The NDIS has revolutionised disability services across Australia since its launch. While the social impact is undeniable, participants, providers, and investors must also navigate a set of tax rules that differ from mainstream arrangements. An experienced NDIS Tax Accountant can help you understand these complexities. This guide explains how Australian tax law interacts with NDIS funding, service provision, and related property investments, and it includes direct links to relevant government sources so you can verify each point for yourself.

1. Why Tax Treatment Matters

| Stakeholder | Why it’s important |

| Participants | NDIS funding is generally not assessable income (see the ATO’s ruling – QC 58539). Understanding GST‑free purchasing and record‑keeping rules protects your plan budget. |

| Providers | Correct GST classification, PAYG & super obligations and the right business structure all affect profit and compliance risk. |

| Investors | Specialist Disability Accommodation (SDA) can deliver attractive yields, but GST, CGT and land‑tax outcomes hinge on precise structuring. |

2. Tax Rules for NDIS Participants

| Item | Tax treatment | Key source |

| NDIS payments | Not taxable income. | ATO – NDIS payments |

| GST on supports | Supports are GST‑free when supplied to a participant under a current plan and by a registered provider – s 38‑38 GST Act, explained in GSTR 2013/1. | |

| Record keeping | Participants (and plan managers) must keep invoices for 5 years – see NDIA record‑keeping guidance. | |

| Personal tax deductions | Expenses paid with NDIS funds are private and not deductible – see TR 93/34. |

3. NDIS Providers – Key Obligations & Opportunities

3.1 GST

- GST‑free supplies – Services that satisfy s 38‑38 are GST‑free. Ensure invoices clearly separate GST‑free and taxable items.

- Registration – You must register if turnover > $75 000 (or $150 000 for not‑for‑profits). Details: ATO – Registering for GST.

3.2 Income Tax & Deductions

- Assessable income – Fees received from the NDIA or self‑managed participants are ordinary income (ITAA 1997 s 6‑5).

- Deductible expenses – Wages, rent, insurance, client‑transport vehicles, staff training, software and other ordinary expenses are deductible (ITAA 1997 s 8‑1).

- Depreciation / Instant Asset Write‑Off – Small businesses (turnover < $10 m) may access the instant asset write‑off for assets under the current threshold – see ATO guidance.

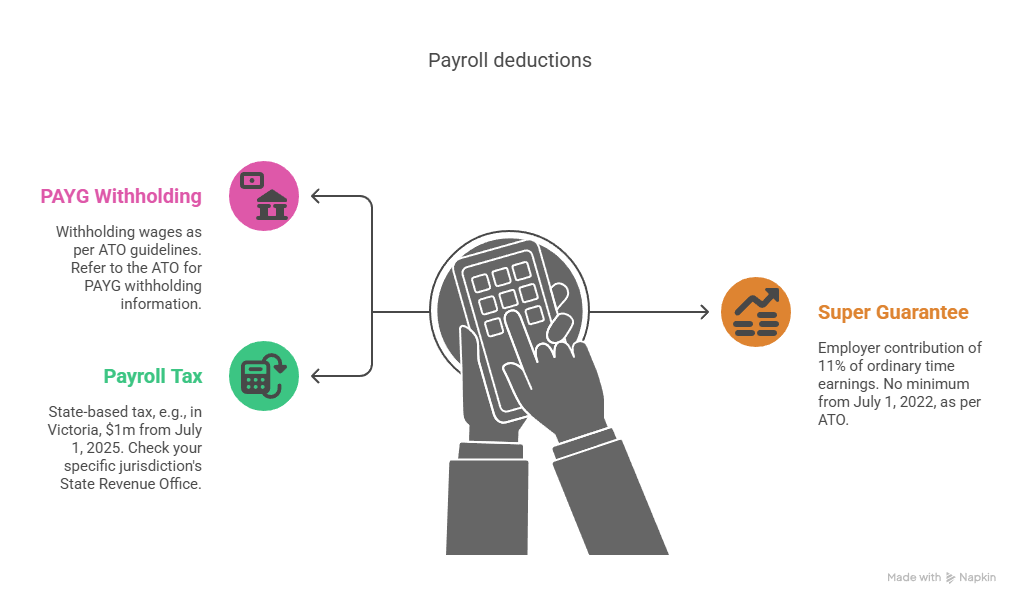

3.3 Employment Taxes

| Tax | 2024‑25 threshold / rate | Key link |

| PAYG withholding | Any wages | ATO – PAYG withholding |

| Super guarantee | 11 % of OTE (no minimum from 1 Jul 2022) | ATO – Super guarantee |

| Payroll tax | State based – e.g. Vic $1 m from 1 Jul 2025 | SRO Vic – Payroll tax (check your jurisdiction) |

3.4 Choosing the Right Structure

| Structure | Pros | Cons |

| Sole trader | Simple, cheap setup | Personal liability; profits taxed at marginal rates. |

| Company | 25 % base‑rate entity tax, asset protection | No 50 % CGT discount for shares held < 12 m by individuals. |

| Discretionary trust | Flexible income distribution; CGT discount | More complex admin; trustee duties. |

4. Investing in SDA & Other NDIS Property

| Issue | Treatment | Official source |

| Rental income | Assessable under ITAA 1997 s 6‑5. | |

| GST | Residential rents are input‑taxed – no GST on rent, no credits on expenses. | ATO – GSTR 2000/7 |

| Depreciation | Purpose‑built SDA often qualifies for higher rates – engage a quantity surveyor. | |

| Capital gains | 50 % CGT discount for individuals/trusts after 12 months. Small‑business CGT concessions apply only if the property is an active asset of your SDA operating business – see ATO small business CGT concessions. | |

| SDA compliance | Follow NDIA design standards & enrolment rules. | NDIS – SDA information |

5. Compliance Checklist

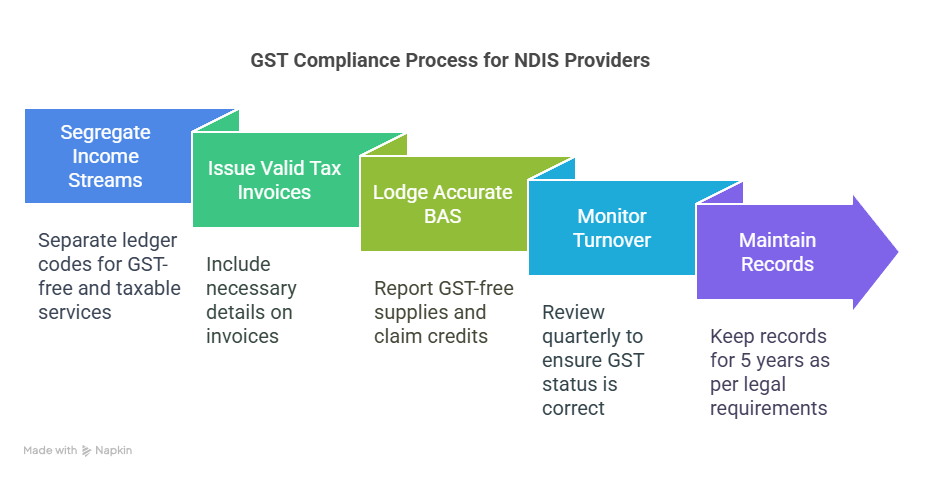

- Segregate income streams – Separate ledger codes for GST‑free NDIS services and taxable services.

- Issue valid tax invoices – Include provider ABN, invoice date, ‘GST‑free supply’ wording and participant plan reference.

- Lodge accurate BAS – Report GST‑free supplies at G1 + G3; claim credits at G10/G11.

- Monitor turnover – Review quarterly to ensure GST status remains correct.

- Maintain records for 5 years – s 382‑5 Taxation Administration Act 1953.

6. Next Steps

Navigating the NDIS tax landscape need not be daunting. By understanding GST classifications, leveraging legitimate deductions and selecting the optimal structure, participants, providers and investors can all enhance their financial outcomes while staying fully compliant.

The team at TTS & Associates has supported NDIS clients since the scheme’s pilot phase. Contact us for tailored guidance that aligns with ATO rulings and NDIA requirements.

Disclaimer: This article is general information only and does not constitute tax advice. Always seek personalised advice from a registered tax agent.