Succession planning means preparing for a smooth transfer of business ownership or leadership when the current owners or key managers step down. Whether you run a family business or other enterprise, having a formal succession plan can ensure the business you built continues to thrive in the next generation. It’s about being proactive: identifying who will take over, how the handover will occur, and addressing financial, legal and tax implications in advance. The ATO cautions that failing to plan succession can lead to unintended tax consequences for business owners and their families (ATO, 2025). This article outlines why a succession plan is important and the key steps in developing one.

Why You Need a Succession Plan

Imagine a scenario where a business owner suddenly wants to retire or faces a health issue without any succession plan. The business might struggle to continue, employees and customers face uncertainty, and the owner may not get full value when exiting. A well-crafted succession plan provides certainty and continuity. It aims to:

- Preserve business value: By planning an orderly transition, you avoid a forced sale or closure that could significantly undervalue the business.

- Reduce conflicts: In family businesses, succession can be emotional. A clear plan (deciding which child or partner takes over, for example) helps prevent disputes among family or co-owners.

- Optimise tax outcomes: With planning, you can structure the handover to minimize taxes. For instance, there are small business capital gains tax (CGT) concessions that, if you qualify, can significantly reduce or eliminate the tax on the sale or transfer of your business. Planning ahead allows you to meet the conditions and maximize these tax benefits.

- Retain key talent: If a successor is identified and groomed, they are more likely to stay and lead, ensuring stability for staff and clients.

Without a plan, succession may occur in a rushed or suboptimal way (e.g. a fire-sale of the company or heavy tax liabilities on transfer). Succession planning essentially gives you control over how and when you exit, rather than leaving it to chance or crisis.

Key Components of a Succession Plan

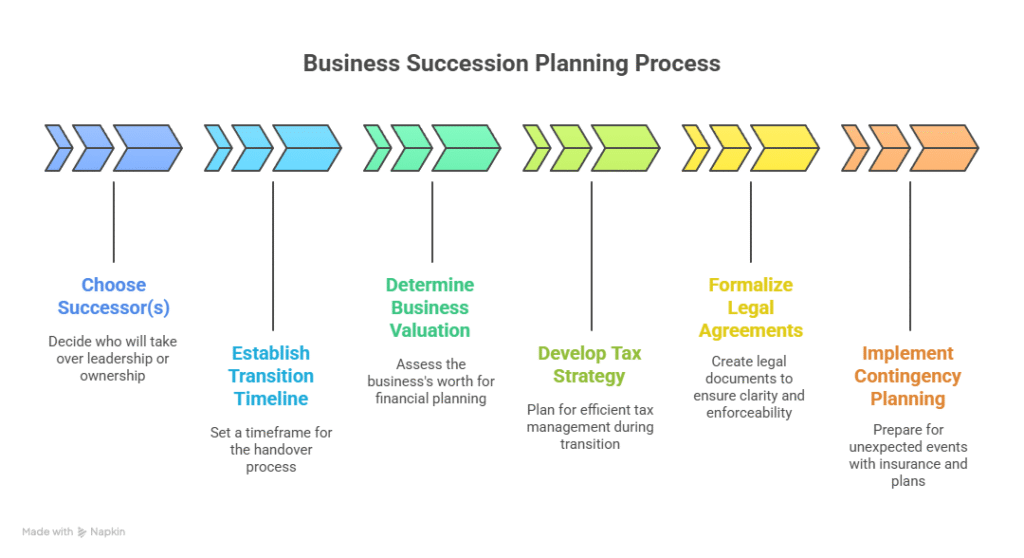

Every business is different, but an effective succession plan often includes:

- Chosen successor(s): Decide who will take over the business leadership or ownership. It could be family members, business partners, senior employees through a management buyout, or an external buyer.

- Timeline for transition: Establish a timeframe for the handover. You might plan to retire in 5 years, with gradually reduced involvement. A phased transition allows the successor to assume more responsibility while the current owner remains to mentor and monitor.

- Business valuation and funding: Get a realistic valuation of the business. If the successor will purchase the business (fully or partially), determine how that will be funded. Options include installment payments to the retiring owner, external financing, or using insurance proceeds (for example, funding a buy-sell agreement through a life insurance policy if a partner passes away).

- Tax and structure strategy: Work with an accountant or tax advisor to structure the transfer efficiently. This could involve reorganizing the business structure (for instance, moving assets into a family trust or company) or timing the sale of shares to take advantage of tax concessions. For example, integrating the 15-year exemption or retirement exemption in your plan can allow a retiring small business owner to sell or hand over the business with little to no capital gains tax.

- Legal agreements: Formalize the plan in legal documents. This might include updating the company’s shareholders’ agreement or partnership agreement to reflect buyout terms, creating a buy-sell agreement (which outlines what happens if an owner dies or leaves), and updating your personal estate plan (wills, etc.) to align with the business succession. Getting these legal frameworks in place provides clarity and enforceability.

- Contingency planning: A good succession plan also covers unexpected events. Consider insurance (like key person or shareholder insurance) to provide funds or stability if an owner dies or becomes disabled. This ensures the business isn’t thrown into financial disarray and can fund buyouts if needed under difficult circumstances.

Keeping the Plan Current

Once in place, a succession plan is not static. Business and personal circumstances evolve – for instance, the chosen successor might change their mind about taking over, or new tax laws might offer different opportunities. It’s wise to review your succession plan every couple of years or when major changes occur (like significant growth, a family change, or new legislation). Adjust roles, timelines, and financial arrangements as needed so the plan remains relevant and effective.

Start Planning Early and Seek Advice

Succession planning is a journey, not a one-time event. It’s often wise to start the process years before the expected transition. This lead time lets you groom your successor, accumulate necessary funds, and work through any issues well ahead of the handover.

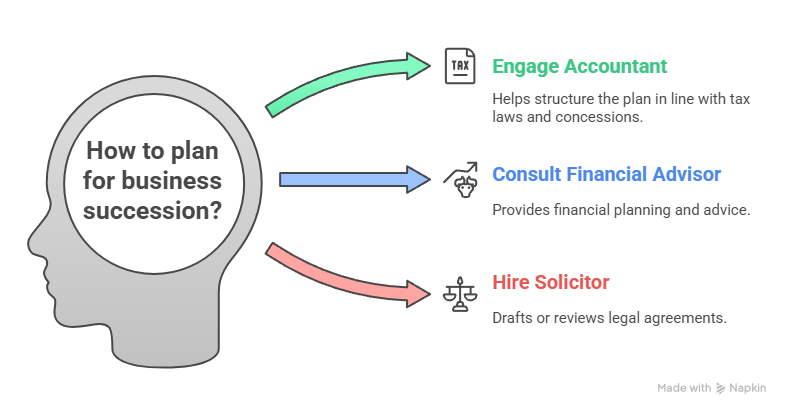

Because succession involves complex issues of family, finance, and tax, getting professional advice is invaluable. Engage your accountant or financial advisor early – they can help structure the plan in line with tax laws and concessions. A solicitor with experience in business or estate planning should draft or review the legal agreements involved.

Remember, a succession plan doesn’t mean you have to exit the business right away – it simply means when the day comes, the transition will be on your terms. You’ll protect what you’ve built and give the next generation the best chance of success. Our business succession planning guide provides a detailed 2025 roadmap, including local Victorian considerations, for those ready to dive deeper. By planning ahead, you ensure your business legacy is secure and that you, as the outgoing owner, meet your personal and financial goals in the process.

Plan for tomorrow’s success today. TTS & Associates can help with succession planning—Contact Us