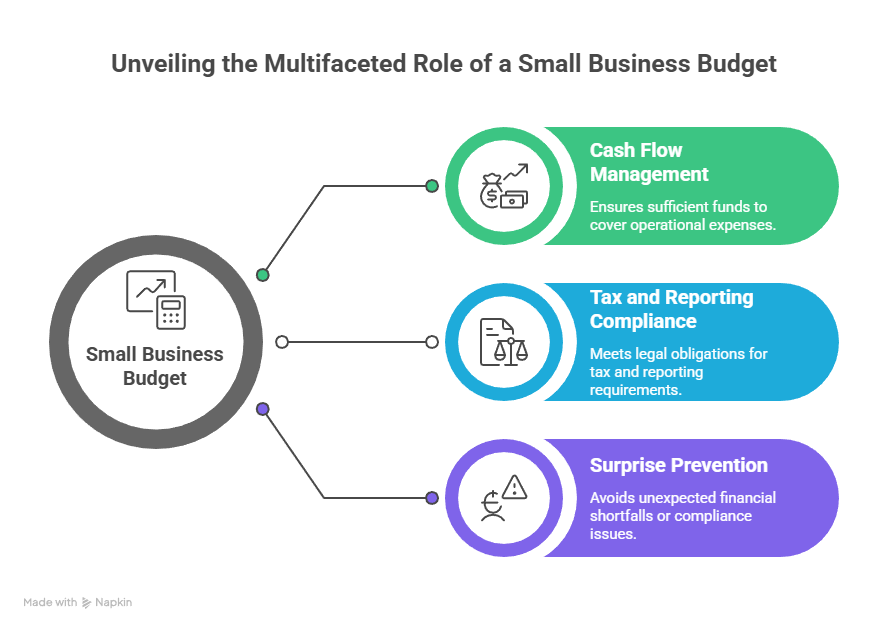

A Budget for Small Business should do two jobs at once: keep the doors open (cash flow) and keep you compliant (tax and reporting). If it only does one of those, you’ll still get surprises—usually at the worst time, like when your BAS is due or a quarterly super payment lines up with a slow sales month.

Below is a straightforward way to build a Budget for Small Business in Australia, using numbers you already have and a process you can maintain. This is general information for Australian businesses, not personal financial advice.

Step 1: Decide what the budget is for

Budgets fail when they try to be everything. Start by choosing the main decisions your budget needs to support over the next 90 days:

- Can we hire, or do we need to wait?

- What sales level do we need to break even?

- How much should we set aside for GST and income tax?

- Do we have enough buffer to survive a slow month?

Write those decisions at the top of the budget. It keeps the model focused and stops “nice-to-have” detail from taking over.

Step 2: Base your cash forecast on receipts, not invoices

Many small businesses invoice today but get paid later. A useful budget forecasts cash received, not just sales made.

Start by looking at the last 3–6 months of bank deposits:

- What is the typical weekly or monthly cash-in?

- Is there seasonality (quiet winters, busy spring, end-of-financial-year spikes)?

- How long do customers take to pay?

The ATO recommends using a cash flow budget or projection to make sure you have funds to meet tax and other obligations (see ATO – manage your business cash flow).

Step 3: Build your ‘non-negotiables’ list

Next, list cash-out items that must be paid no matter what:

- rent or lease commitments

- wages and superannuation

- key supplier accounts

- insurance and licences

- loan repayments

Then add your tax set-asides. Treat them like bills, not leftovers:

- GST and BAS

- PAYG withholding (if you employ staff)

- PAYG instalments (if you’re in the instalment system)

If you want a simple way to line this up with lodgement cycles, this explainer is a helpful starting point: BAS lodgement simplified.

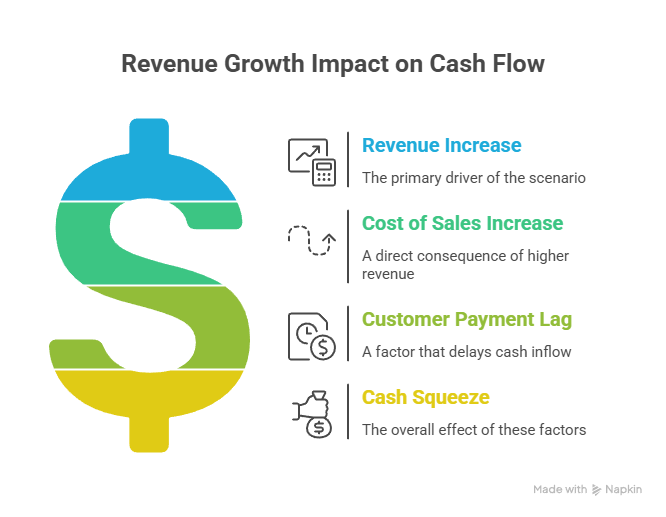

Step 4: Separate variable costs so you can scale safely

A common budgeting mistake is assuming costs rise “roughly” with sales. In reality, some costs scale hard and fast (materials, subcontractors), while others stay stable (rent, software).

Split variable costs into two groups:

- Cost of sales: the direct cost of delivering the work (materials, freight, subcontractors)

- Sales and admin: costs that rise with activity (merchant fees, fuel, casual labour)

This makes it easier to answer a key question: “If we grow revenue by 20%, what happens to cash?” If your cost of sales is also rising 20% and customer payments lag, the budget should show the squeeze.

Step 5: Use a template, then customise the tax lines

A blank spreadsheet is intimidating. The Australian Government’s business portal provides a free template to create and track a budget (see business.gov.au – create a budget).

Once you have a structure, add three lines that many templates miss:

- GST set-aside

- income tax set-aside (or PAYG instalments)

- superannuation timing

These lines turn a normal budget into a Budget for Small Business that matches Australian compliance reality.

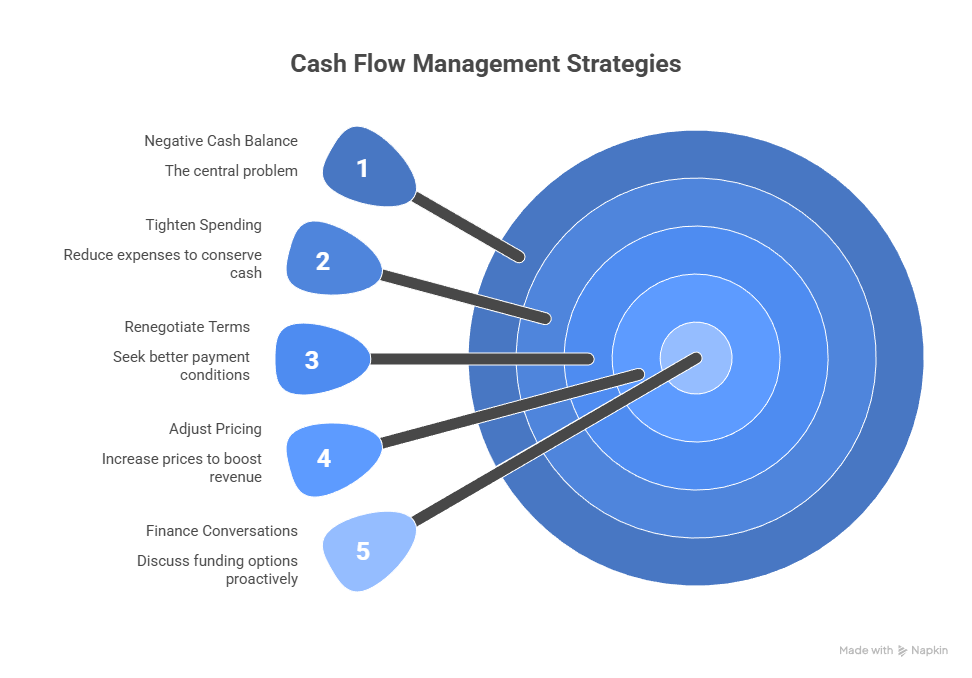

Step 6: Add one “stress test” scenario

Budgets feel useless when reality changes. A simple stress test helps you respond earlier.

Create a copy of your budget with one change:

- revenue down 10% for two months, or

- a major customer pays 30 days late, or

- costs increase (e.g., rent, wages, insurance)

Now look at the cash balance and your buffer. If it goes negative, you have options before it’s urgent: tighten spending, renegotiate terms, adjust pricing, or bring forward finance conversations.

Step 7: Review monthly, but look ahead every week

A monthly review keeps reporting accurate. A weekly look-ahead keeps cash safe.

A workable rhythm:

- Weekly: update expected receipts, check buffer, confirm tax set-asides

- Monthly: compare budget vs actuals, update the next 90 days forecast

- Quarterly: revisit pricing, margins, staffing plans, and tax planning

If your business structure or growth plans are changing, you may also want to review your setup and registrations so the budget assumptions stay true. See: Business setup help in Australia.

A quick checklist before you lock it in

Before you rely on the numbers, run this checklist:

- Have you included GST (and treated it as not-your-money)?

- Do wages include super and leave entitlements where relevant?

- Are “annual” bills set aside monthly?

- Does your cash-in reflect real payment timing?

- Do you have a buffer plan if sales dip?

A budget that answers these questions doesn’t need to be complicated. It needs to be current, honest, and reviewed regularly.

General information only – seek professional advice before acting.