Searching for a Financial Planner Melbourne often happens after a turning point: a business sale, an inheritance, a new mortgage, or a realisation that retirement is closer than it feels. The challenge is that “planner” can mean different things, and the right choice depends on what you actually need—strategy, product advice, tax coordination, or all three.

This article explains how to approach the search in Melbourne, what’s regulated, and how to make sure tax doesn’t get missed in the process. This is general information only and not tailored financial advice.

Step one: be clear on the job you want done

Before you meet anyone, define the scope:

- Are you building wealth, protecting it, or drawing income in retirement?

- Do you need help selecting financial products (super, managed funds, insurance)?

- Do you mainly need structure and accountability (budgets, debt plan, savings plan)?

- Do you need tax strategy for property, a business, or a trust?

Clarity here saves time and avoids paying for advice you don’t need.

Understand the regulation: advice vs information

In Australia, personal advice about financial products is regulated. If someone recommends particular super funds, investments, or insurance policies for you, they’re providing personal advice and should be properly authorised.

You can check an adviser’s status and authorisations using the public register (see ASIC – Financial Advisers Register). ASIC’s MoneySmart also outlines what financial advice is and what documents you should receive (seeMoneySmart – financial advice).

You should also expect key documents. A Financial Services Guide (FSG) explains who they are, how they’re paid, and their dispute resolution process. If personal advice is given, you should receive a Statement of Advice (SOA) that sets out recommendations, reasoning, and costs in writing (see MoneySmart – statement of advice).

A Financial Planner Melbourne may be licensed, authorised under a licensee, or work in a firm that includes both accountants and advisers. Your due diligence should confirm who is responsible for the advice and what qualifications apply.

Make tax part of the conversation from day one

Tax is often treated as a separate “accountant problem”, but it’s tightly linked to planning outcomes. A strategy can look great pre-tax and disappoint after tax.

Bring these topics up early:

- expected taxable income this year and next

- capital gains tax implications if you sell assets

- property deductions and cash flow vs tax outcomes

- super contribution caps and timing

- business structures (sole trader, company, trust) and how income is distributed

The ATO summarises super contribution caps and key thresholds that often matter in planning (see ATO – contributions caps).

If you’re a small business owner, this overview can help you frame questions around tax outcomes: Strategic tax planning.

Ask how the plan will be built (and what assumptions are used)

Plans can differ dramatically based on assumptions. Ask for clarity on:

- how inflation is modelled

- what return assumptions are used and whether they are conservative

- how fees and taxes are treated in projections

- what happens under a “bad year” scenario

A good planner should be comfortable discussing downside scenarios, not just averages.

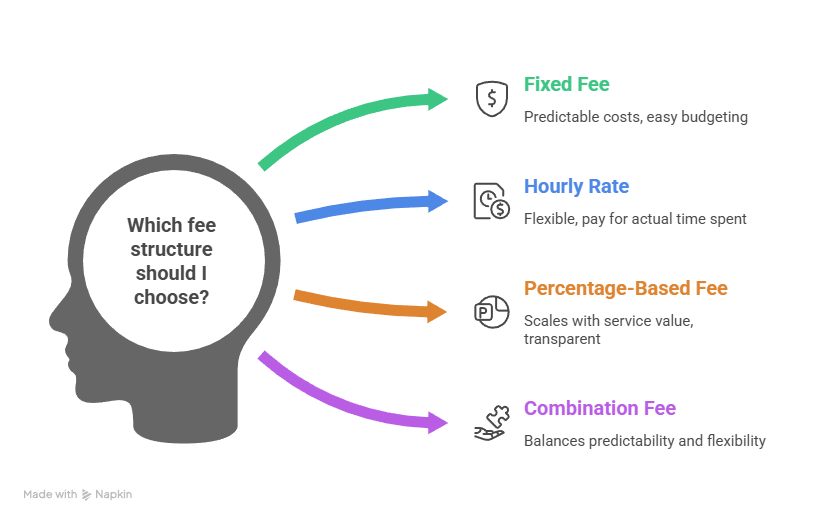

Understand fees and conflicts in plain English

Fees can be charged in different ways: a fixed fee, an hourly rate, a percentage-based ongoing fee, or a combination. The key is whether the cost is transparent and whether you understand what you receive each year.

Ask:

- What is the total first-year cost, including implementation?

- Is there an ongoing fee, and what does it cover?

- Are there any product commissions or referral arrangements?

- How will you measure whether the plan is working?

How an accountant and planner can work together

Many people in Melbourne already have an accountant, especially if they own a business or investment property. The most practical approach is often coordination:

- the planner focuses on strategy, product structures, and long-term modelling

- the accountant confirms tax outcomes, keeps records clean, and handles compliance

- both agree on assumptions and timing (especially around end of financial year)

For investors, these two guides may help you identify tax-sensitive issues to raise:Property investment accountant and Capital gains inherited property.

A short checklist for your first appointment

Take a one-page brief to your first meeting:

- your top 3 goals and target dates

- your income sources (and whether they’re stable)

- your debts, interest rates, and repayment terms

- your super balances and contribution history

- your main assets that could trigger CGT if sold

- what you want help with (and what you don’t)

This makes the meeting about decisions, not paperwork.

When to pause and get a second view

It’s worth slowing down if:

- you’re pushed to sign quickly

- fees are hard to explain in plain language

- tax implications are brushed aside

- you don’t receive clear documents about scope and costs

Choosing a Financial Planner Melbourne should feel methodical. A good fit will welcome questions, be transparent about what they can and can’t do, and coordinate with your tax adviser where appropriate.

General information only – seek professional advice before acting.