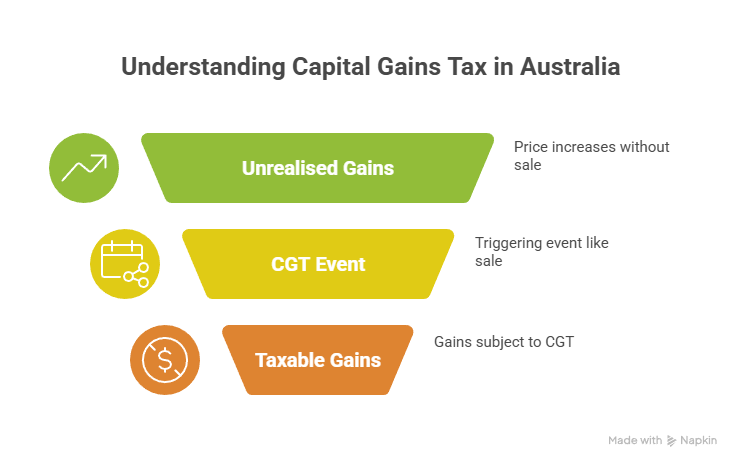

Many investors worry about unrealised capital gains tax but in Australia, CGT generally arises only when a CGT event happens, such as a sale or certain disposals. Price movements on assets you still hold are usually unrealised and not taxed until you trigger the event. There are important exceptions and planning choices to understand, especially around property, restructuring and super.

Realised vs unrealised: where tax actually bites

Your shares can rise in value for years without immediate tax. CGT is calculated when you dispose of them: proceeds minus cost base, then losses, then any 50% discount (12-month rule for individuals and trusts). The unrealised gain becomes realised at disposal and is added to your taxable income as a net capital gain (ATO CGT overview).

For assets held 12 months or more, many individuals can apply the 50% discount, halving the gain before it hits your tax return. Foreign residents have restricted access, and companies do not get the discount (ATO: CGT discount; CGT discount for foreign residents).

When unrealised amounts can still matter

While tax is not payable until a CGT event, record-keeping should start on day one. Keep contracts, settlement statements, and capital-improvement invoices, because they form your cost base and reduce future tax. The ATO sets five-year minimum retention rules, with some items needing longer—especially where they affect the cost base (ATO: Record-keeping for business).

In certain restructures or roll-overs, unrealised gains can be deferred, not eliminated. These events shift the taxing point into the future, so your paperwork must track the new cost base and acquisition date (ATO CGT overview).

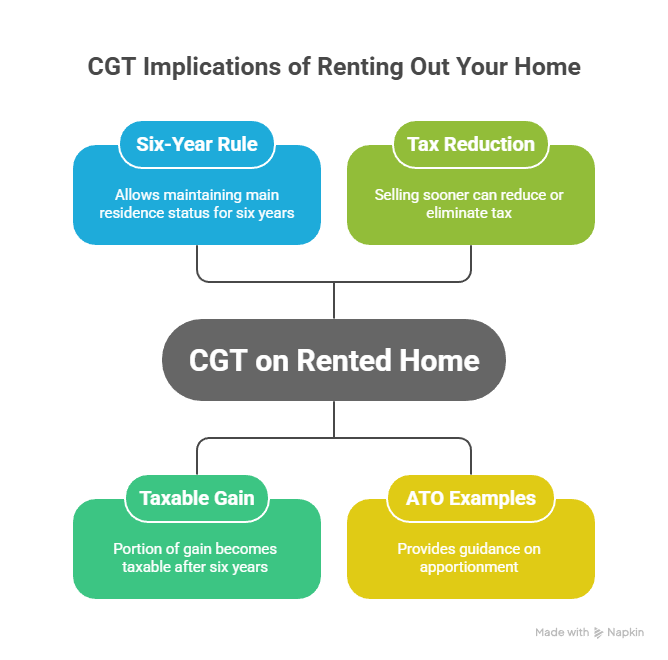

Property: the six-year absence choice makes timing critical

Your home is generally CGT-free. If you move out and rent it, you may choose to keep it as your main residence for up to six years while absent. This choice interacts with timing: hold beyond six years of rental and part of the gain can become taxable when realised; sell sooner and you could reduce or eliminate tax. The ATO’s examples show how to apportion across main-residence and rental periods (Treating former home as main residence).

Where you inherit property, CGT generally doesn’t arise at the time of inheritance. The unrealised position converts to a taxable gain if and when you later sell, subject to main-residence and two-year rules in certain cases (ATO: Inherited property and CGT).

Business sales: concessions can transform outcomes

If you run a small business, Division 152 small business CGT concessions can reduce, disregard or defer tax when you sell an active asset—once you satisfy basic conditions (turnover or net-asset tests, active-asset test, and significant individual rules). Here, the difference between unrealised (planning phase) and realised (contract date) matters because eligibility can turn on timing (ATO: Small business CGT concessions; Eligibility overview).

Super (SMSF) and unrealised gains

Inside a self-managed super fund (SMSF), investments are still generally taxed on realised gains. However, the tax rate depends on the fund’s phase: accumulation vs retirement phase, and whether exempt current pension income (ECPI) applies. Strategy and documentation—especially around limited recourse borrowing arrangements and asset valuations—directly affect outcomes. Our guides Superfund Accountant: Stay Compliant and SMSF Accounting: Keep Your Fund On Track outline simple routines.

Planning moves to consider before you sell

- Sequence losses: crystallise capital losses (where commercial) before gains to reduce the net position.

- Hold for 12+ months: if appropriate, crossing the 12-month mark can unlock the 50% discount.

- Model residence choices: with property, test the six-year absence choice against your sale timing.

- Small business eligibility: run the Division 152 tests early; don’t assume eligibility.

For property and BAS-adjacent workflows, TTS & Associates’ BAS lodgement simplified and Quarterly BAS due dates will help you keep paperwork audit-ready so the unrealised record becomes a clean, realised calculation when you sell.

Bottom line: unrealised capital gains tax is usually a misnomer—Australia taxes gains when realised. But the groundwork you lay while a gain is unrealised determines how much tax you’ll pay at the finish line.

General information only – seek professional advice before acting.