Many employees receive fringe benefits as part of their remuneration – perks like a company car for personal use, subsidized loans, or salary-packaged expenses. These perks can be valuable, but it’s important to understand how they affect your tax situation and government entitlements. This guide explains fringe benefits from the employee perspective: what “reportable fringe benefits” are, how they impact things like Medicare and HELP, and what you can do to manage any downsides.

You Don’t Pay FBT – Your Employer Does

First, know that you as an employee do not pay the Fringe Benefits Tax (FBT) on perks you receive – your employer does. For example, if you get a work car that you can drive privately, your employer is responsible for calculating and paying FBT on it. The value of the benefit still gets recorded on your income statement (or PAYG summary) as a Reportable Fringe Benefits Amount (RFBA) if it’s over a certain threshold, but this is not additional taxable income to you. In other words, you don’t add the fringe benefit amount to your salary when lodging your tax return, and you won’t pay income tax on that amount (ATO, 2025).

What is a Reportable Fringe Benefits Amount (RFBA)?

Your RFBA is the grossed-up taxable value of fringe benefits you received above a minimum threshold. Currently, if the total taxable value of your fringe benefits exceeds $2,000 in an FBT year (1 April – 31 March), your employer must report the grossed-up value as an RFBA on your income statement or payment summary. This reported figure is higher than the actual cost of the benefits – it’s “grossed up” to represent what you would have earned as salary (before tax) to get the same benefit value. The key points about RFBAs:

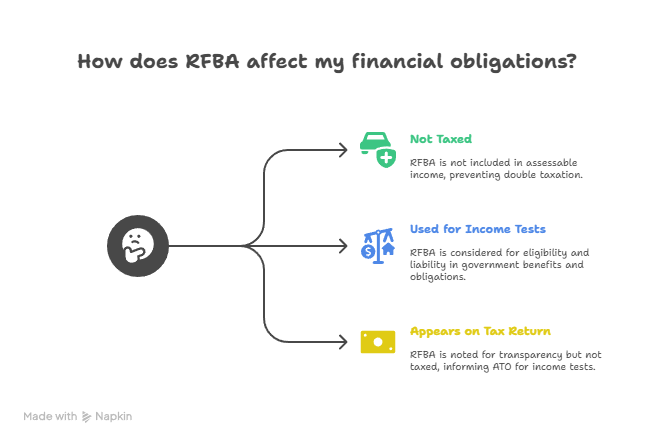

- Not taxed in your return: As noted, the RFBA is not part of your assessable income for calculating income tax. It won’t increase the tax you pay on your tax return (the ATO doesn’t double-tax you; the employer has already paid FBT).

- Used for income tests: The RFBA is used in determining your eligibility for or liability for various government benefits and obligations. Essentially, it gets added to your other income for certain means tests. For example, an RFBA will count towards:

- Medicare Levy Surcharge income threshold – potentially causing you to pay the surcharge if your income including RFBA exceeds the threshold and you don’t have private hospital cover.

- HELP and other study loan repayments – your RFBA is included in “repayment income,” which could push you into a higher repayment bracket for your student loan.

- Family benefits and tax offsets – things like Family Tax Benefit Part A and B, childcare subsidies, and tax offsets (e.g. the seniors and pensioners tax offset) use income tests that include any RFBA.

- Super contributions surcharge and other thresholds – certain superannuation-related taxes and older Centrelink assessments also consider RFBA as part of your income.

- Appears on your tax return for info: If you lodge online with myTax or through an agent, your RFBA will typically be pre-filled or noted in the tax return (there’s a section for reportable fringe benefits). This is just for transparency – it doesn’t mean you are taxed on it, but it informs the ATO for the above income tests.

Managing the Impact of Fringe Benefits

If you have a large RFBA amount, you might notice it affects things like your HELP repayment or Medicare surcharge. While you shouldn’t decline genuine benefits just to avoid an RFBA, it’s something to be mindful of. Here are some tips:

- Consider the trade-offs: In some cases, you might have a choice between receiving a benefit or extra salary. For example, a particular benefit might be pushing your combined income (with RFBA) just over the Medicare surcharge or other threshold. In such a case, you could talk with your employer about adjusting your package or making contributions to stay below the cutoff if feasible.

- Contribute to reduce your RFBA: If you’re salary packaging a benefit, you could ask about making an employee contribution toward the cost. For instance, some employees pay part of their novated lease car expenses with after-tax dollars. This can reduce the taxable fringe benefit value that the employer reports (since you’ve effectively offset some of the cost), lowering your RFBA. You’re essentially trading off some tax savings to improve your position in income tests – it may be worthwhile if an RFBA is causing you to lose valuable entitlements.

- Focus on exempt benefits: Some benefits are specifically exempt from FBT (and thus won’t generate an RFBA). Examples include certain work-related items (like a laptop or phone primarily for work use) or minor benefits under $300. While you usually don’t control what benefits your employer offers, it’s useful to know that not all perks are equal. If you’re in discussions about your remuneration, you could favor benefits that don’t come with FBT strings attached.

For more on how fringe benefits are calculated and how novated car leases in particular work (a common employee benefit), you can read our guide on FBT and novated leases which covers recent exemptions for electric vehicles and more.

Employee’s Guide to Understanding Fringe Benefits. TTS & Associates can guide you—Contact Us