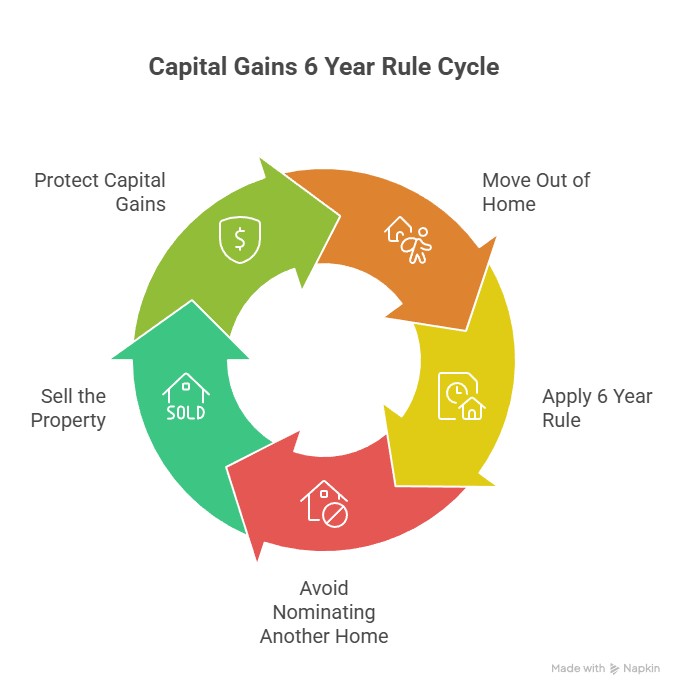

If you rent out your former home, the capital gains 6 year rule can protect some or all of your gain when you sell. The rule lets you treat the property as your main residence for up to six years after you move out, provided you don’t nominate another home as your main residence during that time (see ATO: Treating former home as main residence). (Australian Taxation Office)

The core idea

Your home is generally CGT-free. Once you move out and rent it, the six-year absence choice can extend that exemption. If you sell within the six-year window, the gain may be fully exempt; if you hold longer, the ATO requires an apportionment between exempt and taxable days (see ATO: Your main residence – home). (Australian Taxation Office)

Timing nuances that trip people up

- The six years are cumulative periods of absence; move back in and the clock can reset.

- If you buy before you sell, you can treat both homes as your main residence for up to six months under specific conditions (see Moving to a new main residence). (Australian Taxation Office)

- Short private use during rental periods can affect apportionment—keep a diary and utility evidence.

How to choose wisely

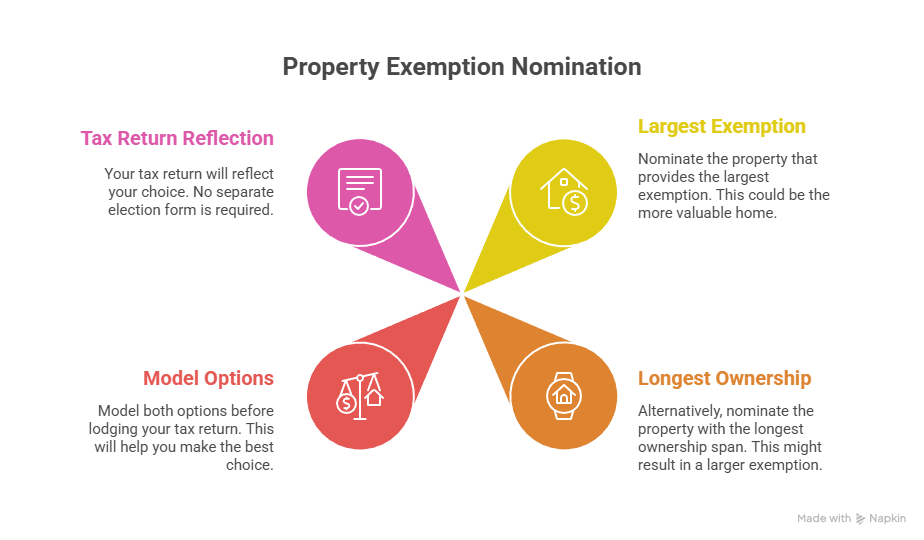

You usually nominate the property that gives the largest exemption. That might be the more valuable home or the one with the longest ownership span. Model both options before lodging your return; you don’t file a separate election form, but your tax return reflects your choice (see ATO: Treating former home as main residence). (Australian Taxation Office)

Working example (simplified)

You live in a unit for 3 years, move interstate and rent it for 5 years, then sell. If you treat it as your main residence while absent, only the final 2 rental years may be taxable. The ATO’s examples show how to apportion days and adjust the cost base for capital works and selling costs (main residence pages). (Australian Taxation Office)

Records to keep

- Settlement and contract dates (apportionment is date-based).

- Rental schedules and periods of vacancy.

- Evidence of private use (if any).

- Capital improvements (added to cost base for CGT).

For help organising files and CGT schedules, see our Property Investment Accountant guide.

Interactions with other rules

If you run a business from home or short-stay let a room, part of the property can become subject to CGT even before you move out. Review the ATO’s guidance on using your home for rental or business before you list (see ATO: Using your home for rental or business). (Australian Taxation Office)

Action list before you sell

- Map your residency timeline and potential six-year periods.

- Gather improvement invoices and agent statements.

- Model both nomination choices and keep your workings with your records.

- Lodge with a clear paper-trail in case the ATO asks questions.

Handled carefully, the capital gains 6 year rule can preserve the main-residence exemption long after you’ve moved out—provided your dates, documents and nomination logic line up with ATO guidance. (Australian Taxation Office)

General information only – seek professional advice before acting.