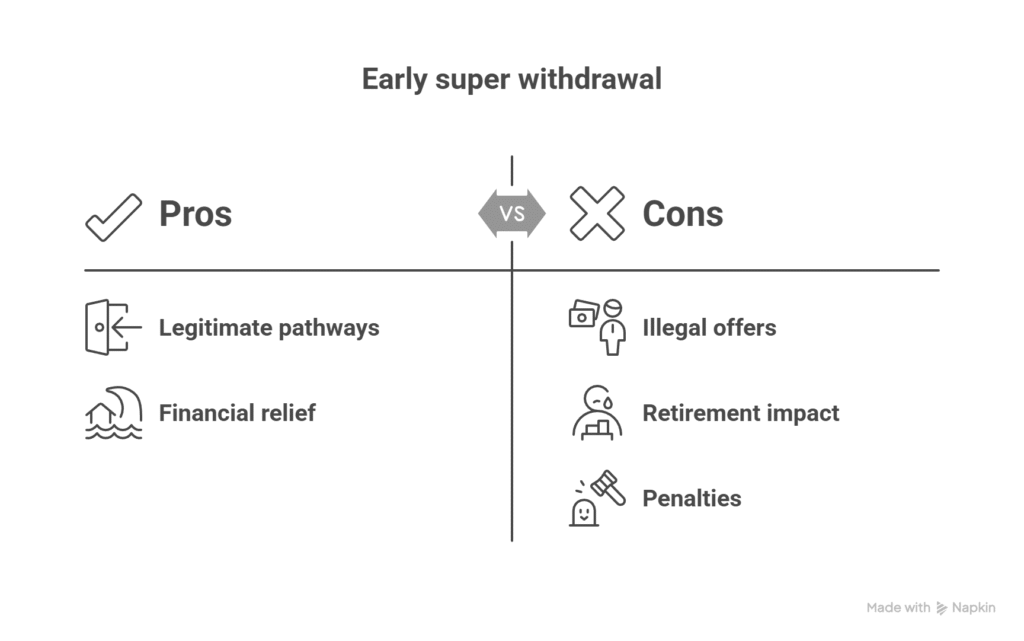

It’s understandable to look for options when money is tight. But trying to withdraw super early is one of the most heavily policed areas of the system, because super is designed for retirement, not day-to-day cash flow. The good news is there are legitimate pathways. The bad news is that many “easy access” offers online are illegal and can leave you worse off.

This guide sets out the legal options, the typical evidence required, and the red flags to avoid.

Start here: super is preserved until a condition of release is met

In most cases, your super is preserved until you meet a condition of release such as reaching preservation age and retiring, or turning 65. Early access is only allowed in limited circumstances (see ATO: When you can access your super early).

If you’re considering an application, focus on the official criteria first. The “why” matters. Wanting to pay bills, buy a car, or fund a holiday won’t qualify.

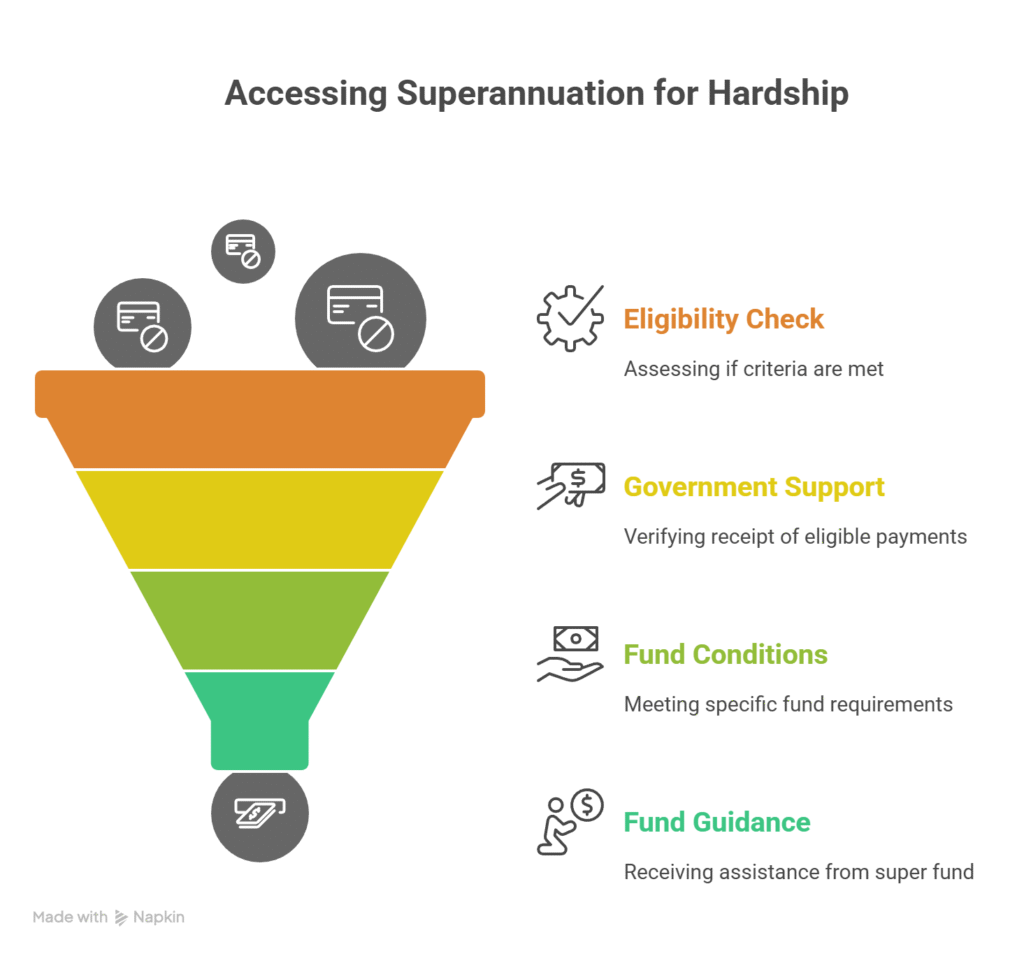

Pathway 1: Severe financial hardship (strict eligibility tests)

Severe financial hardship is a legal pathway, but it is not a general relief program. Eligibility depends on factors such as receiving eligible government income support payments for a minimum period and meeting specific fund conditions. Your super fund will usually guide the process, and each fund’s rules can differ within the legal framework.

A practical tip: treat this as a documented application. Keep copies of Centrelink letters, bank statements and any evidence the fund requests. Missing documentation is one of the biggest reasons applications stall.

Pathway 2: Compassionate grounds (medical and essential expenses)

Compassionate grounds can allow early release for specific expenses, including certain medical treatment, medical transport, mortgage assistance (to prevent foreclosure), disability modifications, and palliative care. These are tightly defined categories, and applications generally require supporting evidence such as medical reports and quotes/invoices.

The ATO lists the eligible categories and the approval process (see ATO: Early access on compassionate grounds).

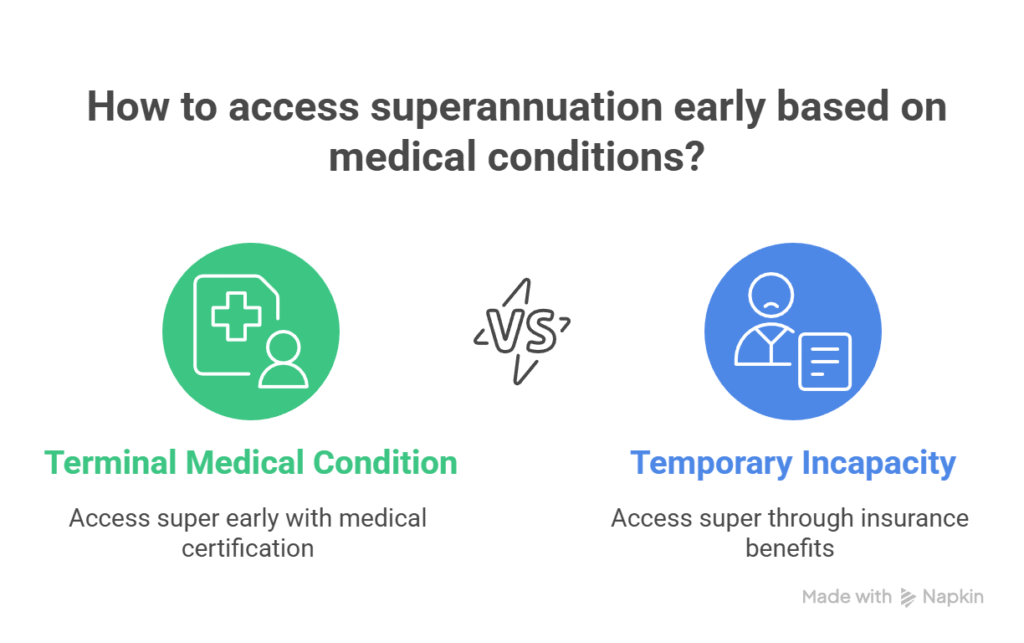

Pathway 3: Terminal medical condition and temporary incapacity

If a person has a terminal medical condition, they may be able to access super early, subject to medical certification requirements. Temporary incapacity can also interact with super, often through insurance benefits held inside the fund. These are situations where paperwork and timing matter, and tax outcomes can differ depending on the benefit type.

Pathway 4: First Home Super Saver (FHSS) – not a withdrawal of your full balance

FHSS is often misunderstood as “taking super out to buy a house”. In reality, it allows eligible first-home buyers to withdraw certain voluntary contributions made into super (plus associated earnings) under the FHSS rules (see ATO: First home super saver scheme).

If your plan involves FHSS, treat it as a forward strategy. It is not the same as withdrawing existing employer contributions for a deposit.

The biggest risk: illegal early access schemes and SMSF “shortcuts”

The ATO has warned about promoters who claim you can access superannuation early by setting up an SMSF and transferring your balance into it, then withdrawing funds for personal use. These arrangements are illegal and can trigger serious consequences, including tax penalties, disqualification as a trustee and enforcement action (see ATO: Illegal early access to super).

How to spot red flags

Red flags include:

- “Guaranteed approval” language

- Pressure to act quickly or pay fees upfront

- Instructions to misstate your circumstances or provide false documents

- A promise that the promoter will “handle it all” without evidence

If you are legitimately setting up an SMSF for retirement planning (not early access), start with governance and compliance. Our guides What is a Self Managed Super Fund? and Set Up a Self-Managed Super Fund (SMSF): Step-by-Step explain the obligations in plain English.

What to do before you apply

If you think you may qualify, a simple process helps:

- Confirm the eligibility category on the ATO website

- Contact your super fund to ask what evidence they need

- Gather documents (letters, invoices, medical reports, bank statements)

- Check tax and Centrelink implications before withdrawing

- Consider alternatives (payment plans, hardship support, refinancing advice)

If you’re under pressure, it can be tempting to chase the fastest option. In practice, the fastest option is often the one that causes the most damage later.

The takeaway

Yes, it can be possible to access superannuation early, but only through defined legal pathways like compassionate grounds, severe financial hardship, or specific medical circumstances. If anyone offers “easy early access”, assume it is unsafe until proven otherwise. Our TTS & Associates experts can guide you through all things superannuation and how it applies to your situation.

General information only – seek professional advice before acting.