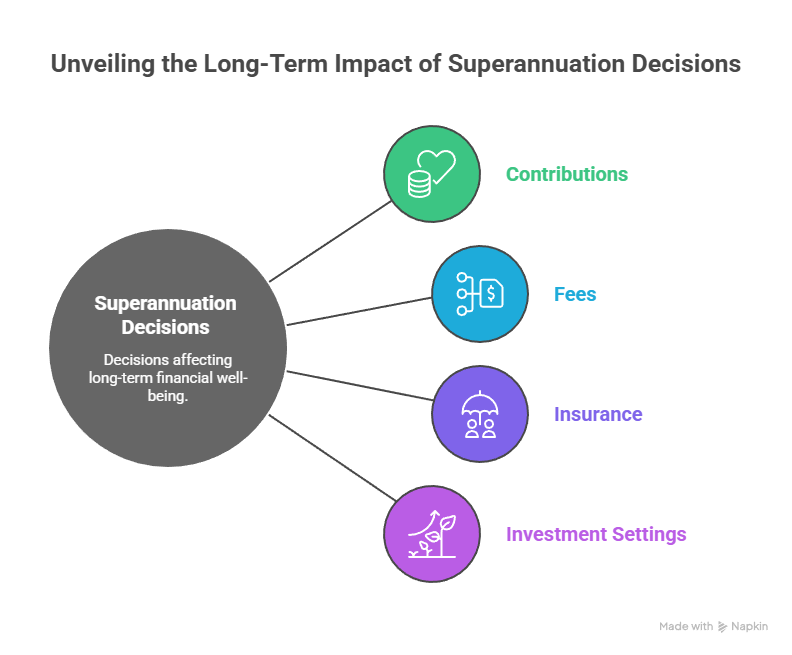

Superannuation decisions can have long tails. A small change in contributions, fees, insurance, or investment settings can compound over years—good or bad. That’s why many people look for a Financial Adviser Superannuation when they hit a major life event (new job, redundancy, business sale) or when retirement starts to feel “close enough to plan”.

This guide covers what super-focused advice typically involves in Australia, what’s regulated, and which tax and compliance points deserve attention. This article is general guidance and not personal financial advice.

First: know what’s regulated

Personal advice about financial products (including super funds and investments inside super) is regulated in Australia. Before acting on recommendations, check the adviser’s details and authorisations on the public register (see ASIC – Financial Advisers Register). MoneySmart also explains what financial advice is, and what you should receive in writing (see MoneySmart – financial advice).

Paperwork and reviews: what “good” looks like

Super advice should come with clear documentation. At a minimum, you should understand:

- who is providing the advice and how they’re paid

- what is in scope (and what isn’t)

- what changes will be implemented and when

- how often the strategy will be reviewed

If personal advice is provided, you should receive a Statement of Advice (SOA) that sets out recommendations, reasons, and costs (see MoneySmart – statement of advice). Ongoing reviews matter because super settings can drift as your income, employment, and goals change.

Contributions: the “easy” lever that still has rules

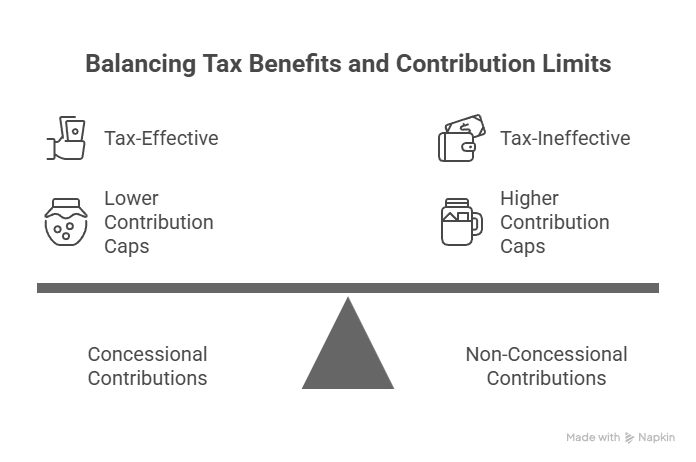

For many people, contributions are the highest-impact super lever because they change the amount that gets invested and may be tax-effective depending on circumstances. However, caps apply and should be checked before making decisions.

The ATO sets out the current concessional and non-concessional contribution caps and related thresholds (see ATO – contributions caps). A Financial Adviser Superannuation should be able to explain how contributions fit your cash flow and your broader tax position, without assuming “more is always better”.

Investment options and fees: what to compare

Investment choice matters, but fees and structure often matter just as much. Useful comparisons include:

- total fees (administration, investment, advice where applicable)

- diversification and risk level

- how often the portfolio is reviewed and rebalanced

- whether the option fits your timeframe (shorter vs longer)

Ask how the recommendation matches your risk tolerance and what would cause the recommendation to change. Also ask whether the advice is based on your whole financial position, or only what sits inside super.

Insurance inside super: useful, but not set-and-forget

Many Australians hold life, TPD (total and permanent disability), or income protection insurance inside super. It can be convenient, but it isn’t always the best fit.

Questions to ask:

- what cover you have today and what it costs

- whether definitions and exclusions match your needs

- what happens to cover if you change jobs or funds

- whether premium payments materially reduce your retirement balance

A good discussion here is about trade-offs: protection today versus retirement outcomes later.

SMSF vs retail/industry funds: understand the responsibilities

An SMSF can provide control and flexibility, but it also brings real obligations. Trustees are responsible for compliance, investment strategy, record keeping, and administration.

Start with responsibilities and costs, not marketing. The ATO provides guidance on trustee obligations and ongoing requirements (see ATO – Self-managed super funds). If you want a practical overview of setup and what’s involved, see our guide:Set up self managed super fund and our service page:Superannuation services.

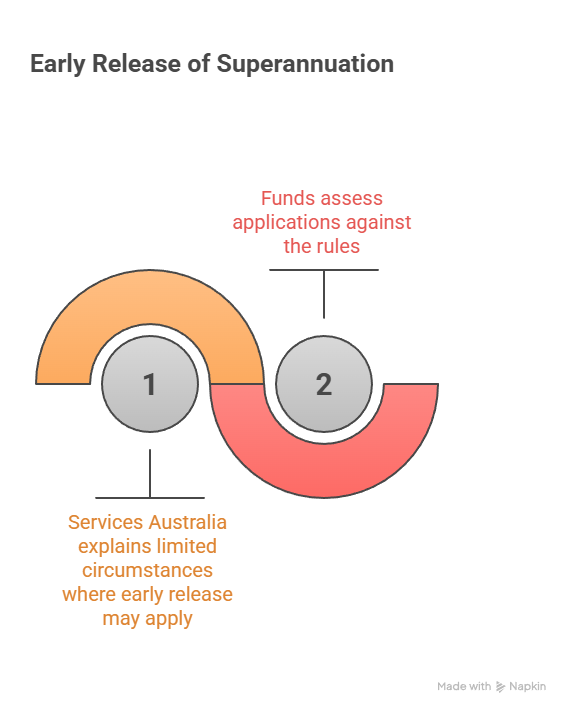

Early access: verify the rules before you act

“Early access” to super is limited and tightly controlled. If someone says you can withdraw super for a purpose that doesn’t match official criteria, treat it as a red flag.

Services Australia explains limited circumstances where early release may apply and notes that funds assess applications against the rules (see Services Australia – early release of superannuation). If you’re under pressure to act quickly, pause and confirm the criteria before providing personal details or signing anything.

How super advice should connect with your tax position

Super sits in a separate “system”, but it still interacts with tax:

- contributions have tax treatment and caps

- investment income inside super is treated differently from outside super

- changes to assets can trigger capital gains tax outside super

- timing decisions around 30 June can matter

If you’re a business owner or investor, super strategy should be aligned with your broader tax plan rather than handled in isolation. This overview can help frame that discussion: Strategic tax planning.

A checklist for your first meeting

To get value quickly, bring:

- your current super statement(s) and insurance details

- your contribution history (if available)

- an income estimate for this financial year

- planned changes (job change, property purchase, retirement timing)

- your main goal (retirement income, flexibility, protection)

A Financial Adviser Superannuation should explain recommendations in plain English, show how costs work, and coordinate with your accountant where tax and reporting are relevant. If anything is unclear, ask for a written summary and take time to review it before committing.

General information only – seek professional advice before acting.