Search online for “ATO Super Payment Boost: Who Gets It and How” and you’ll find a mix of helpful information, half-truths, and, unfortunately, scammy advice. In reality, the ATO administers a few legitimate ways the government can top up your super, but eligibility is specific and the amounts are capped.

This guide explains the genuine “boosts”, how they work, and the simple steps that help you avoid missing out.

1) The Low Income Super Tax Offset (LISTO)

LISTO is designed to stop low-income earners paying more tax on concessional super contributions than they would on their wages. If you’re eligible, the ATO pays an amount into your super fund (up to a cap).

The ATO outlines the rules and eligibility in plain language (see ATO: Low income super tax offset and ATO: Government contributions thresholds).

Two practical “don’t miss it” points:

- Make sure your super fund has your Tax File Number (TFN).

- Lodge your tax return (when required), as LISTO is calculated from reported income.

2) The announced LISTO boost from 2027

The Government has announced a future expansion of LISTO from 1 July 2027, including a higher threshold and higher maximum payment (see Treasury: LISTO boost).

3) Government co-contribution (for eligible after-tax contributions)

The co-contribution is another legitimate government super top-up. If you make personal after-tax contributions and meet the eligibility criteria, the government may contribute extra to your super.

The ATO sets out the eligibility tests and income thresholds (see ATO: Super co-contribution).

A common misunderstanding is thinking “any contribution triggers a top-up”. In practice, co-contributions are targeted and generally require: personal non-concessional contributions, income below thresholds, and a lodged tax return.

4) Spouse contributions tax offset

If your spouse has a low income, you may be able to claim a tax offset when you contribute to their super. This is not a payment into your super; it’s an income tax offset you claim in your return if you meet the rules.

The ATO explains the offset and calculation method (see ATO: Spouse super contributions and ATO: Superannuation-related tax offsets).

5) “Boosts” that are not actually boosts: what to watch for

Not everything described online as a “super boost” is legitimate. Two red flags are especially common:

- Promises of early access to super for lifestyle expenses or non-eligible reasons

- Pressure to roll your super into a newly created SMSF quickly, often with fees upfront

The ATO has warned about illegal early access schemes and the penalties involved (see ATO: Illegal early access to super and ATO: When you can access your super early).

If you’re being told “everyone qualifies” or “it’s a loophole”, that’s your cue to stop and verify.

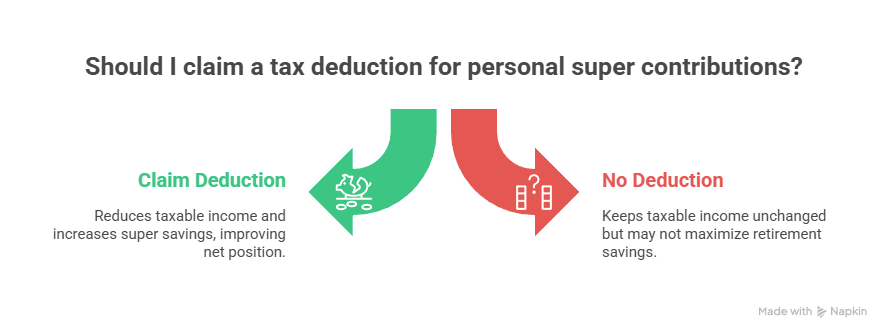

6) Personal deductible contributions: a different kind of “boost”

Sometimes the best “boost” is not a government payment, but using the rules correctly so more of your money stays invested for retirement. In some cases, you may be able to claim a tax deduction for personal super contributions (subject to eligibility and caps). That can reduce taxable income and increase the amount ending up inside super—effectively improving your net position compared with saving the same amount outside super.

This strategy is not automatic and can be easy to get wrong if the notice of intent process isn’t followed. It’s also one area where timing around 30 June matters. If you’re considering it, it’s worth aligning the decision with broader year-end planning, rather than making a last-minute payment.

7) A simple checklist to maximise legitimate boosts

If your goal is to capture legitimate government support without overcomplicating things, start with these steps:

- Confirm your TFN is recorded with your super fund

- Keep your details up to date (name, address, and contact info)

- Make voluntary contributions only after checking eligibility and caps

- Lodge your tax return on time

- Keep proof of any personal contributions (receipts, confirmations)

If you’re also managing BAS and payroll for a small business, this is a good moment to tighten your year-round process so super data is clean and contributions are correctly reported. See BAS Lodgement Simplified for a practical workflow.

The takeaway

A real ATO superannuation payment boost exists, but it’s structured: LISTO, co-contributions and spouse offsets are designed to help specific groups, within defined limits. The safest approach is to check eligibility against ATO sources, keep your super records correct, and avoid anyone promising “easy early access”. TTS & Associates is well versed in superannuation and how it can be applied to your situation.

General information only – seek professional advice before acting.