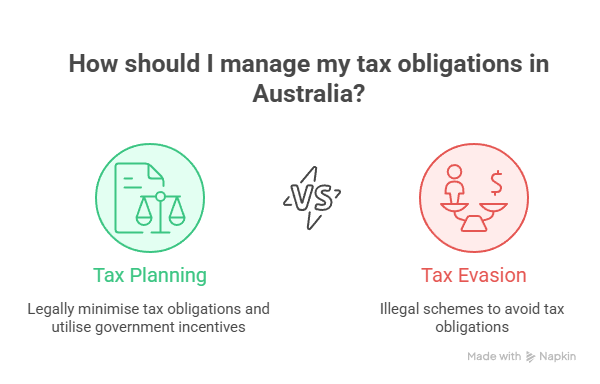

Tax planning in Australia is essential if you want to legally minimise your tax obligations while making the most of government incentives. The Australian Taxation Office (ato.gov.au) supports legitimate tax planning, which involves arranging your financial affairs to reduce your taxable income in compliance with the law. It’s important to distinguish this from tax evasion or participation in illegal schemes.

Here are five smart and entirely legal tax planning strategies Australians can use to reduce their tax bill and boost financial wellbeing.

1. Maximise Superannuation Contributions

Superannuation is one of the most tax-effective tools available for long-term wealth building. Concessional contributions – such as employer contributions and salary sacrifice – are taxed at just 15%, which is often much lower than your marginal income tax rate.

By directing part of your pre-tax income into super, you reduce your taxable income and increase your retirement savings. In the 2024–2025 financial year, the concessional contributions cap is $27,500. You can also make personal contributions and claim a tax deduction if you’re self-employed or not receiving enough employer contributions.

Just be sure not to exceed the cap – contributions over the threshold are taxed at a higher rate. Smart planning ensures you make the most of your available cap each year.

2. Take Advantage of Business Deductions and Depreciation

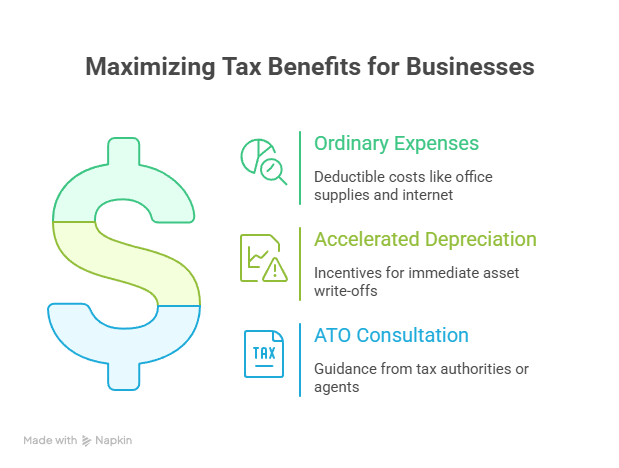

If you run a business or have income from freelancing or a side hustle, claiming all eligible deductions is essential. Ordinary expenses directly related to earning assessable income – such as office supplies, internet, and vehicle use for business – can be deducted to reduce your taxable income.

In addition, many small businesses can benefit from accelerated depreciation incentives, such as the instant asset write-off. This allows you to immediately deduct the full cost of eligible assets (up to a threshold), rather than depreciating them over several years.

These provisions change depending on the federal budget, so it’s worth consulting the ATO website or a tax agent to ensure you take full advantage of current incentives.

3. Time Your Income and Capital Gains

The timing of income and expenses can significantly impact how much tax you pay in a given year. For example, if you’re a sole trader or run a small business under cash accounting, delaying the issue of invoices until after June 30 can push income into the next financial year. Conversely, you might bring forward expenses – such as insurance premiums or software subscriptions – into the current year to maximise your deductions.

Capital gains timing is equally important. Holding onto assets for more than 12 months qualifies you for a 50% capital gains tax (CGT) discount as an individual. So, if you’re considering selling an asset, it’s worth checking how long you’ve held it.

You should also consider the tax year in which the gain will fall. If you expect a lower income next year (due to retirement, a gap year, or business slowdown), deferring the sale may reduce your CGT liability.

If you’ve made capital losses, they can be used to offset gains – another reason to coordinate your asset sales wisely.

4. Use Offsets, Rebates and Income Exemptions

Australia’s tax system includes various offsets and rebates designed to directly reduce the amount of tax payable – not just taxable income.

- Low Income Tax Offset (LITO): Applies if your income is below certain thresholds.

- Low and Middle Income Tax Offset (LMITO): Though this has now phased out, other incentives may be introduced in future budgets.

- Spouse Super Contribution Offset: If you contribute to your low-income-earning spouse’s super fund, you may receive an offset of up to $540.

- Senior Australians and Pensioners Tax Offset (SAPTO): This can significantly increase the effective tax-free threshold for older Australians.

You may also be entitled to the private health insurance rebate, which can either be claimed through your insurer or in your tax return.

Additionally, some types of income are partially or fully tax-exempt, including:

- Certain government pensions and allowances

- Redundancy payments (up to a threshold)

- Some scholarships or study-related payments

These exemptions can lower your effective tax rate, so it’s important to identify which income sources are non-taxable.

5. Keep Accurate Records and Get Expert Advice

None of the above strategies will work effectively if you fail to keep good records. Maintaining clear, up-to-date documentation ensures you can substantiate your claims and maximise deductions.

Digital bookkeeping tools such as Xero, MYOB, or QuickBooks can help automate this process. They make it easier to:

- Log business expenses

- Track super contributions

- Store digital copies of receipts

- Reconcile your income and expenses

Finally, consider consulting a registered tax agent or financial adviser to get personalised advice. They can:

- Recommend strategies specific to your financial goals

- Help you stay up to date with tax law changes

- Ensure compliance while reducing your tax liability

- Review your business structure to determine whether a company or trust might be more tax-effective than a sole trader model

Final Thoughts: Take Action Early

For further ideas on reducing your tax legally, you can read Tax Planning for Victorians: 10 Smart Ways to Save Tax, which shares practical tips that apply broadly, not just in Victoria. Or contact us for a chat.

General information only – seek professional advice before acting.