply

- Confirm your fund has your TFN recorded

- Leave time for processing—last-minute payments can miss cut-offs

- Align the decision with broader tax planning, not only a “super top-up”

For broader end-of-year preparation, you may also find our tax planning article useful: Tax Planning in Australia: 5 Smart Ways to Reduce Tax.

The bottom line

Super is tax-advantaged, not tax-free. The system rewards long-term saving, but the “price” is rules: caps, conditions of release, and different tax rates at different stages. Once you understand the moving parts, you can treat super as a strategy—rather than a mystery line on your payslip. TTS & Associates are experts in superannuation and how it can be applied to your situation.

General information only – seek professional advice before acting.