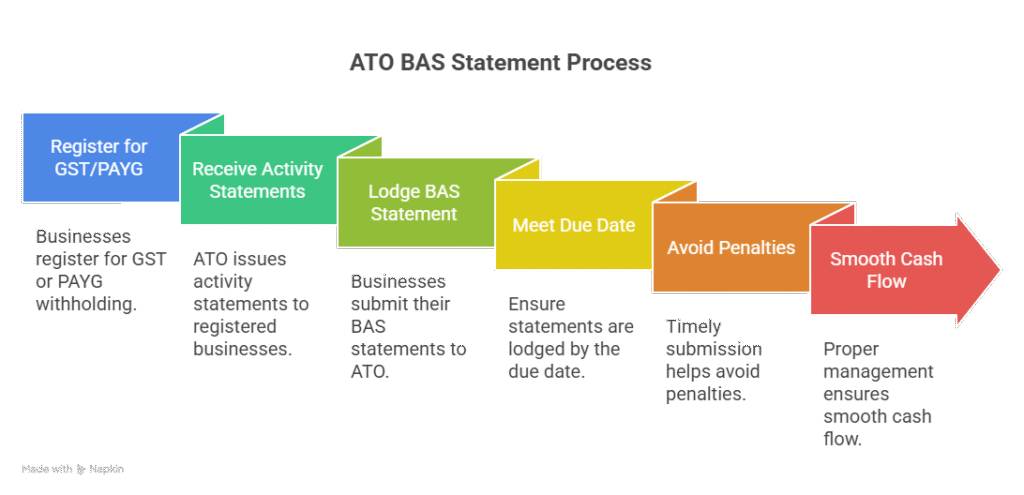

An ATO BAS statement is the Business Activity Statement you lodge with the Australian Taxation Office (ATO) to report Goods and Services Tax (GST), Pay As You Go (PAYG) withholding, PAYG instalments and selected other taxes.

If you’re registered for GST or withhold PAYG from wages, you’ll be issued activity statements and must lodge by the due date shown on each form. Getting the rhythm right helps you avoid penalties and smooth out cash flow throughout the year (see the ATO’s BAS overview).

What the ATO BAS statement covers

Think of the BAS as a single, periodic tax snapshot. It typically includes:

- GST labels – your sales (G1) and GST on sales (1A), and the GST credits you can claim on business purchases (1B).

- PAYG withholding – wages paid (W1) and tax withheld (W2).

- PAYG instalments – prepayments of your income tax, where applicable.

- Other items – such as luxury car tax, wine equalisation tax or fringe benefits tax (FBT) instalments, if relevant to your business.

Small businesses benefit from Simpler BAS, which limits what you need to code for GST while keeping the tax outcome the same. Correctly distinguishing taxable, GST-free and input-taxed supplies is still essential; the ATO’s Simpler BAS guide shows common treatments and examples. (See the ATO’s Simpler BAS GST bookkeeping guide.)

Who must lodge and how often

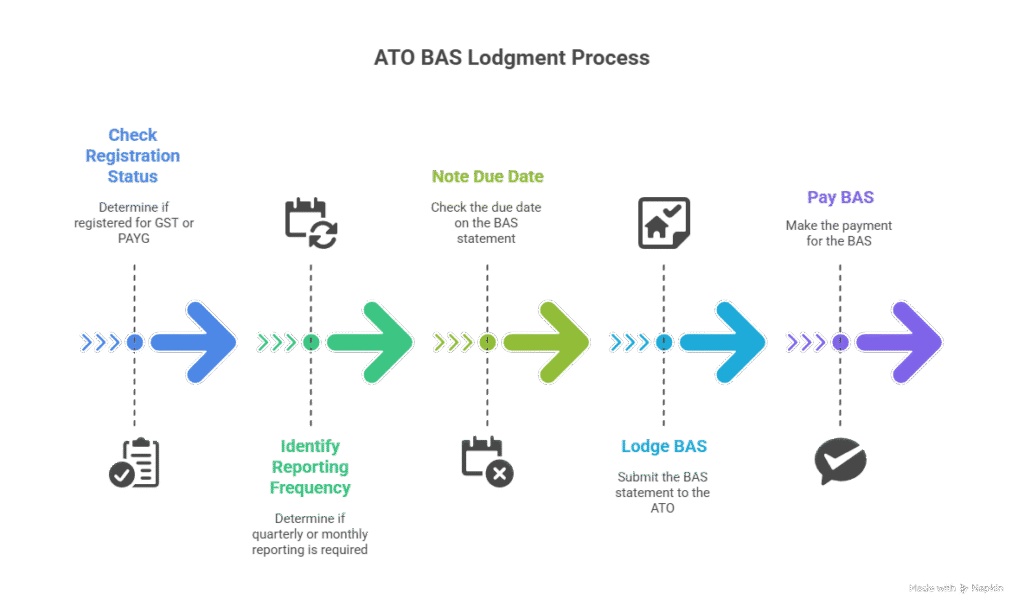

You must lodge an ATO BAS statement if you are registered for GST or have PAYG withholding or PAYG instalments obligations. The ATO assigns a reporting frequency based on size and risk profile: most small businesses lodge quarterly; larger or elected entities lodge monthly. Your due date is displayed on each BAS, and if it falls on a weekend or public holiday you can lodge and pay on the next business day. See the ATO’s current page on due dates for lodging and paying your BAS.

For a small-business walkthrough of the quarterly timetable and planning tips, TTS & Associates’ explainer on Quarterly BAS Due Dates is a handy companion.

Preparing an accurate BAS (and avoiding rework)

Build a simple month-end routine so quarter-end isn’t a scramble:

- Reconcile weekly. Match bank feeds and attach tax invoices.

- Review GST coding. Sense-check outliers (e.g., unusually high 1A or 1B).

- Check payroll. Align Single Touch Payroll (STP) summaries with W1/W2.

- Document adjustments. Private use, bad debts or discounts can require GST adjustments.

- Retain evidence. Keep invoices, payroll reports and the ATO lodgement receipt for at least five years.

If you’re new to lodgement, our step-by-step BAS Lodgement Simplified guide explains how to prepare, review and file confidently using Online services for business or SBR-enabled software.

Lodging and paying: methods and cash-flow tips

You can lodge your ATO BAS statement via Online services for business, through compliant accounting software, or via a registered BAS/tax agent. The payment due date usually matches the lodgement due date. Build a forecast that combines: net GST (1A minus 1B), any PAYG withholding, and PAYG instalments, then set funds aside progressively. If cash is tight, lodge on time anyway and set up a payment plan—staying on time with lodgement can help you avoid late-lodgement penalties, even if payment is staged (ATO guidance on due dates and payment options applies).

For a practical, software-based workflow, see Online BAS Lodgement: 5 Steps to Hassle-Free Filing.

If you miss a deadline: penalties and interest

Two charges can apply if you’re late:

- Failure to Lodge (FTL) penalty – calculated in 28-day increments using penalty units, scaled by entity size. Even a nil or credit BAS can attract FTL if lodgement is late. See the ATO page on Failure to lodge on time penalty for current rules.

- General Interest Charge (GIC) – daily interest on overdue amounts from the day after the due date until paid. Current rates are published quarterly (see GIC rates).

If you’re affected by events outside your control—serious illness, natural disaster or major system outage—contact the ATO or your agent promptly to request a deferral or remission. Early engagement generally means more options (ATO due-dates guidance).

Should you use a BAS accountant?

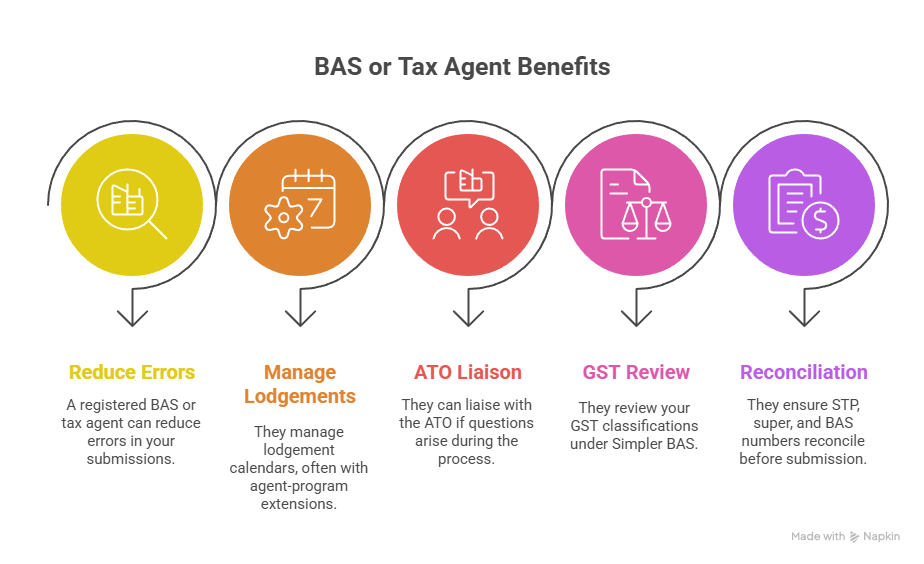

A registered BAS or tax agent can reduce errors, manage lodgement calendars (often with agent-program extensions), and liaise with the ATO if questions arise. They can also review your GST classifications under Simpler BAS and make sure STP, super and BAS numbers reconcile before submission. If you prefer expert support, explore our guide Hire a BAS Agent: Key Benefits for Your Business or get in touch with our team for compliant, on-time lodgements.

By treating each ATO BAS statement as part of a regular compliance rhythm—reconcile, review, lodge—you’ll stay ahead of deadlines and protect cash flow. Use the ATO pages above for authoritative rules and our linked how-to articles for practical implementation. If anything is unclear, ask a registered adviser before you lodge; a quick check now beats costly amendments later.

General information only – seek professional advice before acting.