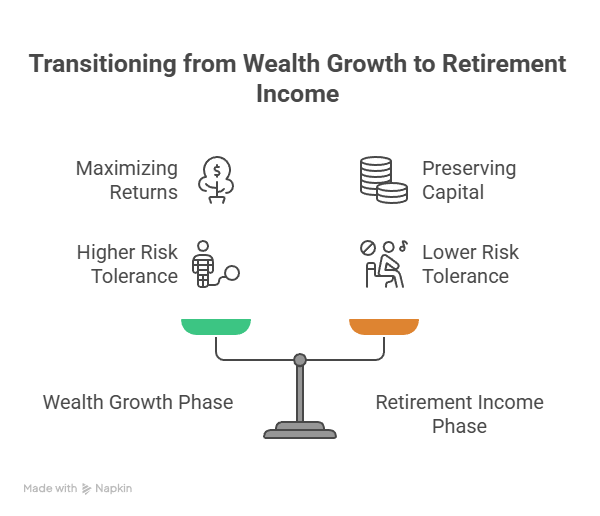

People usually look for a Financial Adviser Retirement when the question changes from “How do I grow wealth?” to “How do I turn savings into income without running out?” That shift brings new risks: sequencing (bad market years early), longevity, health costs, and the rules around super and government benefits.

This article explains what retirement-focused advice typically covers in Australia and the tax and paperwork issues worth raising early. This guide is general information and isn’t personal financial advice.

Start with the decision points that matter most

Retirement planning becomes simpler when you map the big decision points:

- when you plan to stop full-time work (and whether part-time work continues)

- when super becomes accessible based on preservation age and conditions

- what lifestyle spending you want to fund each year

- whether you plan to sell assets (home downsizing, investment property, business exit)

ASIC’s MoneySmart has guidance and calculators to help you structure a retirement plan (see MoneySmart – plan for your retirement).

Super access and income streams: know the basics

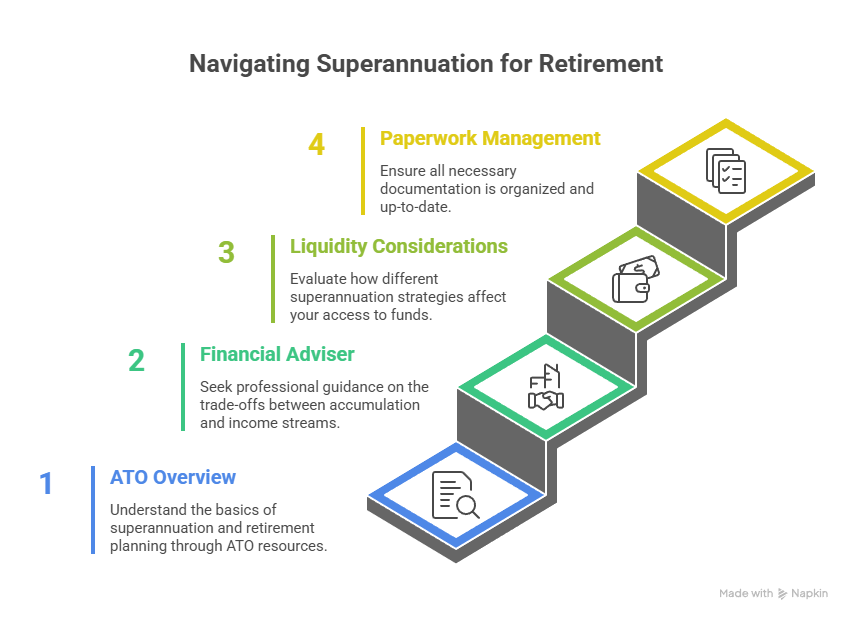

Super can be accessed only under certain conditions. Your preservation age and retirement status matter, and different rules can apply if you’re still working.

The ATO provides an overview of super access and planning considerations (see ATO – super and planning for retirement). A Financial Adviser Retirement should also explain the practical trade-offs between keeping money in accumulation, starting an income stream, and how this affects liquidity and paperwork.

Factor in Age Pension and deeming rules

Even if you don’t expect the Age Pension at the start of retirement, eligibility can change over time as assets and income shift.

Services Australia applies both an income test and an assets test, and financial assets may be assessed using deeming rules (see Services Australia – income test andServices Australia – assets test). A key planning goal is understanding which decisions may unintentionally reduce future flexibility.

Tax at retirement is different, not ‘gone’

Retirement doesn’t remove tax; it changes what drives it. Common issues include:

- taxable income from investment properties, dividends, or business income

- capital gains tax if you sell investments to fund retirement

- how different income sources interact with Medicare levy and offsets

- the timing of contributions and withdrawals around year-end

If super contributions are part of the strategy, caps apply and should be checked before acting (see ATO – contributions caps). For property or business owners, tax planning around asset sales can be as important as investment selection.

Sequence risk and spending plans: the “quiet killer”

Many retirees underestimate the impact of poor market returns early in retirement. Even if long-term average returns look fine, large withdrawals in bad years can permanently reduce the portfolio.

Practical ways people manage this (conceptually) include:

- keeping a cash bucket for 1–2 years of essential spending

- using a spending “floor” and a “flex” component

- reviewing drawdown rates annually rather than setting-and-forgetting

A good adviser should model scenarios and explain the assumptions in plain language.

Health and aged care: plan for uncertainty

Health costs are a common reason retirement budgets drift. Even if you’re fit now, it’s sensible to stress-test your plan for higher medical costs or the possibility of needing support services later.

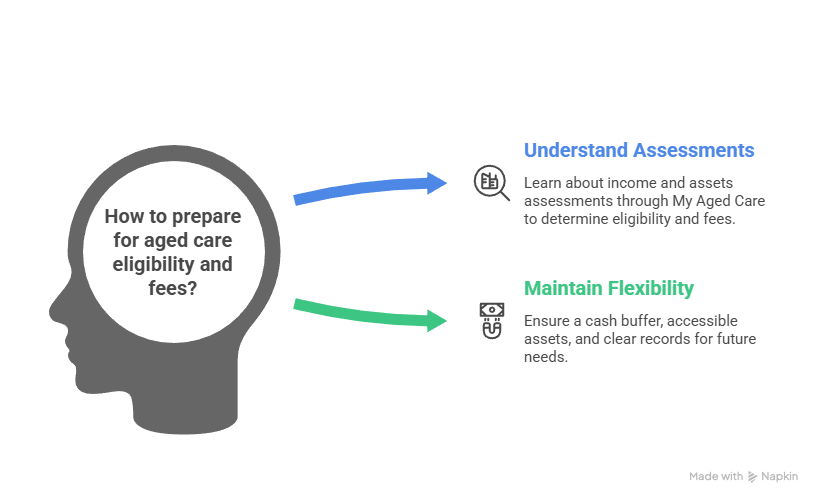

If aged care is a consideration, eligibility and fees often depend on income and assets assessments. My Aged Care explains how income and assets assessments work for support services (see My Aged Care – income and assets assessments). You don’t need to predict the future perfectly, but you do want enough flexibility (cash buffer, accessible assets, and clear records) to respond.

Documents and coordination: what a good process looks like

Retirement advice usually involves more paperwork than people expect. You should understand:

- what documents you will receive and keep (scope, fees, recommendations)

- who implements the changes and what the timing is

- how your accountant will be kept in the loop for tax reporting

If you’re also running a business, the retirement plan should line up with succession thinking. This guide may help: Succession planning plan.

Choosing the right professional (and checking credentials)

In Australia, personal advice about financial products is regulated. You can check an adviser’s details and authorisations on the public register (see ASIC – Financial Advisers Register). You should also ask what’s included in the service—one-off modelling, ongoing reviews, Centrelink guidance, or coordination with tax.

A short briefing sheet for your first meeting

To make the first meeting productive, bring:

- your latest super statements and contribution history

- a list of assets (with estimated values) and debts (with rates)

- your expected retirement date(s) and spending estimate

- notes on planned asset sales or major life changes

- your latest tax return (or business financials)

This helps a Financial Adviser Retirement focus on decisions rather than data chasing. The goal is a plan you can follow, review, and adapt as life changes.

General information only – seek professional advice before acting.