A business budget is more than a spreadsheet. It’s a practical plan for how money will move through your business over the next 3, 6, or 12 months, so you can pay wages, GST, suppliers, and tax on time without surprises. For many small businesses, budgeting is also the fastest way to spot cash pinch points before they turn into late fees or stress.

This article explains how to build a Business Budget that works in Australia, with a focus on cash flow and tax obligations. This is general information only and isn’t personal financial advice.

Start with the “cash reality”, not the profit figure

A budget built on profit alone often fails because profit and cash are not the same thing. Timing issues like GST, PAYG withholding, superannuation, and customer payment terms can leave profitable businesses short on cash.

A simple starting structure is:

- Cash in: customer receipts (by week or month), other income

- Cash out: wages, super, suppliers, rent, loan repayments, tax

If you’re unsure where to begin, use bank statements and accounting reports for the last 3–6 months. The ATO expects businesses to keep records that support income and deductions (see ATO guidance on record keeping).

If cash is tight, start with a weekly view. A four-week rolling cash view can show problems early, especially when a BAS payment, quarterly super, or a big supplier invoice land in the same fortnight.

Map your tax obligations into the calendar

Most budgets fail when tax is treated as an “afterthought”. In Australia, tax and reporting have fixed due dates and regular cash impacts.

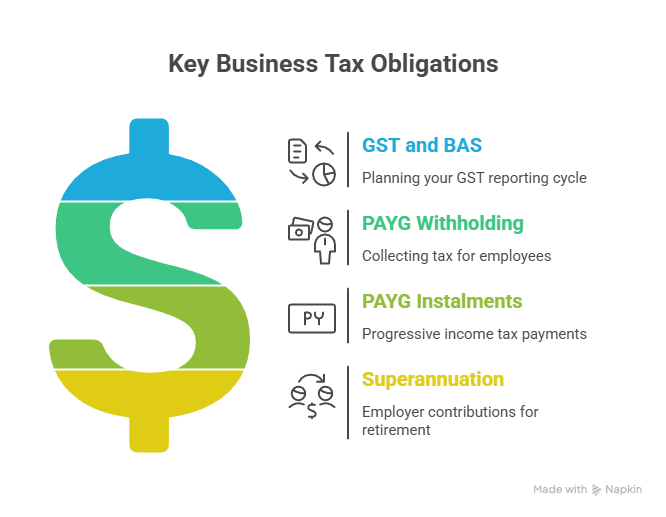

Build these into your Business Budget as scheduled outflows:

- GST and BAS: plan your Business Activity Statement (BAS) cycle and whether you report on a cash or accrual basis (see ATO – GST accounting methods).

- PAYG withholding: if you employ staff, withholding is collected on behalf of the ATO (see ATO – PAYG withholding).

- PAYG instalments: some businesses pay income tax progressively during the year (see ATO – PAYG instalments).

- Superannuation: employer contributions are due by set dates (see ATO – Super guarantee).

If you already lodge BAS, this guide helps you understand where a BAS agent fits: BAS accountant explained.

Build a revenue forecast you can update quickly

Forecasting revenue is not about being “right”; it’s about being consistent and updating when reality changes.

Pick one method:

- Pipeline-based: confirmed work + weighted quotes

- Historical: last year same month, adjusted for changes

- Capacity-based: jobs per week × average sale

Then stress-test it. If sales fall 10% for two months, what breaks first: wages, stock, or BAS cash? If you invoice on 30-day terms, show the lag between “sales” and “cash received”.

Separate fixed costs, variable costs, and ‘lumpy’ costs

Budgeting gets easier when you categorise costs by behaviour:

- Fixed costs: rent, software subscriptions, insurance

- Variable costs: materials, subcontractors, merchant fees

- Lumpy costs: annual licences, equipment replacement, quarterly BAS payments

Lumpy costs are the ones that catch people. If you pay quarterly BAS or annual insurance, create a monthly “set-aside” line so the cash is there when the bill lands.

Add a cash buffer rule, then automate it

A budget becomes useful when it changes how you operate. A practical rule is to keep a minimum cash buffer (for example, 4–8 weeks of fixed costs) in a separate account.

Automation helps:

- Transfer a set amount after each main revenue day (weekly or fortnightly).

- Keep a “tax set-aside” account for GST and PAYG.

- Use bank rules in your software to keep coding consistent.

ASIC’s MoneySmart explains budgeting as a tool for planning and staying on top of bills (see MoneySmart – budgeting).

Review monthly, and do one ‘deep review’ each quarter

A Business Budget is not a once-a-year document. Treat it like a living plan.

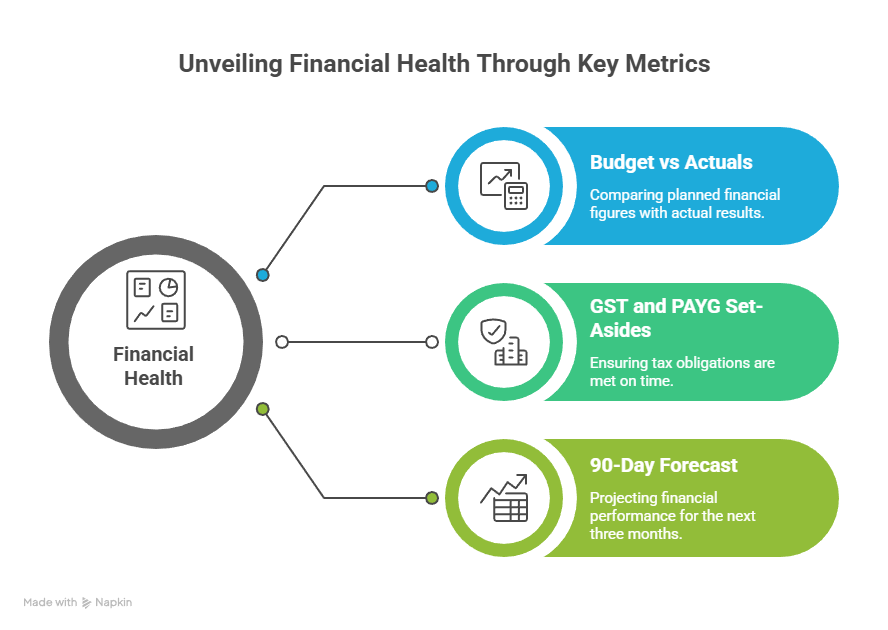

Monthly routine:

- Compare budget vs actuals for revenue and major expenses

- Check GST and PAYG set-asides are tracking

- Update the next 90 days forecast

Quarterly routine:

- Re-forecast revenue based on current pipeline

- Review margins and supplier costs

- Decide whether you can afford hiring, equipment, or marketing increases

If your business is growing, a quarterly tax planning check can reduce surprises at year end. For a broader overview, read Tax planning in Australia.

Common budgeting traps to avoid

Common patterns we see in small business budgeting include:

- Budgeting off “average months” and ignoring seasonality

- Forgetting GST is not profit

- Underestimating wages on-costs (super, leave, payroll compliance)

- Treating owner drawings as “whatever is left”, without a plan

A practical template to start today

For a simple first version, build a one-page monthly budget with:

- Sales (cash received)

- Cost of sales (materials/subcontractors)

- Operating costs (fixed + variable)

- Tax set-asides (GST, PAYG, super)

- Net movement in cash and closing balance

Start simple and update it regularly. A workable budget beats a perfect model you never revisit.

General information only – seek professional advice before acting.