When you inherit a home, you don’t usually pay CGT at the time you receive it. Tax may arise if and when you sell, and the rules depend on dates, use and whether you sell within 2 years. Understanding capital gains inherited property rules helps you decide whether to sell, hold, or move in. The ATO’s pages outline the framework clearly (see Inherited property and CGT). (Australian Taxation Office)

The two-year window

If you dispose of the property within 2 years of the deceased’s death, a full exemption can apply in many common scenarios (for example, when the property was the deceased’s main residence and not used to produce income). If circumstances delay the sale, the ATO can allow extensions where conditions are met (see Extensions to the 2-year ownership period). (Australian Taxation Office)

If you sell after two years

A partial exemption may apply. You’ll apportion the gain between exempt and taxable periods, considering use as a main residence vs rental. The ATO provides worked examples for calculating a partial exemption (see Calculating a partial exemption). (Australian Taxation Office)

Cost base and acquisition date

If the deceased acquired the home before 20 September 1985, you are taken to have acquired it at the date of death at market value. If they acquired it after that date, you inherit their cost base (with adjustments). Either way, documents matter: title details, valuations, and records of improvements (see How CGT applies to inherited assets). (Australian Taxation Office)

Living in the property after inheritance

Move in and make it your main residence, and future use can influence CGT when you sell. If you later rent it, main-residence rules and absence choices will affect apportionment. Keep a clear timeline and note any periods of income-producing use.

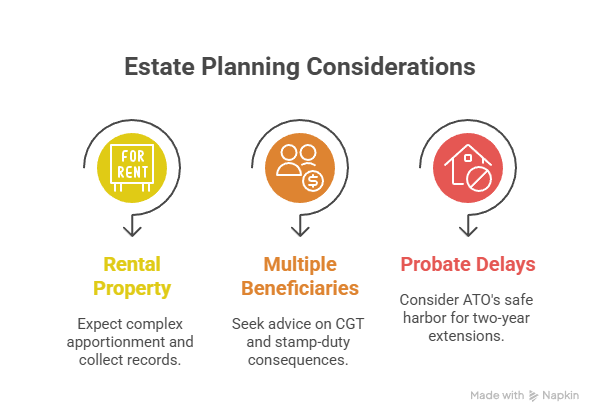

Common scenarios and what to check

- House was rented at death: expect a more complex apportionment; collect agent statements and lease records.

- Multiple beneficiaries: a deed of partition or sale to one beneficiary can have CGT and stamp-duty consequences—seek advice before signing.

- Delays from probate or renovations: consider the ATO’s safe harbour for exceptional circumstances when seeking a two-year extension (ATO extension guidance). (Australian Taxation Office)

Records to assemble now

- Probate documents, will extracts and title records.

- Market valuation at date of death (if pre-CGT acquisition).

- Invoices for capital improvements and selling costs.

- Rental schedules if the property was or becomes income-producing.

For help packaging evidence and modelling outcomes, see our Property Investment Accountant article.

Decision pathway

- Can you sell within 2 years? If so, check if a full exemption applies.

- If not, model partial exemption vs moving in.

- Gather documents early; valuations are easier near the relevant dates.

- Keep your workings with the return in case of ATO follow-up.

Handled early and documented well, capital gains inherited property outcomes can be optimised within the ATO’s framework. (Australian Taxation Office)

General information only – seek professional advice before acting.