Setting up your own super fund is a major financial decision. An SMSF gives you control over investments, but it also brings legal duties, reporting rules and penalties if you get them wrong. Below is a practical sequence to set up a self managed super fund the right way, with links to official guidance and a few tips from the accounting coalface.

Whilst this gives you a practical overview, you should only proceed after speaking with an accounting or tax professional.

1) Decide if an SMSF suits your goals

An SMSF is a trust run for the sole purpose of providing retirement benefits to members. Trustees control investments, ensure the fund stays compliant and keep records for audit. The ATO’s overview explains obligations, risks and what to consider before you start. For a plain-English primer, see TTS & Associates’ What is an SMSF?.

2) Choose trustees and structure

You can have individual trustees (2–6 people) or a corporate trustee (a company acting as trustee). Corporate trustees cost more to set up but simplify membership changes and asset titling. Every trustee must sign the ATO’s trustee declaration and understand duties, including the sole purpose test, valuation, and record-keeping.

3) Draft and execute a compliant trust deed

Your deed sets the rules of the fund. It should cover membership, contributions, investment powers, benefit payments and trustee changes. Execute it correctly under your state’s laws and keep the original safe. The deed should allow for limited recourse borrowing arrangements (LRBAs) if you may borrow in future.

4) Check Australian residency from day one

To access concessional tax treatment, the fund must be an Australian super fund all year. That means establishment/asset location in Australia, central management and control ordinarily in Australia, and the active member test. If a member is overseas, plan to keep management and contributions compliant .

5) Get the identifiers and open accounts

Apply for the fund’s TFN and ABN and elect to be regulated by the ATO within 60 days of establishing the fund. Open a dedicated bank account in the SMSF’s name and ensure future rollovers and contributions flow directly to it.

6) Create your investment strategy (and review it annually)

Trustees must document a strategy covering risk, return, diversification, liquidity, member needs and insurance. Revisit it when circumstances change and annually with minutes to show you reviewed it. The ATO’s investment requirements page outlines the sole purpose test, related-party limits and other restrictions.

7) Know what you can and can’t invest in

SMSFs face rules on related-party transactions, in-house assets and borrowings. For example, acquiring assets from a related party is generally prohibited unless they’re listed securities or business real property at market value. If you borrow under an LRBA, it must be a single acquirable asset (or identical asset class) held in a separate holding trust (see SMSF borrowing restrictions and Rules on assets under an LRBA).

8) Set your admin calendar early

Each year you must prepare accounts, value assets at market value, appoint an approved SMSF auditor at least 45 days before your annual return is due, finalise the audit, and lodge the SMSF annual return (SAR) and pay the levy . New funds that self-lodge usually have a 31 October due date.

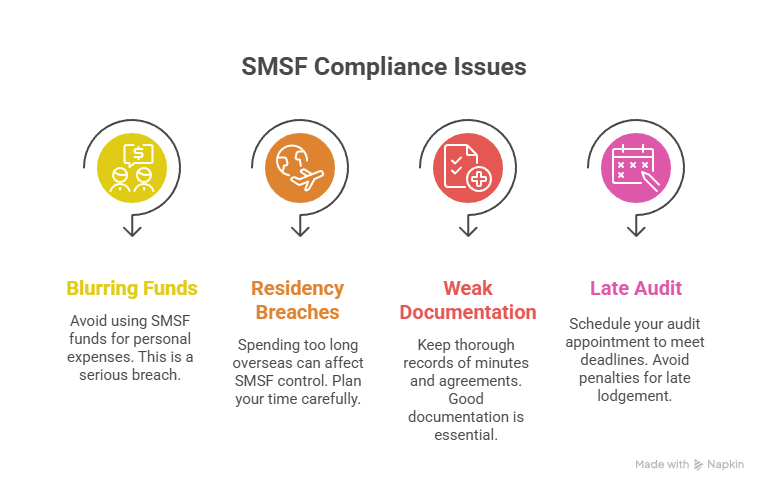

9) Common pitfalls—and how to avoid them

- Blurring personal and fund money: never pay private costs from the SMSF.

- Residency breaches: lengthy time overseas can jeopardise “central management and control”. Plan in advance.

- Weak documentation: minutes, investment strategy reviews and loan agreements must be on file.

- Late audit appointment: diarise the 45-day rule to keep lodgement on track.

10) Build a simple operating rhythm

Adopt monthly reconciliations, quarterly reviews of contributions caps and pension payments (if any), and an annual pre-30 June check. TTS & Associates’ SMSF accounting guide explains how to keep records audit-ready.

With the right foundations, an SMSF can be a powerful retirement vehicle. The key is to set it up correctly, document decisions, and follow the ATO’s rulebook from day one.

TTS & Associates can help you setup that correct structure that fits your plans.

General information only – seek professional advice before acting.