Borrowing inside super is tightly controlled. Loans for SMSF are generally only allowed under a Limited Recourse Borrowing Arrangement (LRBA), where recourse is limited to a single acquirable asset held in a separate trustee (holding trust). Get the structure or loan terms wrong and you risk non-arm’s length income (NALI) at 45%, contribution cap breaches, or an in-house asset problem. Here’s how to approach LRBAs step-by-step.

What an LRBA looks like

Under super law (SIS Act ss 67A/67B), an LRBA lets an SMSF acquire one asset (or a parcel of identical assets) with borrowing, while other fund assets are protected if the loan defaults. The asset sits in a holding trust until the loan is repaid, then transfers to the fund. The ATO explains the model and its limits.

Single acquirable asset—and replacements

The “single asset” test is strict. Multiple titles usually require separate LRBAs unless they are so integrated they form one asset (for example, strata and car space that cannot be sold separately). Replacement assets are allowed in limited circumstances, but they must be permissible fund investments.

Related-party loans—use the “safe harbours”

If a member or related entity lends to the SMSF, terms must be arm’s length. The ATO’s PCG 2016/5 sets safe-harbour rates and terms for real property and listed-share LRBAs (interest benchmark, LVR, maximum term, and security). Deviate without evidence and income from the asset may be NALI taxed at 45%. The broader NALI framework is set out in LCR 2021/2.

Documentation matters (especially with related parties)

The ATO expects a written loan agreement, correct security over the asset, and evidence of market-value terms. Without this, cash advanced by a related party can be treated as a contribution, potentially breaching caps (see Relationships with the LRBA lender).

Leases to related parties—only in specific cases

Residential property owned under an LRBA cannot be used by members or relatives. Leasing to related parties is generally prohibited unless the property is business real property on arm’s-length terms, and you comply with the in-house asset rules for the holding trust interest.

Cash-flow, contributions and risk checks

Before borrowing, model:

- Net rent vs repayments: include vacancies, rates, insurance and SMSF admin costs.

- Contributions caps: you can’t “tip in” unlimited cash if the property runs short; exceeding caps has tax consequences.

- Liquidity and diversification: your investment strategy must address concentration risk and how the fund will meet expenses.

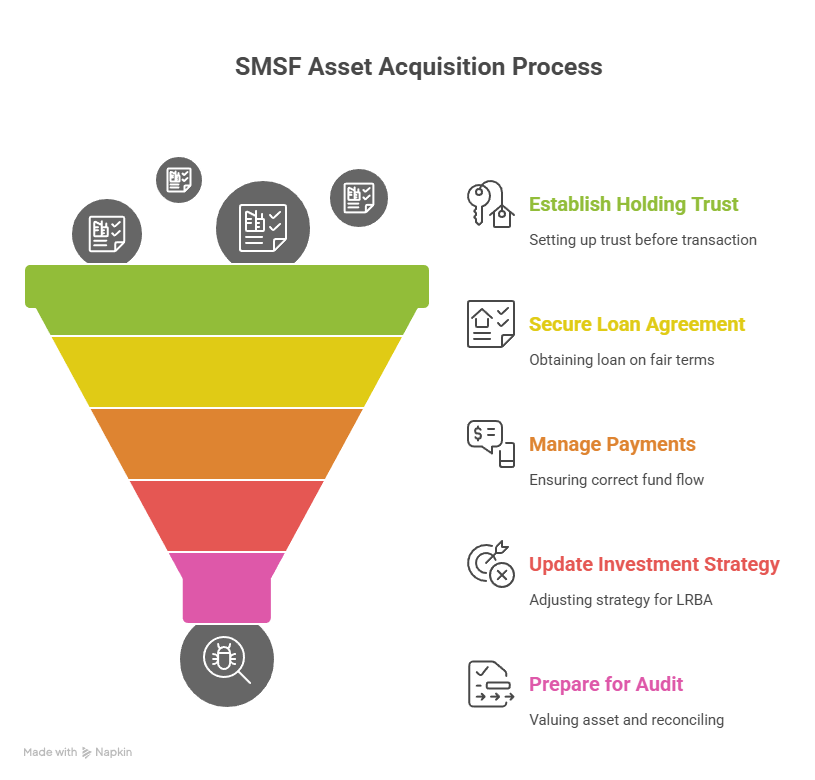

Implementation checklist

- Confirm the asset qualifies as a single acquirable asset and the acquisition path (new purchase vs related-party transfer at market value).

- Put the holding trust in place before exchange/settlement.

- Obtain a written loan agreement on arm’s-length terms (or mirror PCG 2016/5 safe harbours).

- Ensure all payments (deposit, instalments, costs) flow correctly from the SMSF.

- Record minutes updating the investment strategy for the LRBA and concentration risk.

- At year-end, value the asset, reconcile loan statements and prepare for audit.

TTS & Associates can help you keep the books audit-ready—see Superfund Accountant: Stay Compliant and our SMSF accounting guide for practical routines.

Used carefully, LRBAs can expand an SMSF’s investment universe. The key is tight documentation, arm’s-length terms and a realistic cash-flow plan anchored to ATO guidance.

Still got questions? Make time with TTS & Associates and we can help.

General information only – seek professional advice before acting.