People often ask, “can superannuation be used to buy a house?” Usually they mean one of two things: using super as a deposit for a home they’ll live in, or using super to invest in property. The rules are very different, and getting it wrong can create tax problems and—worse—illegal early access issues.

This guide explains the main pathways so you can plan without myths.

The general rule: super is for retirement

Superannuation is designed for retirement and is generally “preserved” until you meet a condition of release. Accessing super early is only permitted in limited circumstances, and “I want to buy a home” is not, by itself, a valid reason to withdraw your existing super balance (see ATO: When you can access your super early).

So if you’re hoping to take money out of your current super account to buy a house, the usual answer is no—unless you qualify under a specific scheme or exception.

Pathway 1: The First Home Super Saver (FHSS) scheme

The FHSS scheme is the main “first-home” pathway. It allows eligible first-home buyers to make voluntary contributions to super and later apply to release those contributions (plus associated earnings) for a home deposit (see ATO: First home super saver scheme).

Two practical points matter:

- FHSS is about voluntary contributions, not withdrawing your full existing super balance.

- There are annual and total contribution limits under the scheme, and timing rules around signing contracts and requesting releases.

If you’re considering FHSS, treat it like a process, not a quick hack. You need to check eligibility, plan contribution timing, and leave enough time for the ATO’s determination and release steps.

Pathway 2: Accessing super at retirement age (then buying property)

If you’re older and approaching retirement, you may be able to access super once you reach preservation age and meet a condition of release, or once you turn 65. Preservation age depends on your date of birth (see ATO: Preservation age table).

In that scenario, you might use a lump sum or income stream to help fund a property purchase. The tax outcomes can vary based on age, benefit components and the way you draw funds, so it’s worth modelling before you commit.

Pathway 3: SMSF property rules (investment only)

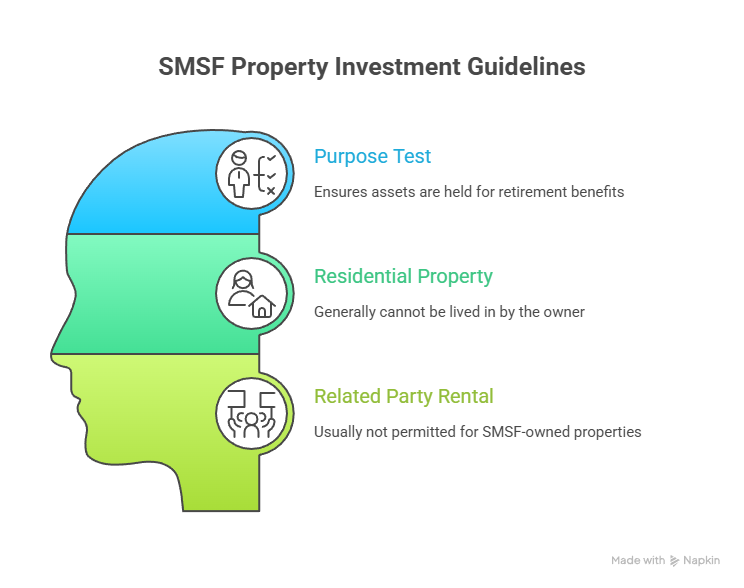

A self-managed super fund (SMSF) can invest in property, including direct real estate. This is where myths circulate, so start with the purpose test: SMSF assets must be held for retirement benefits. That generally means you cannot live in a residential property owned by your SMSF, and you usually cannot rent it to a related party.

Good documentation matters. Trustees should be able to show why the property fits the fund’s investment strategy (risk, diversification, liquidity, and cash flow), not just why it “seemed like a good deal”.

Borrowing inside super: limited and tightly controlled

SMSFs can borrow to buy property only in limited circumstances, typically through a limited recourse borrowing arrangement (LRBA), which has strict rules (see ATO: Limited recourse borrowing arrangements).

Before you go down this route, assess whether you have:

- enough balance to diversify (property is illiquid)

- cash buffers for expenses, vacancies, and compliance costs

- the governance discipline to keep everything arm’s length and recorded

For a practical starting point, see What is a Self Managed Super Fund? and Set Up a Self-Managed Super Fund (SMSF): Step-by-Step.

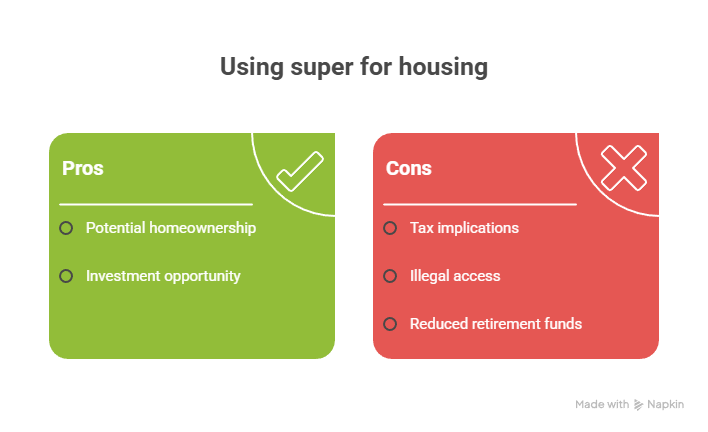

What people miss: the opportunity cost

Even where a pathway is legal, the bigger question is the trade-off. When you use super for a deposit (via FHSS), you may benefit from concessional tax treatment on contributions. But you also need to work within FHSS rules and timings.

When you buy property inside an SMSF, you may get exposure to real estate, but you can lose diversification. Property can also reduce liquidity, which matters when the fund must pay expenses, insurance, and eventually pensions.

A good decision asks: “What does this do to my retirement outcome and my near-term housing goals?”

A decision checklist before you act

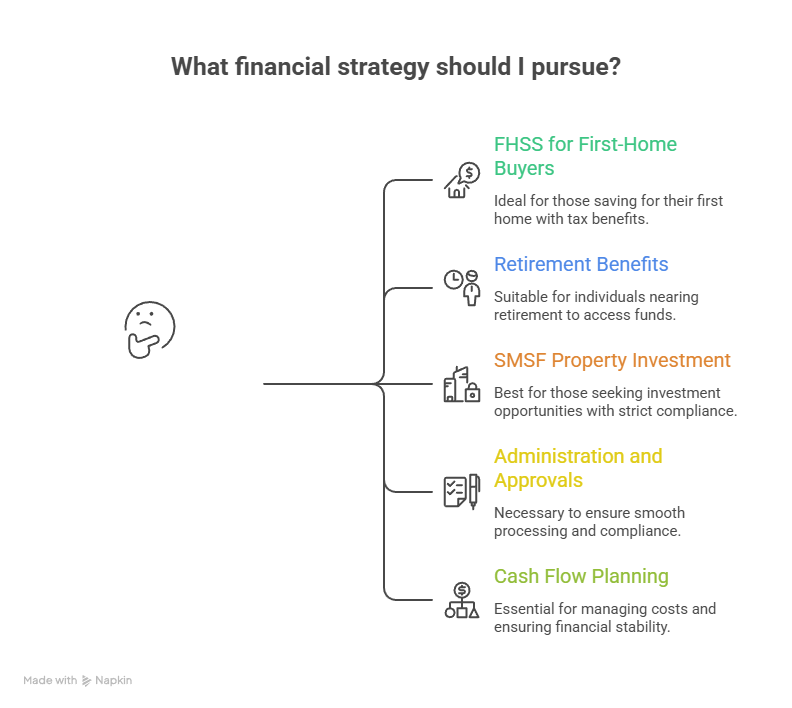

If you’re still asking “can superannuation be used to buy a house?”, run this checklist:

- Are you a first-home buyer considering FHSS (voluntary contributions and later release)?

- Are you approaching retirement and planning to use accessible benefits?

- Are you considering SMSF property (investment only, strict compliance)?

- Have you allowed time for administration and approvals (ATO determinations, fund processing)?

- Have you mapped cash flow for stamp duty, legal costs, and buffers?

If you want a parallel comparison, it can help to review non-super deposit pathways, such as government guarantees and deposit schemes (see MoneySmart: Save for a house deposit).

The takeaway

Super can support home ownership in ways, but the “headline idea” is often misleading. FHSS is about voluntary contributions, retirement access is about conditions of release, and SMSF property is an investment strategy with strict rules. Clarity now prevents expensive mistakes later. Speak with us at TTS & Associates to discuss how superannuation can be applied to your situation.

General information only – seek professional advice before acting.