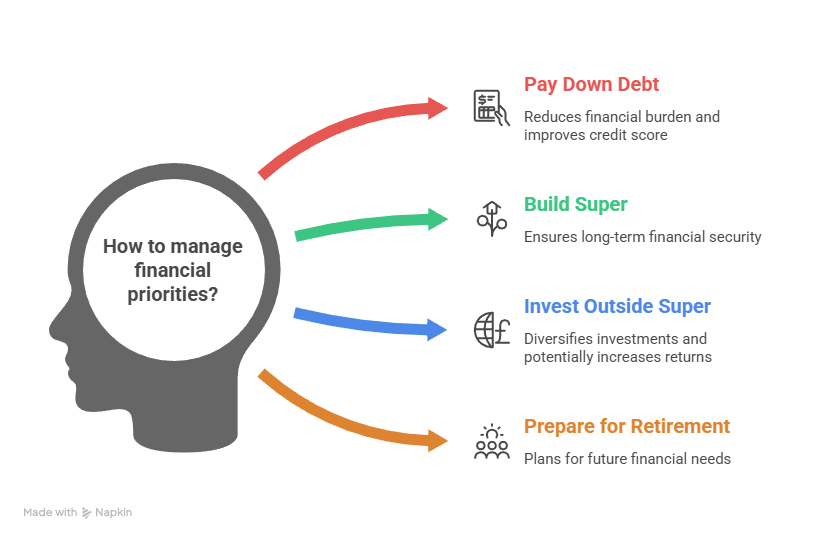

A Financial Adviser Melbourne can help you make sense of big financial choices—especially when there are competing priorities like paying down debt, building super, investing outside super, or preparing for retirement. The hard part is knowing what you’re paying for, what’s regulated, and how to spot advice that doesn’t match your situation.

This article sets out practical questions to ask and the tax-adjacent issues that are commonly overlooked. This article is general information and doesn’t consider your personal circumstances.

Know what “advice” means in Australia

In Australia, personal financial advice about products is regulated. That includes recommendations about super funds, investments, managed accounts, or insurance that are tailored to you.

Before you proceed, confirm the adviser’s details and authorisations on the public register (see ASIC – Financial Advisers Register). ASIC’s MoneySmart also explains the difference between general information and personal advice, and what you should receive in writing (see MoneySmart – financial advice).

Ask what they will (and won’t) cover

A common frustration is paying for a plan that doesn’t address the real problem. In your first meeting, ask for clarity on scope:

- retirement modelling and income strategies

- super contribution approach and insurance inside super

- investment selection and risk settings

- debt strategy and cash flow structure

- estate coordination and beneficiary nominations

If you mainly need tax and compliance support, you may not need product advice at all. If you do need product advice, make sure it’s clearly documented.

Understand the ‘best interests’ expectation in plain terms

Licensed advisers have duties and standards that shape how advice should be provided. In practice, you should expect:

- a fact-finding process (income, assets, goals, risk tolerance)

- a written explanation of recommendations and costs

- a clear link between your goals and the proposed strategy

If the recommendation arrives before the questions, that’s a red flag.

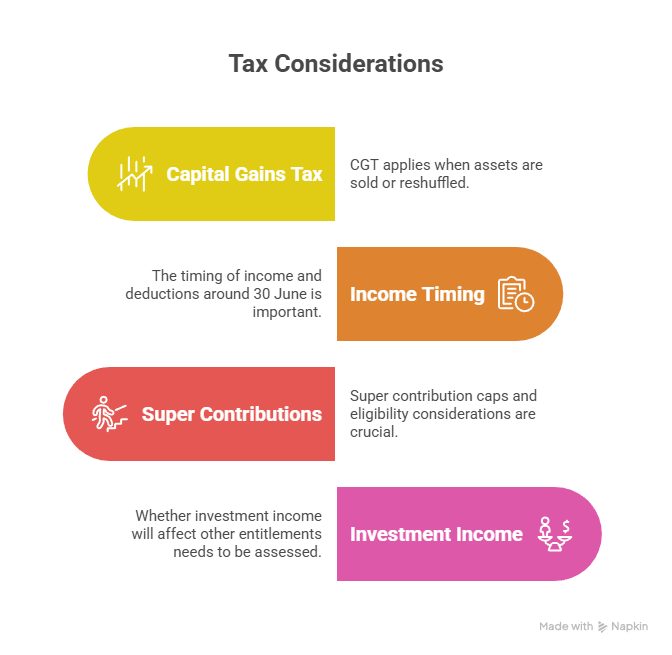

Build a tax checklist for the advice discussion

Even when advice is sound, tax can change the outcome. Bring these topics into the conversation early:

- capital gains tax (CGT) if existing assets are sold or reshuffled

- the timing of income and deductions around 30 June

- super contribution caps and eligibility considerations

- whether investment income will affect other entitlements

The ATO provides current contribution caps and thresholds that often matter when strategies involve super (see ATO – contributions caps). If you hold property or a business, also ask how the strategy interacts with your existing structure (company, trust, SMSF).

For a tax-focused overview of planning decisions, see: Tax planning in Australia.

Fees: focus on total cost and ongoing value

Ask for the total cost in the first year, including implementation. Then ask what you receive in year two and beyond.

Useful questions:

- Is the fee fixed, hourly, percentage-based, or mixed?

- What ongoing service is provided (reviews, rebalancing, modelling updates)?

- Do you receive any commissions or referral fees?

- How will performance be measured beyond investment returns?

A Financial Adviser Melbourne should be able to explain fees without jargon. If it feels opaque, pause.

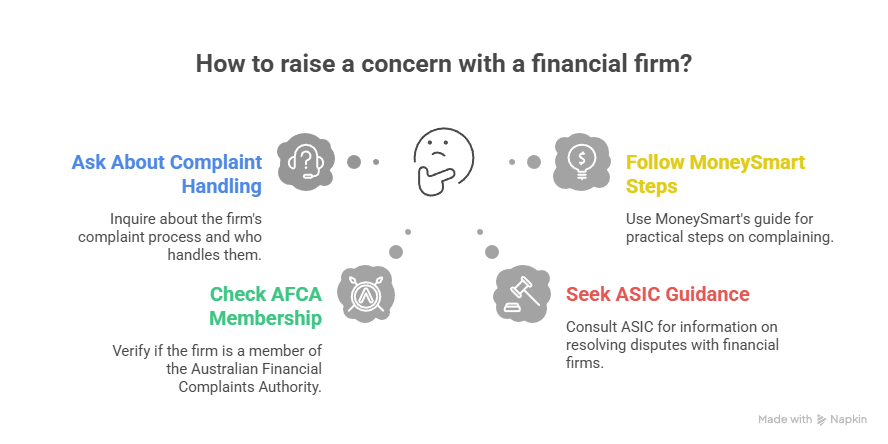

Check the complaints pathway before you commit

Good firms make it easy to raise concerns. Ask who handles complaints and whether the business is a member of the Australian Financial Complaints Authority (AFCA).

ASIC explains that if you can’t resolve a dispute with the firm, you may be able to take it to AFCA (see ASIC – disputes with financial firms). MoneySmart also outlines practical steps on how to complain if things go wrong (see MoneySmart – how to complain).

Coordination matters more than most people think

Advice is most effective when your accountant and adviser work from the same facts. That includes:

- the same income assumptions for the year

- consistent records (especially for CGT events)

- agreement on timing (for contributions, asset sales, business distributions)

If you’re a small business owner, structure choices can be as important as investment choices. This guide can help you frame questions:Setting up a sole trader business and Family trust set up.

A short list of “green flags” and “red flags”

Green flags:

- clear scope, fees, and review process

- stress-testing and downside scenarios are discussed

- tax considerations are acknowledged and coordinated

- you feel comfortable asking questions

Red flags:

- pressure to sign quickly

- one product solution for everyone

- reluctance to provide documents or explain costs

- tax impacts dismissed as “someone else’s problem”

Your first meeting: what to bring

Bring a short pack so the conversation is practical:

- your latest tax return (or business financials)

- a list of assets and debts (with interest rates)

- super statements and contribution history

- insurance summaries (if relevant)

- your top 3 goals and timelines

A Financial Adviser Melbourne can be valuable when advice is tailored, documented, and coordinated with your tax position. The goal is clarity: you should leave with a plan you understand, not just pages of projections.

General information only – seek professional advice before acting.