Fringe Benefits Tax (FBT) – often referred to in plural as fringe benefits taxes – is a tax that employers pay on certain non-cash benefits they provide to employees (or their associates) in place of salary or wages. If an employer provides such perks to staff – for example a company car for personal use, free private health insurance, or an interest-free loan – then FBT applies. The tax is designed to ensure those benefits are taxed similarly to cash salary. Here we explain how FBT works under Australian tax law, key rates and exemptions, and tips for managing your FBT obligations.

How FBT Works

FBT is paid by the employer, not the employee, and it is separate from income tax. It’s levied on the taxable value of the fringe benefits provided. The FBT year runs from 1 April to 31 March, aligning with many common benefit cycles. The FBT rate is currently 47% (equivalent to the top marginal tax rate) on the grossed-up value of benefits (ATO, 2025). “Grossing up” reflects the income an employee would have to earn (before tax) to buy the benefit themselves. For example, if you give an employee a benefit worth $1,000 (and you can claim GST credits on it), the taxable grossed-up value might be $2,080, and you as the employer pay 47% of that in FBT.

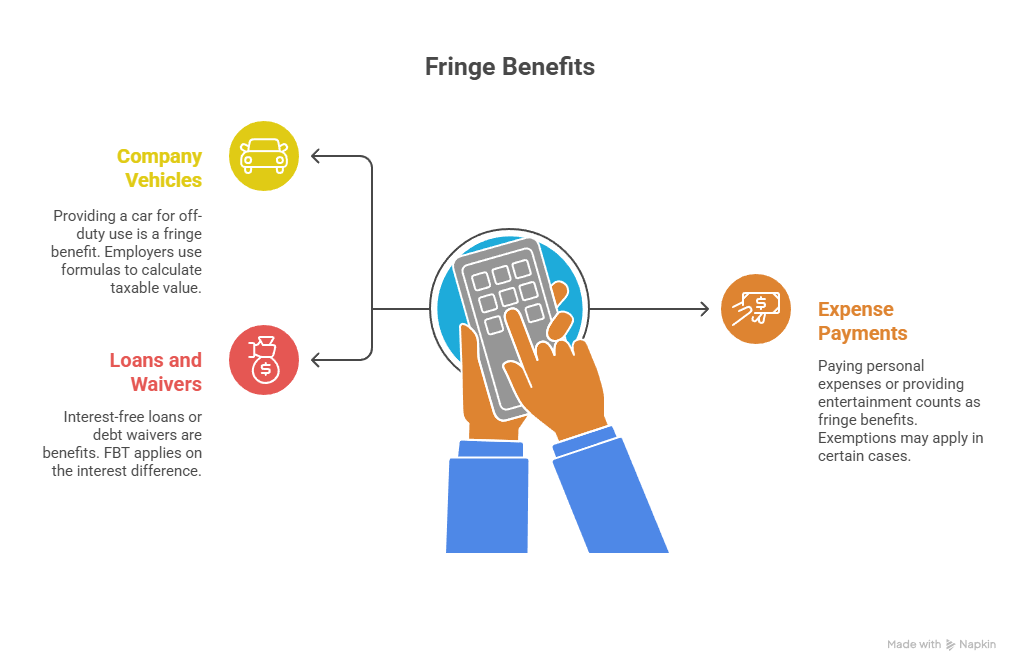

Some common examples of fringe benefits include:

- Company vehicles for private use: If you provide a car that an employee can use off-duty (commuting or personal trips), this is a fringe benefit. Employers commonly use the statutory formula or operating cost method to calculate the taxable value for FBT.

- Expense payments & entertainment: If your business pays an employee’s personal expenses (e.g. private bills) or provides entertainment (concert tickets, holiday stays, meals or drinks), these generally count as fringe benefits unless specifically exempt (for example, under the minor benefits exemption).

- Loans and debt waivers: An interest-free or low-interest loan to an employee is a benefit. FBT may apply on the difference between the interest the employee actually paid and the interest they would have paid at the benchmark rate. Similarly, if you forgive an employee’s debt, it’s treated as a fringe benefit.

The ATO categorises fringe benefits into many types (car benefits, loan benefits, expense payment benefits, etc.), each with specific valuation rules. As an employer, you must calculate the taxable value for all benefits you’ve provided in the FBT year, then apply the gross-up and FBT rate. FBT is reported and paid annually – most employers have an FBT return due by 21 May each year (or later if using a tax agent’s FBT program).

Key FBT Exemptions and Concessions

Not all benefits are taxable. There are important exemptions and reductions that can save employers FBT:

- Minor benefits exemption: A benefit valued at under $300 (and provided infrequently) is generally exempt from FBT. For example, giving an employee a $250 gift card for a special occasion would usually be exempt, provided such gifts are not routine.

- Work-related items: Some items employees use primarily for work are FBT-free, such as a portable laptop or tablet, protective clothing, tools of trade, or an eligible work phone. These are exempt if primarily for business use and generally one item per employee per year (items that are similar).

- Electric cars and novated leases: New legislation has made certain electric cars FBT-exempt if they meet eligibility criteria (this took effect from the FBT year starting April 2022). This change has made novated lease packages for electric vehicles particularly attractive – we explore the details in our FBT and novated leases guide.

- Employee contributions: An employee can reduce the FBT on a benefit by making an after-tax contribution. For instance, if an employee pays for some of their company car’s operating costs directly, those payments offset the FBT liability on the car benefit.

It’s important to maintain good documentation to substantiate any exemptions or reductions you claim. For example, keep invoices and usage logs for work-related item exemptions, and ensure you have declarations from employees where required (such as stating they used a provided item primarily for work).

Reporting and Impacts on Employees

While employees don’t pay FBT, they should be aware of reportable fringe benefits. If an employee receives more than $2,000 in taxable fringe benefits (total taxable value before gross-up) in an FBT year, you as the employer must record a Reportable Fringe Benefits Amount (RFBA) on their end-of-year income statement or PAYG summary. This amount (grossed-up) doesn’t count as income for income tax, but it is used in determining eligibility for certain government benefits and tax offsets (for example, it can affect liability for the Medicare levy surcharge or family tax benefits).

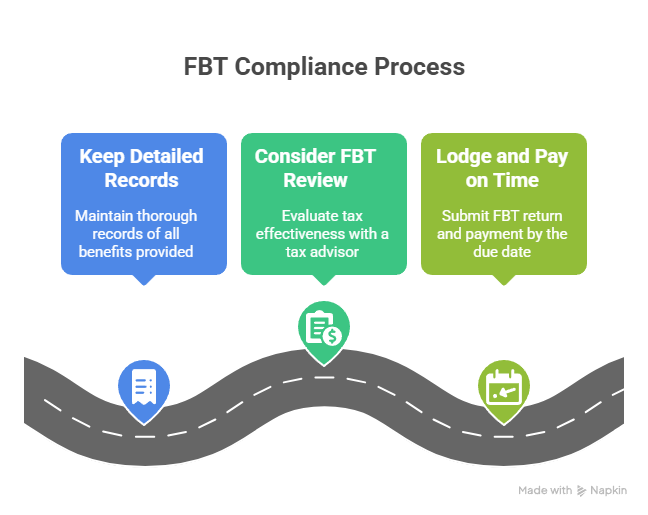

Managing FBT Compliance

FBT can be complex, given the various categories and valuation rules. To manage your obligations:

- Keep detailed records of all benefits provided – including receipts, employee declarations, logbooks for car usage, and any calculations you’ve made.

- Consider an FBT review or consulting a tax adviser annually. They may identify ways to restructure benefits to be more tax-effective – for instance, providing an equivalent exempt benefit instead of a taxable one.

- Lodge and pay on time: The FBT year ends 31 March. Ensure you lodge your FBT return and pay by the due date (usually 21 May) to avoid penalties.

Fringe Benefits Tax is an additional cost of providing generous perks to staff, but with careful planning you can minimize its impact. By understanding which benefits attract FBT and utilizing available exemptions, employers can offer attractive remuneration packages while managing the tax effectively.

Master FBT compliance with ease. Employers get key insights. TTS & Associates can support you—Contact Us