A self-managed super fund set up in Australia gives you control over your retirement investments—but with that control comes significant legal and administrative responsibility. A self-managed super fund (SMSF) is a private superannuation fund that you manage yourself, providing greater flexibility in investment decisions and retirement planning.

If you’re a new trustee looking to start an SMSF, here’s a step-by-step guide to help you understand how to set up a self-managed super fund and meet your compliance obligations.

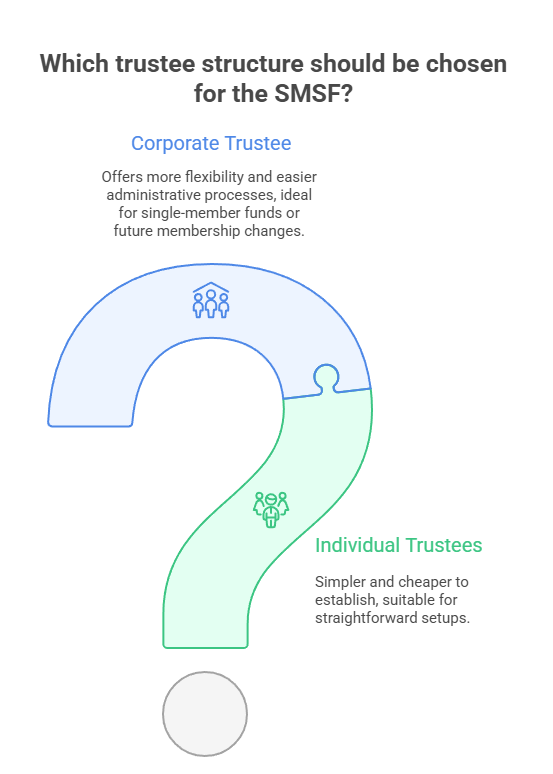

1. Choose Your SMSF Trustee Structure

The first step in SMSF set up is deciding on the fund’s trustee structure. You have two main options:

- Individual trustees – each member is a trustee.

- Corporate trustee – a company acts as trustee, and each member is a director of that company.

Individual trustees are simpler and cheaper to establish, but corporate trustees offer more flexibility—particularly if the fund will have only one member or if future changes to membership are likely. Corporate trustees also make administrative processes, such as asset ownership changes, easier to manage.

Regardless of structure, all members must be either trustees or directors of the corporate trustee. You must also ensure each trustee is eligible (i.e. not disqualified under superannuation law) and understands their legal responsibilities.

2. Establish the Trust and Trust Deed

A self-managed super fund is legally a trust. To establish the trust:

- Draft a trust deed, the legal document that sets out the fund’s rules, including benefit payments, trustee powers, and decision-making processes. This should be done by a legal professional or SMSF service provider to ensure full compliance.

- Execute the deed by signing it—this formally creates the fund.

- Appoint the trustees or set up the corporate trustee, if applicable.

- Admit all fund members.

Once the trust deed is executed, your fund legally exists. At this point, you can start arranging to roll over super from other funds or accept contributions, but you must never use SMSF funds for personal use. All money held in the SMSF must be used solely to provide retirement benefits to members.

Securely store the original signed deed—it’s one of your most important documents.

3. Register the Fund with the ATO

You must register your SMSF with the Australian Taxation Office (ATO) to receive tax concessions and become a regulated fund.

Here’s how:

- Apply for an Australian Business Number (ABN) and Tax File Number (TFN).

- Elect for your fund to be regulated under the Superannuation Industry (Supervision) Act 1993.

- Complete the registration within 60 days of establishing the fund.

Once processed, the ATO will issue your ABN and TFN, and your fund will be listed on the Super Fund Lookup register, which allows employers and other funds to verify your fund’s compliance status.

Important: Only regulated SMSFs can receive rollovers and employer contributions and access favorable tax treatment (15% on income, versus 45% for non-compliant funds).

4. Set Up the SMSF Bank Account and ESA

Open a bank account in the SMSF’s name, using the fund’s ABN. This account is used for all fund transactions, including:

- Receiving rollovers and contributions

- Investment income and expenses

- Paying taxes and other fund costs

By law, SMSF assets must be kept separate from personal or business assets of members.

You also need to obtain an Electronic Service Address (ESA)—a digital address that enables your fund to receive employer contributions and rollover data via the SuperStream system. You can get an ESA from SMSF messaging providers (often included with administration services).

Once you have an ESA, provide it (along with the SMSF’s ABN and bank details) to your employer and any other funds you’re transferring super from.

5. Develop an Investment Strategy

A written investment strategy is a legal requirement for all SMSFs. It must:

- Outline your investment objectives

- Detail the asset types your fund will invest in

- Consider risk, diversification, liquidity, and member insurance needs

Common SMSF investments include:

- Direct shares and ETFs

- Residential or commercial property

- Term deposits

- Managed funds

The strategy must be tailored to your members’ retirement goals and reviewed regularly. It does not need to be submitted to the ATO, but your SMSF auditor will review it annually.

You are also legally required to consider whether the fund should hold insurance (life, total permanent disability, or income protection) for each member. Whether or not you proceed with insurance, you must document your decision in the investment strategy.

6. Understand Ongoing Trustee Responsibilities

After your self-managed super fund is set up, you must comply with ongoing regulatory and administrative obligations, including:

- Lodging an SMSF annual return with the ATO (includes tax return, financial statements, and member data)

- Undergoing an independent audit every year

- Maintaining accurate records of all fund decisions, transactions, and minutes

- Keeping up to date with super laws and regulatory changes

Non-compliance can result in severe penalties, including disqualification of trustees, tax penalties, or even loss of the fund’s complying status. Many trustees choose to engage an SMSF accountant or administrator to help manage their compliance tasks.

Should You Set Up a Self-Managed Super Fund?

While setting up an SMSF provides flexibility and control over your retirement investments, it also involves time, effort, and responsibility. You need to stay on top of rules, complete annual compliance tasks, and make sound investment decisions.

If you’re still exploring whether an SMSF is right for you, check out our SMSF Guide Victoria: What Is a Self Managed Super Fund? for a complete overview of pros, cons, and key considerations.

Ready to Set Up Your SMSF?

If you’re confident in taking on the role of trustee and are ready to gain control over your super, setting up a self-managed super fund can be a powerful strategy for building wealth toward retirement.

Need help getting started? Contact us to speak with an SMSF specialist about setting up your fund the right way.