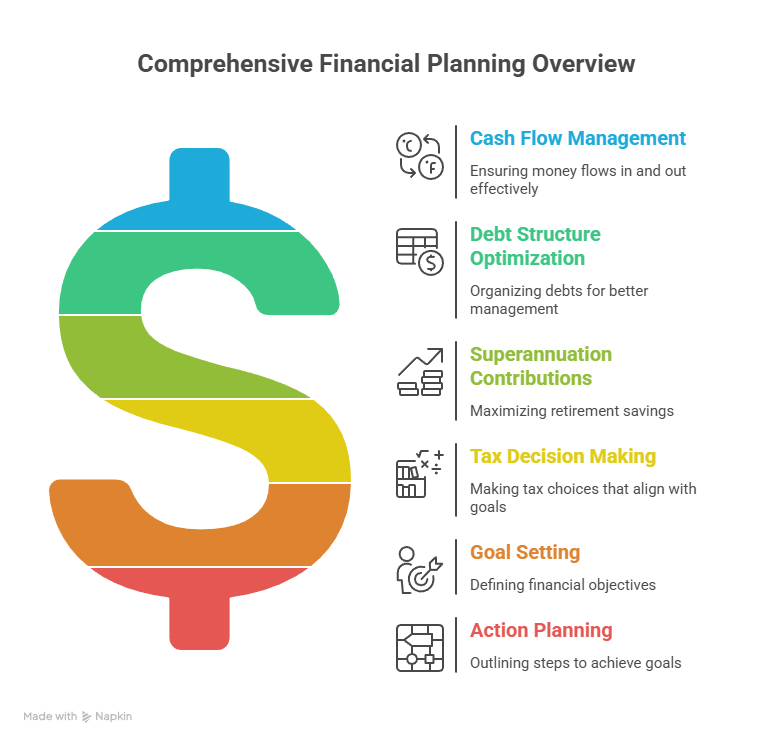

Financial Planning isn’t just about investments. For many Australians, the biggest levers are much more practical: cash flow, debt structure, super contributions, and making sure tax decisions don’t undermine the bigger picture. Done well, a plan helps you understand where you are now, what you want to achieve, and which actions matter most over the next 12–24 months.

This article outlines a plain-English Financial Planning framework, with a tax-aware lens. It’s general information, not personal financial advice.

Start with goals you can measure

Good plans begin with clear goals. “I want to be better with money” is a feeling, not a target.

Write down:

- what you want to achieve (e.g., buy a home, fund a child’s education, retire with a certain income)

- a timeframe for each goal

- a rough dollar figure where possible

ASIC’s MoneySmart suggests setting goals and matching them to time horizons (short, medium, long) as a way to structure decisions (see MoneySmart – develop an investing plan).

Get your baseline: income, expenses, assets, and debts

Before you “optimise”, you need a baseline. Gather:

- recent payslips or business income summaries

- bank and credit card statements

- loan balances and interest rates

- superannuation balances and contributions

- insurance and major recurring bills

Turn this into a one-page snapshot: net worth (assets minus debts) and monthly cash flow (income minus living costs). If you’re running a business, separate business and personal cash flow so tax and GST don’t get muddled.

Build a cash flow system that survives real life

A plan should still work when life gets messy: a slow business month, a car repair, a family emergency.

A simple system often includes:

- a “bills” account (rent/mortgage, utilities, insurance)

- a “buffer” account (3–6 months of essential expenses, if feasible)

- a “tax and super” set-aside (particularly for sole traders and investors)

If your cash flow is business-linked, aligning BAS and PAYG cycles with budgeting can make the whole plan more stable. You might find these guides useful:Hire a BAS agent – key benefits and Strategic tax planning.

Understand the tax ‘knock-on effects’ of big decisions

Tax is rarely the main reason to do something, but it can change the outcome.

Common examples:

- Investments: interest, dividends, capital gains, and deductions all affect after-tax returns.

- Property: cash flow and tax deductions are different from long-term capital growth.

- Structures: sole trader vs company vs trust can affect tax rates, asset protection, and admin burden.

- Super: contributions can be tax-effective, but caps apply.

For super contributions, the ATO sets annual caps and explains how contributions are taxed (see ATO – contributions caps and ATO – caps, limits and tax on contributions).

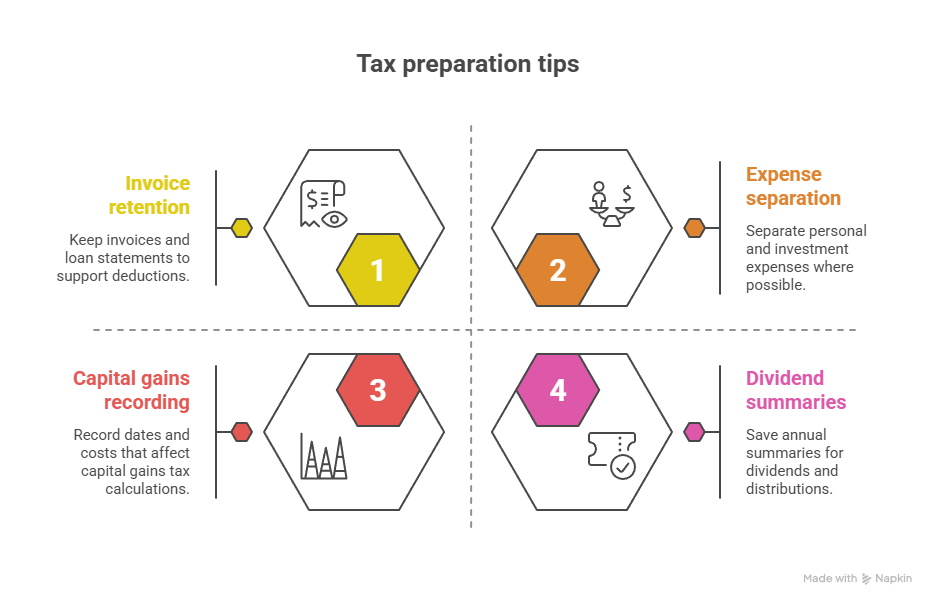

Keep the paperwork in step with the decisions

A plan can fall apart if the documentation lags behind. Two people can make the same decision (for example, buying a rental property) and get different outcomes because one keeps clean records and the other doesn’t.

Practical habits include:

- keeping invoices and loan statements that support deductions

- separating personal and investment expenses where possible

- recording dates and costs that affect capital gains tax calculations

- saving annual summaries for dividends and distributions

The ATO focuses on record keeping because it underpins what you claim and what you report (see ATO – record keeping). If you’re not sure what to keep, ask early—reconstructing documents later is time-consuming.

Don’t ignore succession and estate basics

Even simple planning should consider what happens if you can’t work, or if something happens to you. Insurance can cover some risks, but you should also think about:

- wills and powers of attorney

- business succession arrangements (for business owners)

- superannuation beneficiary nominations and how they fit your estate

These topics sit at the intersection of tax, legal structure, and family outcomes. If you’re a business owner, you may find this guide useful: Succession planning plan.

Decide what help you need, and what it should cost

Some people want a plan they can execute themselves. Others want structured support.

In Australia, “financial advice” is regulated. If you’re seeking personal advice on financial products (like super or investments), make sure the adviser is properly authorised and check their details on the public register (see ASIC – Financial Advisers Register and MoneySmart – financial advice).

Separately, tax planning and compliance support can help you avoid common mistakes and make sure decisions are recorded correctly. If you’re considering trusts, this overview may help clarify terminology: Trust setup Australia.

Build the plan around actions, not documents

The best Financial Planning outcomes come from small, consistent actions:

- automate savings and tax set-asides

- review insurance annually

- check super fees and investment options periodically

- track high-impact spending categories

- plan major purchases with tax timing in mind

Set one review date each quarter to update your assumptions. A plan that’s reviewed beats a plan that’s “perfect”.

General information only – seek professional advice before acting.