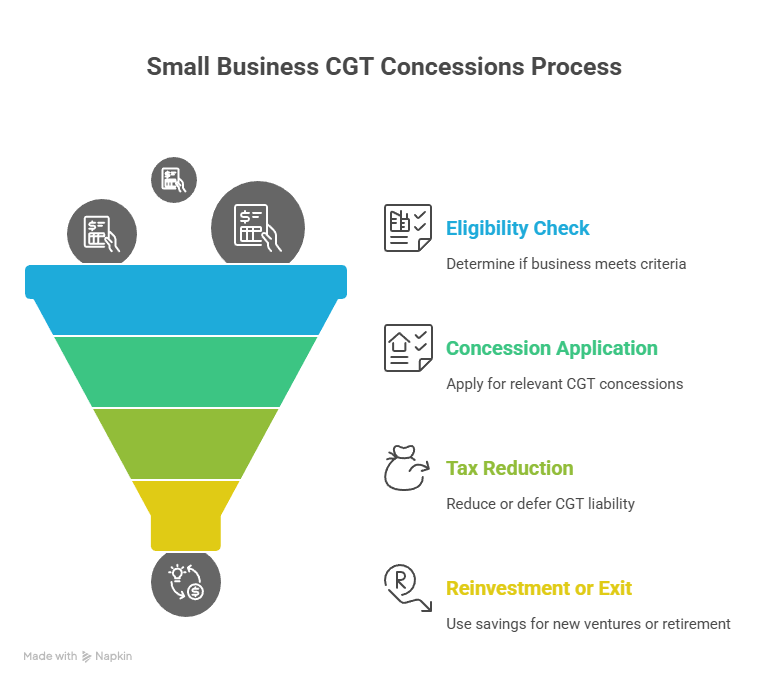

Selling your business or a business asset triggers capital gains tax (CGT), but the capital gains small business concessions can reduce, defer or even eliminate the bill. If you meet the eligibility tests, these concessions reshape after-tax outcomes and help you reinvest or exit on cleaner terms. (see ATO: Small business CGT concessions). (Australian Taxation Office)

First, confirm you’re eligible

Eligibility sits on several pillars: you must be a small business entity (generally turnover < $2m) or pass the $6m net asset test; the asset must be an active asset; and extra rules apply if the owner is a company or trust. The ATO’s overview sets out each threshold and how they interact (see Eligibility conditions). (Australian Taxation Office)

The four concessions at a glance

Once you meet the basic conditions, four reliefs may apply:

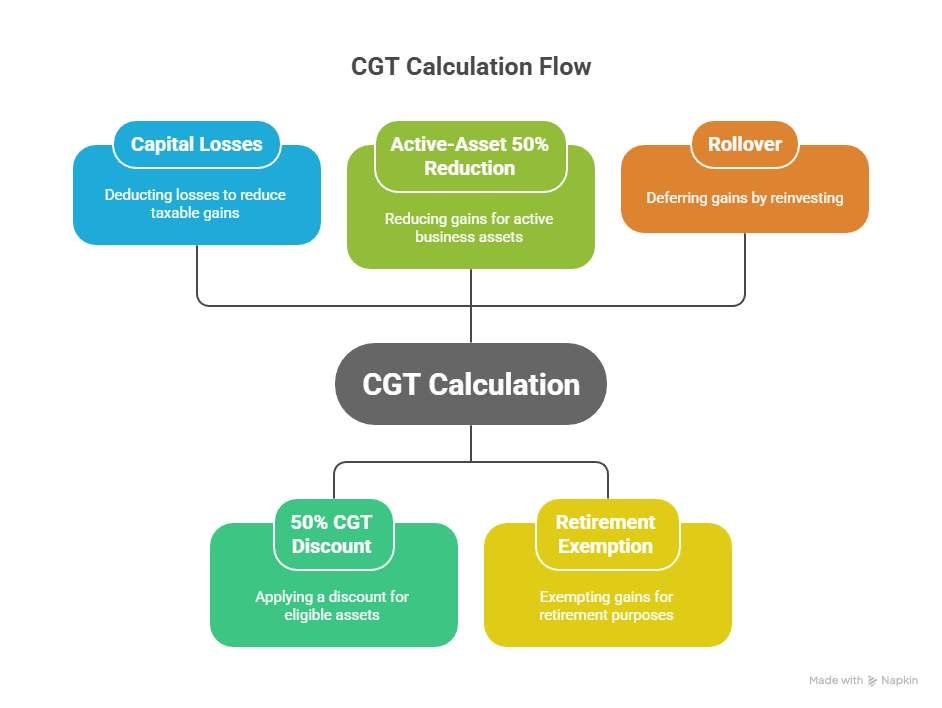

- 15-year exemption: if you’ve owned the active asset for at least 15 years and meet retirement age/conditions, the entire gain can be disregarded.

- 50% active asset reduction: halves the remaining gain after losses and any 50% CGT discount (if available).

- Retirement exemption: lets you disregard up to a lifetime cap if proceeds go to retirement (extra rules for companies/trusts).

- Rollover: defers the gain if you buy a replacement active asset within the time window.

These are summarised in the ATO’s guide to concessions (see ATO: Small business CGT concessions). (Australian Taxation Office)

Ordering matters—work through the sequence

CGT calculations have a strict order: apply capital losses, then the 50% CGT discount (if eligible), then the active-asset 50% reduction, then the retirement exemption or rollover. Following the ATO’s sequence ensures you don’t leave value on the table (see ATO: Applying concessions). (Australian Taxation Office)

Active asset test: don’t assume, prove it

To qualify, the asset must be used or held ready for use in the business for a minimum period. Shares or units require extra checks (significant individual, CGT concession stakeholder). Keep evidence—leases, usage logs, or board minutes—to show the asset’s business role (see ATO: Eligibility conditions). (Australian Taxation Office)

Practical planning tips

- Start early: model eligibility before signing a contract. Small tweaks (ownership percentage, timing) can be decisive.

- Document purpose: keep contemporaneous notes about how the asset supports business activity.

- Align with retirement goals: if using the retirement exemption, track lifetime caps and payment timing carefully.

Case sketch: owner sells a workshop

A sole trader sells a workshop used in their panel-beating business for 16 years. After losses, they apply the 50% CGT discount (held >12 months), then the 50% active asset reduction, and finally the 15-year exemption may fully shelter the gain if conditions are met. The order materially changes the number—walk through it line by line using the ATO checklist. (Australian Taxation Office)

Records and lodgement rhythm

Strong records make claims robust: contracts of sale, valuations, asset registers, trust/company minutes and ownership evidence. Pair this with a clean BAS and tax workflow; our guides Online BAS Lodgement and Business Activity Statement Due Dates Explained help keep the admin tidy.

When to seek advice

Concessions can interact in complex ways—especially for trusts, interposed entities and earn-outs. If you’re even close to the thresholds, a review by a specialist can pay for itself.

In short, the small business CGT concessions provide a structured pathway to reduce, defer or eliminate CGT—if you can prove eligibility and follow the order precisely (ATO eligibility overview). (Australian Taxation Office)

General information only – seek professional advice before acting.