If you’re searching “capital gains how much”, you’re really asking two things: how the gain is calculated and which rate applies. In Australia, capital gains tax (CGT) is not a separate tax—your net capital gain is added to your taxable income and taxed at your marginal rates. The ATO sets the calculation rules (cost base, CGT events, discounts and exemptions), and getting each step right determines how much you actually pay (ATO CGT overview).

Step 1: Work out the gain (and the right cost base)

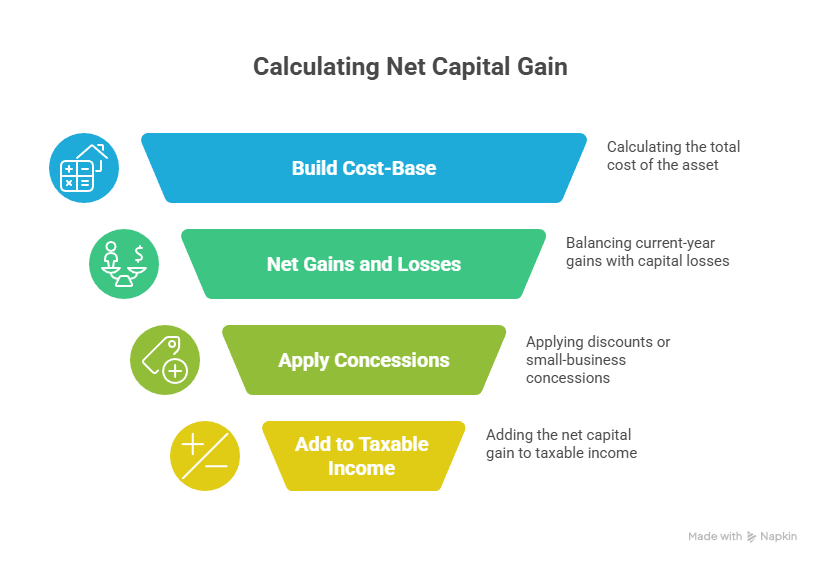

Start by identifying the CGT event—usually a sale, but it can also be a gift, a compulsory acquisition or certain restructures. Your capital gain equals your sale proceeds minus the cost base: purchase price plus eligible costs such as stamp duty, legal fees, and some improvements. Careful record-keeping matters, because missing cost-base items means overstating your gain (ATO: Capital gains tax).

If you’ve owned the asset for less than 12 months, you typically use the other method (no discount). For 12 months or more, you can generally apply the discount method after netting gains and losses (ATO: CGT discount).

Step 2: Apply losses before any discount

Offset any capital losses (current year or carried forward) against your capital gains. Only after losses are applied do you consider the CGT discount. This sequencing can change the answer materially—especially in years with market volatility. The ATO’s guide walks through loss ordering and examples (ATO CGT overview).

Step 3: Check if a discount applies

Individuals and trusts that have held the asset for 12 months or more often qualify for the 50% CGT discount (some assets and situations differ; foreign residents have limited access). Companies don’t get the 50% discount. The discount converts a $40,000 gain into a $20,000 net capital gain, which is then taxed at your marginal rate (ATO: CGT discount; CGT discount for foreign residents).

Property specifics: main residence and rentals

Your main residence is generally CGT-free while you live in it. If you move out and rent it, you may still treat it as your main residence for up to six years (the “six-year rule”) provided certain conditions are met; beyond that, part of any gain can be taxable. The ATO’s pages provide worked examples so you can estimate the taxable portion (ATO: Your main residence; Treating former home as main residence).

If you sell a rental property, you’ll compute the gain, apply eligible capital works and improvement costs to the cost base, and—if held 12+ months—apply the discount. See the ATO’s rental sale example for how figures flow (ATO: CGT when selling your rental property).

Small business? Consider Division 152 concessions

Selling a business or business asset? You may be eligible for small business CGT concessions—the 15-year exemption, 50% active-asset reduction, retirement exemption and roll-over—if you meet basic conditions (turnover or net-asset tests, active-asset test, and significant individual rules). These concessions can reduce, defer or eliminate the gain (ATO: Small business CGT concessions; Eligibility overview).

“Capital gains how much?”—a quick estimation roadmap

- Identify the event and estimate proceeds (contract price less selling costs).

- Build a cost-base: purchase price + stamp duty + legal + non-deducted improvements.

- Net current-year gains with capital losses.

- Apply any discount or small-business concessions.

- The net capital gain is added to taxable income and taxed at marginal rates.

To keep numbers tidy, adopt a monthly reconciliation habit and document improvements. Where clients need help with the CGT record-trail (especially around property and BAS interactions), our explainer on Online BAS Lodgement and Quarterly BAS Dates offers a clean workflow.

Common traps and how to avoid them

- Missing cost-base items: Keep settlement statements, invoices and QS reports for improvements.

- Wrong discount timing: The 12-month clock is contract to contract, not settlement to settlement.

- Ignoring the main-residence choices: If you own two properties in a year, you may need an election—model both outcomes first.

- Overlooking small-business eligibility: The concessions are powerful but technical; confirm tests early.

For property investors, our Property Investment Accountant article shows how to build an evidence file that survives ATO review.

In short, the answer to “capital gains how much” depends on your records, holding period and eligibility for discounts or concessions. Use the ATO pages linked above as your rulebook and map your numbers to those steps before you sell.

General information only – seek professional advice before acting.