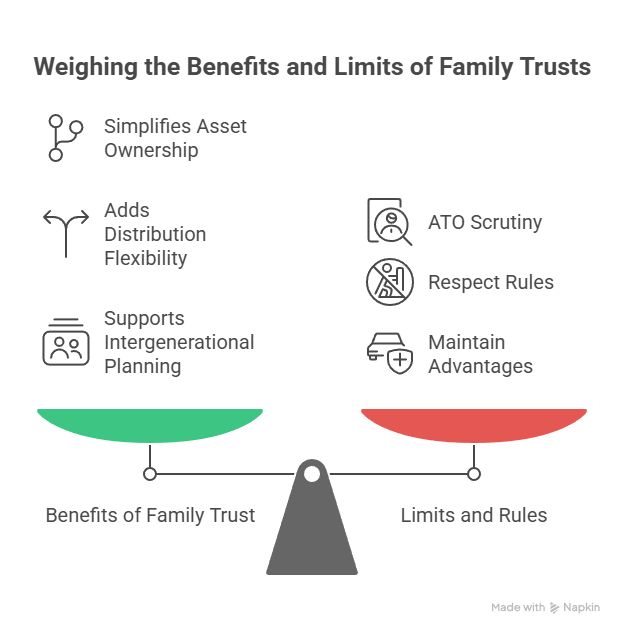

Used well, a family (discretionary) trust can simplify asset ownership, add flexibility for distributions and support intergenerational planning. This article explores the benefits of a family trust, alongside the limits and rules you’ll need to respect so the advantages hold up under ATO scrutiny.

Control and flexibility (with a rulebook)

A key attraction is the trustee’s discretion to distribute income and capital among beneficiaries each year. This gives scope to match distributions with beneficiaries’ circumstances and tax positions. Importantly, the ATO distinguishes colloquial “family trusts” from trusts that have made a formal Family Trust Election (FTE)—the latter unlock specific concessions but narrows the eligible “family group” for distributions.

Asset-holding and succession advantages

Trust assets are held by the trustee, not by individual family members. That separation can support asset-protection goals when paired with appropriate trustee/appointor settings, though protection depends on facts and should not be assumed. From a succession angle, an FTE can help with loss tracing and franking-credit integrity rules for shareholdings, provided the family-group tests are met (see the ATO’s FTE instructions).

Distribution planning and current tax settings

From 1 July 2024, Australia’s personal tax rates changed, affecting after-tax outcomes from trust distributions. Middle-income thresholds were widened and the 32.5% rate dropped to 30%, altering where distributions may land most efficiently within a family (see Treasury’s summary of the 2024–25 tax cuts).

That said, distributions to minors still face Division 6AA’s higher rates on unearned income (except where “excepted income” applies, such as some testamentary trust income). Trustees should model distributions with these rules in mind; the ATO’s instructions for distributions to under-18 beneficiaries outline how the provisions apply. Australian Taxation Office

Compliance: the other side of the ledger

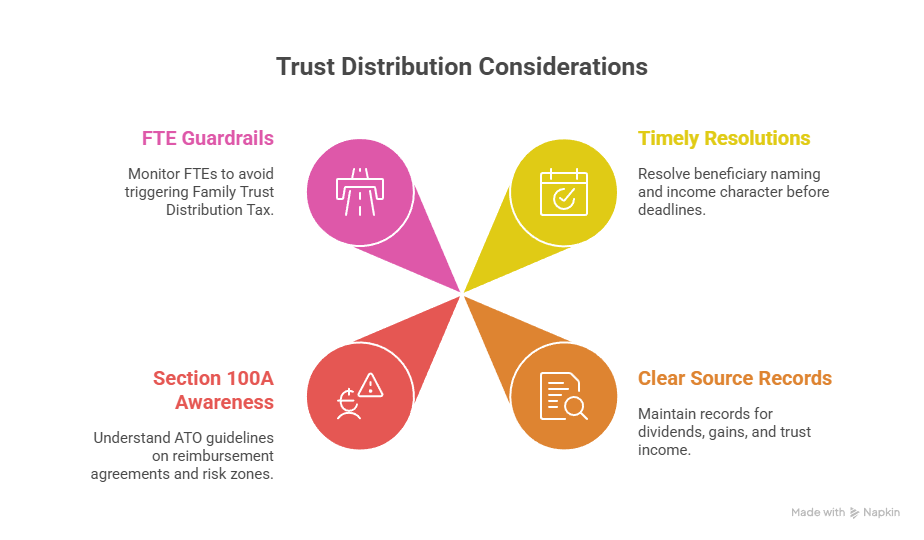

Benefits evaporate if compliance falters. Focus on:

- Timely resolutions (before 30 June or the deed’s date) naming beneficiaries and character of income.

- Clear source records for dividends, capital gains and trust income from other entities.

- Section 100A awareness: the ATO’s PCG 2022/2 sets risk zones for “reimbursement agreements”. Keep arrangements commercial and documented.

- FTE guardrails: once you make an FTE, distributions outside the family group can trigger Family Trust Distribution Tax (FTDT). Keep a family-group register and revisit before year-end (ATO FTE instructions).

When a company or individual might be simpler

For single-asset holdings, a company (with franking) or direct ownership can be administratively lighter. Trusts add deeds, minutes and beneficiary management. The right choice depends on your goals, types of income (e.g., fully franked vs rent), and timeline.

Practical starting steps

- Clarify objectives and beneficiaries; choose a trustee (often corporate).

- Draft and execute a deed; obtain TFN and ABN if carrying on an enterprise.

- Decide whether an FTE is appropriate now or later.

- Build a simple annual compliance calendar (resolutions, BAS if registered, tax return).

- Keep distribution modelling aligned to current personal tax thresholds.

For a step-by-step walk-through and setup checklist, see also TTS & Associates’ How to Set Up a Trust in Australia and Trust Setup Australia: Simple Steps.

General information only – seek professional advice before acting.