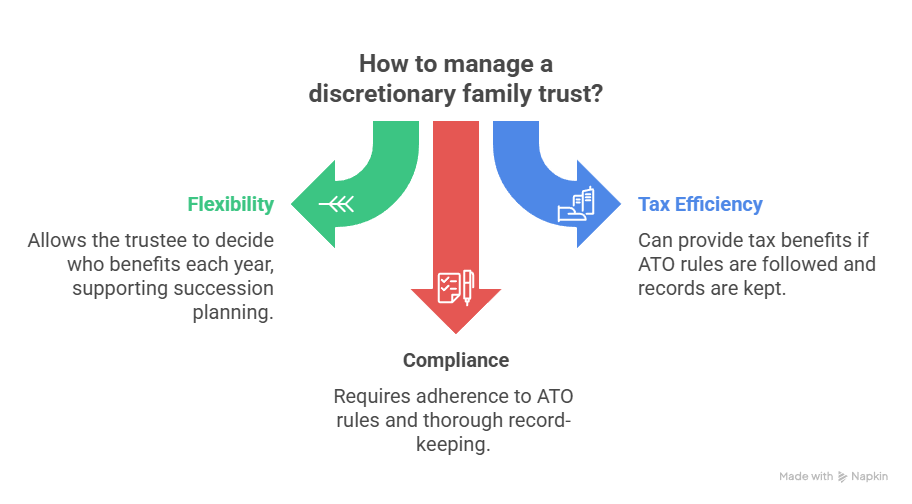

A discretionary family trust is a flexible way to hold investments or run a business while allowing the trustee to decide who benefits each year. It can support succession planning and, in the right circumstances, tax efficiency—provided you follow the ATO’s rules and keep thorough records. Here’s a practical guide to how these trusts work, current compliance themes, and simple steps to stay on track.

What “discretionary” means in practice

In a discretionary trust, the trustee chooses how to distribute income and capital among beneficiaries each year, within the deed’s rules. Many families also make a Family Trust Election (FTE) for tax purposes. An FTE unlocks concessions (like loss tracing and franking-credit integrity) but narrows who you can distribute to without extra tax.

Core setup steps that matter later

- Draft a deed that defines beneficiaries, trustee powers and appointor rights.

- Choose a corporate trustee if you want simpler succession and asset titling.

- Obtain the trust’s TFN and ABN if carrying on an enterprise, open a dedicated bank account, and map your ledger to trust-tax return labels (see Trusts—registration and reporting).

- Minute trustee resolutions on or before 30 June (or the deed’s earlier date) to make beneficiaries presently entitled to income (see Tax issues for trusts – tips and traps).

Distributing to family members—guardrails to respect

The ATO’s compliance focus includes section 100A “reimbursement agreements”, where someone other than the beneficiary enjoys the benefit of a distribution. The ATO’s PCG 2022/2 explains risk zones and expected documentation—essential reading for trustees and advisers. If minors are beneficiaries, remember Division 6AA imposes higher tax on most unearned income, with limited exceptions.

Streaming franked dividends and capital gains

Where your deed allows, you can “stream” franked dividends and capital gains to specific beneficiaries—provided you resolve correctly and keep contemporaneous records. The ATO’s guidance sets out timing and documentation expectations for franked distributions and capital gains.

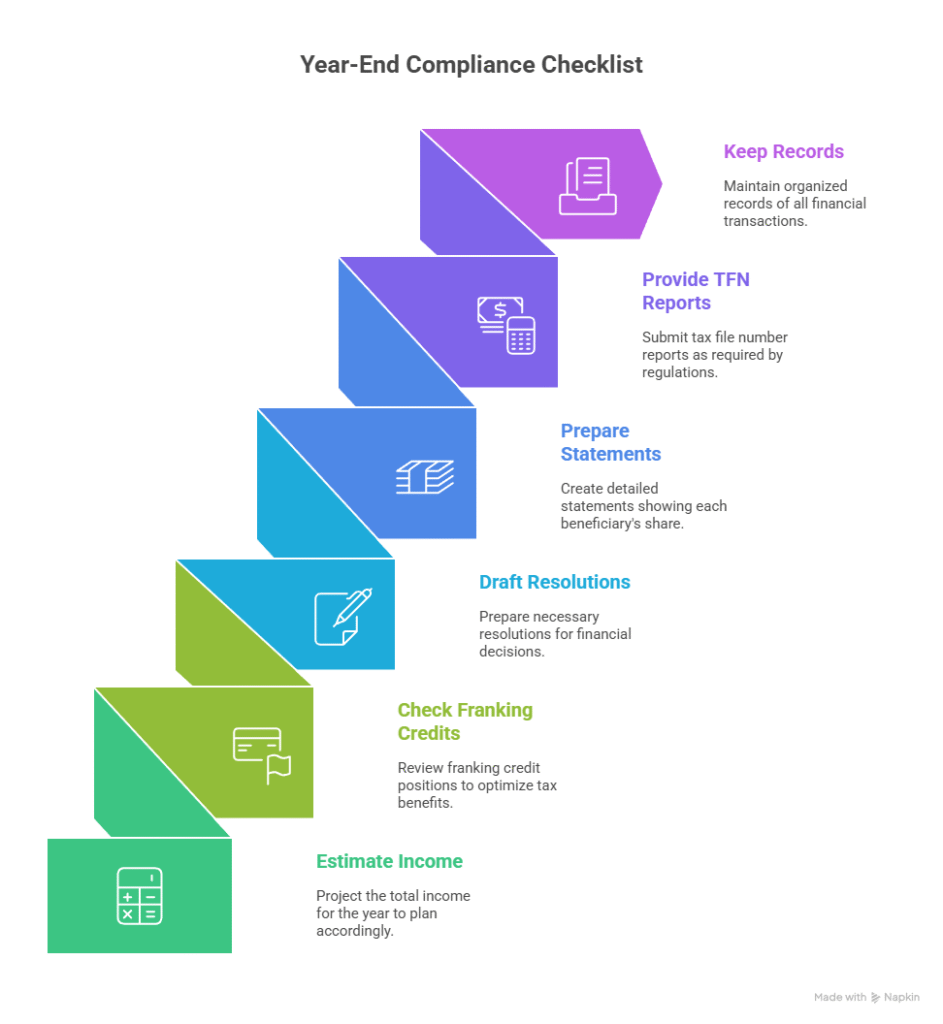

Practical compliance routines

- Before 30 June: estimate income, check franking-credit positions, and draft resolutions.

- After year-end: prepare statements showing each beneficiary’s share; provide TFN reports where required.

- Records: keep source documents for dividends, gains and any inter-entity distributions.

TTS & Associates explains setup sequencing and documentation in How to Set Up a Trust in Australia and Trust Setup: Simple Steps.

When a company or direct ownership might be simpler

If you hold a single asset with stable income (for example, one parcel of dividend-paying shares), a company or direct ownership may be administratively lighter. Trusts shine when you need flexibility, succession options, or plan to admit family members over time.

Key takeaways for trustees

- Understand your deed and minute decisions clearly.

- Consider whether an FTE is worthwhile and maintain a “family group” register (see How to make an FTE).

- Stay within the PCG 2022/2 framework for Section 100A (ATO guidance).

- Plan distributions with minors’ tax rules in mind (Division 6AA).

Handled well, a discretionary family trust can be a robust long-term structure—so long as the paperwork and tax settings match the strategy. Call TTS & Associates to discuss options that best fit your goals.

General information only – seek professional advice before acting.